[Update] Alibaba

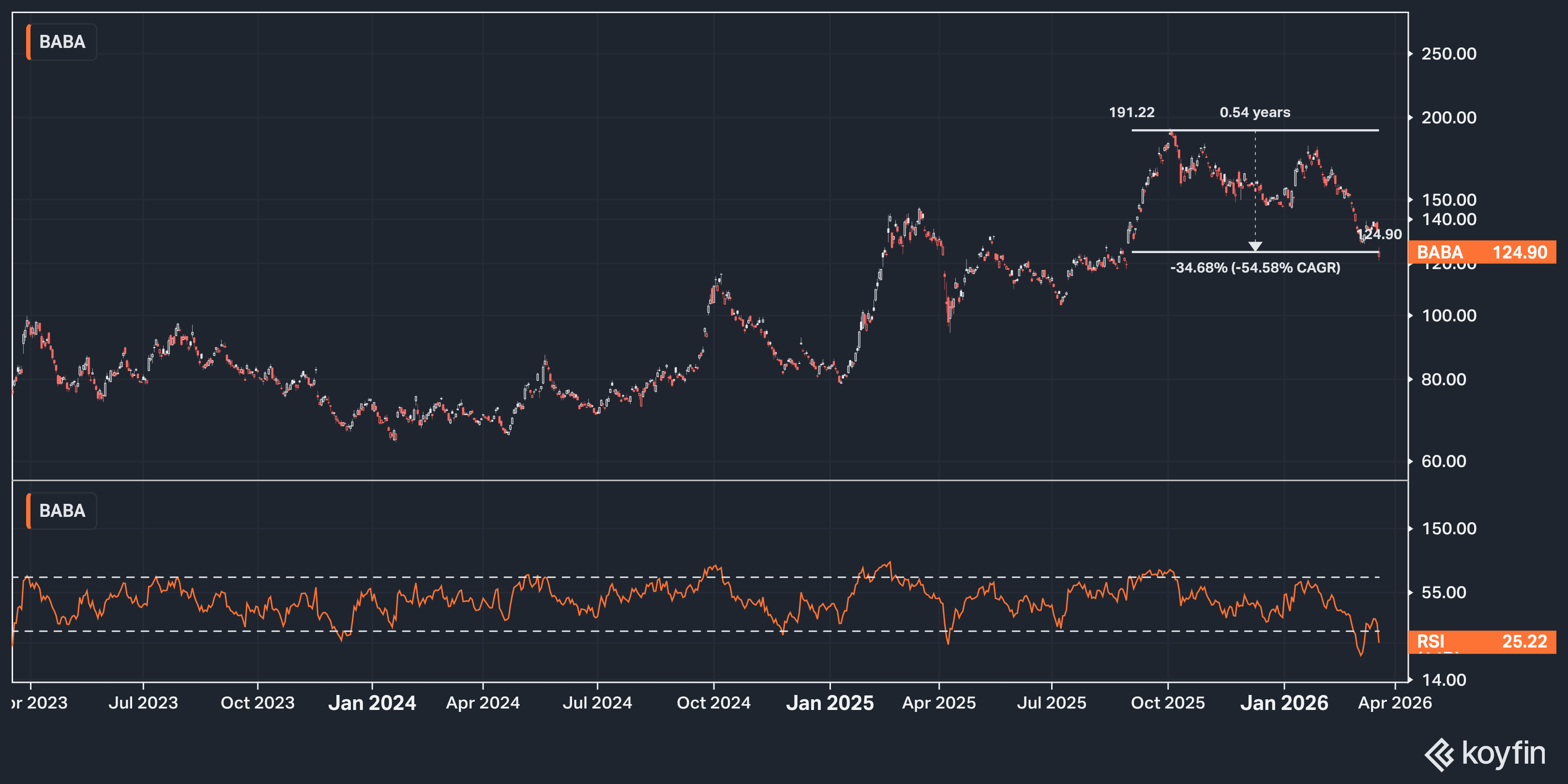

Down 7% on a quarter they literally pre-announced. Ok.

It’s been a brutal couple months to be a BABA shareholder. Stock is down about ~35% from the highs, the Qwen team is losing people, the market hates China again, and now we get an earnings print that looks ugly on the surface…

I want to get some quick thoughts out while the call is still fresh, because I think the reaction today is wrong.

I wrote a whole post back in January walking through exactly what management was telegraphing on the pre-earnings sell-side calls.

They told the Street to lower the bar on basically everything. Cloud, e-commerce, margins, all of it. And then they delivered pretty much right in line with what they guided.

Stock was down about ~7% today. I honestly don’t get it…

Maybe some of us (myself included) thought they were sandbagging a bit more than they were. Fair enough. But the quarter wasn’t bad. It just looks bad on a headline basis because of the divestitures and a late Lunar New Year that pulled activity out of the December quarter and into March.

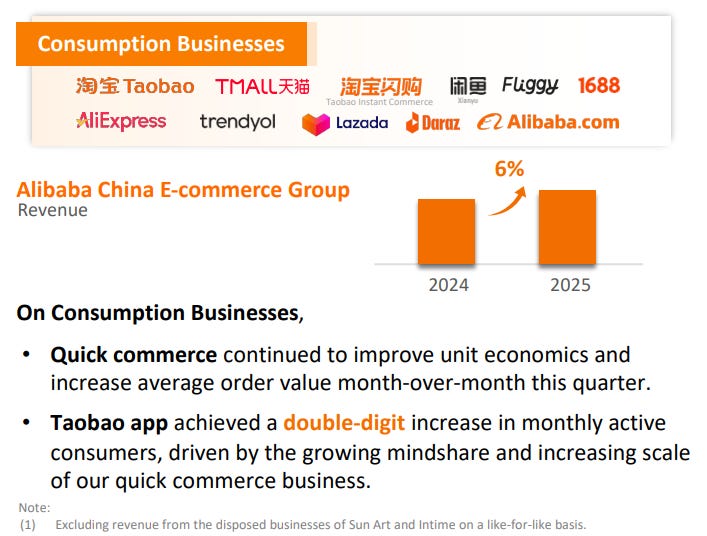

Strip out Sun Art and Intime and you’re at ~9% like-for-like revenue growth.

Customer management revenue grew ~1%. That is soft, I won’t sugarcoat it. But Wu said on the call that heading into the March quarter:

“our physical goods GMV and CMR trend have significantly recovered.”

Lunar New Year spending falls into Q4 this year, Qwen crossed 300 million MAUs with 140 million users trying AI-driven shopping in February alone, and 88VIP members crossed 59 million. I think the e-commerce numbers look noticeably better next quarter.

Quick commerce grew ~56% to RMB 20.8 billion, very impressive growth… unit economics continued to improve sequentially.

Wu laid out the ambition on the call: over RMB 1 trillion in quick commerce GMV by FY28, profitable by FY29.

The market clearly doesn't love this part of the business. I think a lot of people were hoping the unit economics would improve faster, and hearing a profitability target of FY29 instead of FY27 or FY28 probably spooked a few holders. The economics are getting better, losses per order have come down meaningfully since the summer, but "better" and "good" are two different things and the market wants good.

I still think they end up as the dominant player here. Going from a third of Meituan's share to roughly ~50% in under a year is not something you give back to make one quarter's margins look nicer.

Cloud

Ok, now let’s get into the part I actually care about.

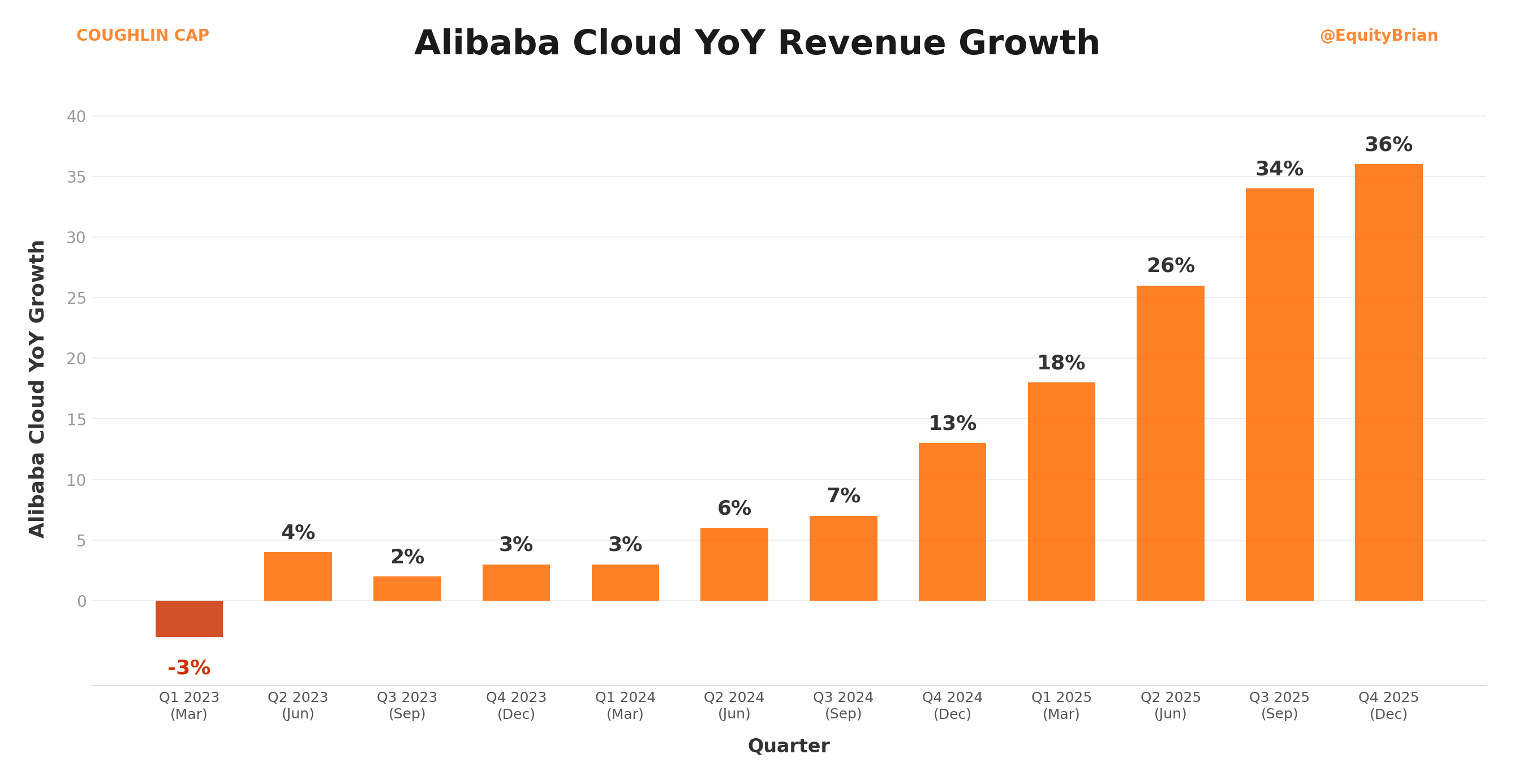

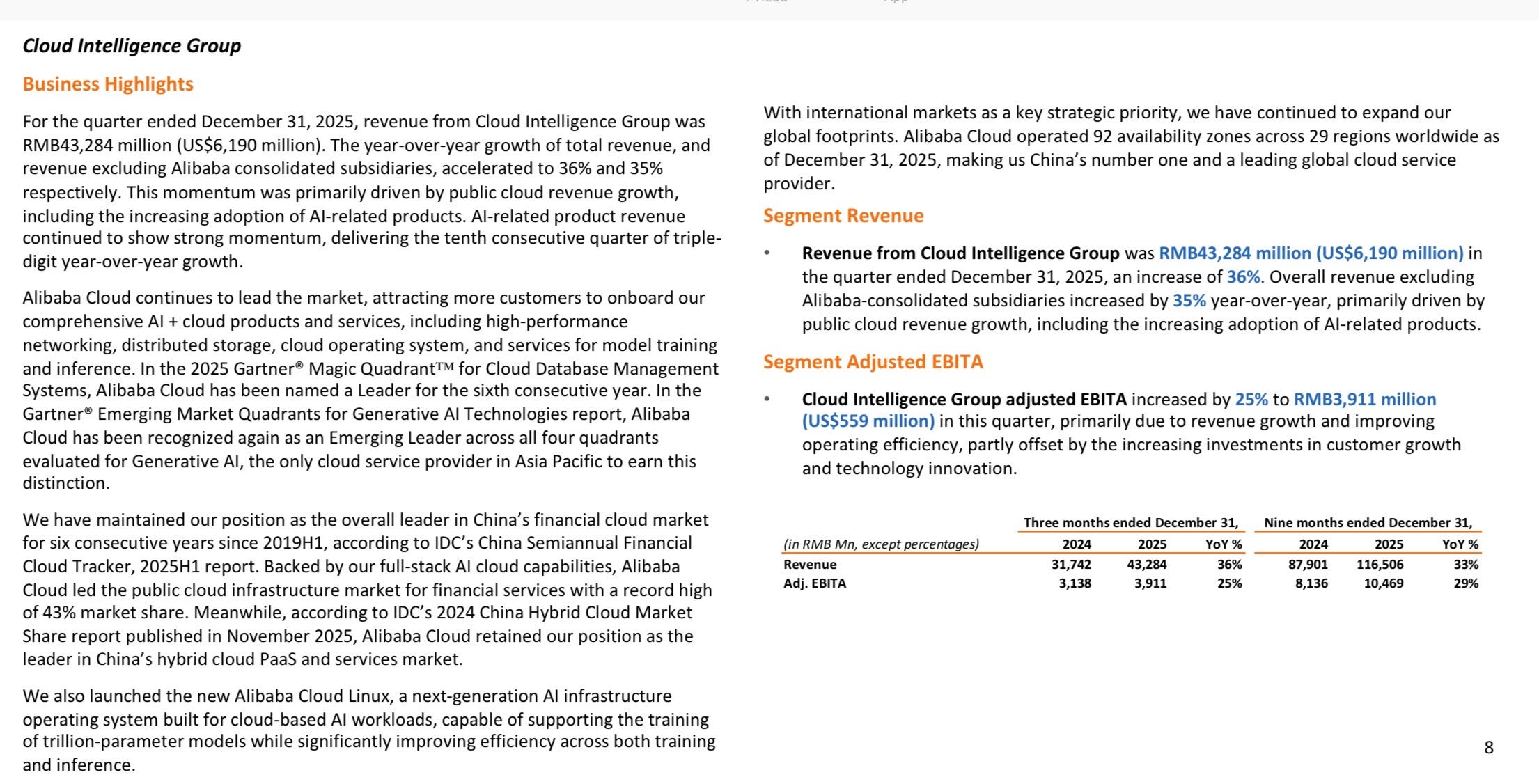

Cloud revenue hit RMB 43.3 billion, up ~36% year-over-year (very impressive). External customer revenue grew ~35%. That’s an acceleration from ~34% last quarter and ~29% the quarter before that.

AI-related product revenue posted triple-digit growth for the tenth consecutive quarter. Cloud EBITA came in at RMB 3.9 billion, up ~25%, with a ~9% margin that held steady while they’re simultaneously pouring capex into capacity expansion.

But the real headline from the call wasn’t the quarterly numbers.