China Tech Looks Cheap Again

J.P. Morgan’s Private Bank put out a piece a couple weeks ago on China tech and AI — The evolving opportunity in China tech and AI.

I wasn’t going to write about it, but after reading it I realized it’s basically a summary of everything I’ve been publishing since last year. So here we are…

Their conclusion: China tech is no longer a macro trade. It’s a stock-picker’s market now. Company execution matters. The AI capex cycle is real. Cloud is inflecting. Valuations don’t reflect any of it.

I mean… yeah. Welcome to the party.

It’s always nice when the big shops catch up. Not because I need the validation, but because when institutional money starts saying what you’ve been saying, people tend to pay a little more attention.

Anyway. There’s good stuff in the report and I want to walk through the parts worth paying attention to, add context where I think they were too conservative, and talk about what they missed entirely.

The Capex Cycle

JPM’s big theme is that AI-related capital expenditure across China’s major tech companies is accelerating and the shift from training workloads to inference-driven demand is improving the economics of the whole thing. More utilization, better pricing power, and a path toward actual operating leverage in cloud.

I’ve been banging this drum for months…

Alibaba’s cloud revenue has re-accelerated into the mid-30% growth range. AI-related cloud products have posted triple-digit growth for ten consecutive quarters. They committed over $50 billion over three years to AI and cloud infrastructure and management keeps hinting the number is going up. And they just laid out a five-year target of $100 billion in annual cloud and AI revenue. That’s roughly a 5x from here. And they’re still rationing GPU access because they can’t deploy servers fast enough.

![[Update] Alibaba](https://substackcdn.com/image/fetch/$s_!Frju!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Ffde61d2f-d3c3-4428-b4b6-8abbf6439a0d_2676x1386.png)

Tencent is spending aggressively too. They dropped RMB 18 billion on AI last year and the guidance suggests that could double in 2027. ByteDance is targeting nearly $25 billion in 2026 capex alone. Between the big four, China’s tech giants are on track to spend over RMB 380 billion a year on AI infrastructure.

JPM frames this as a reinvestment cycle that management teams are increasingly willing to lean into even at the expense of near-term margins. I agree, and I think that’s actually the right move.

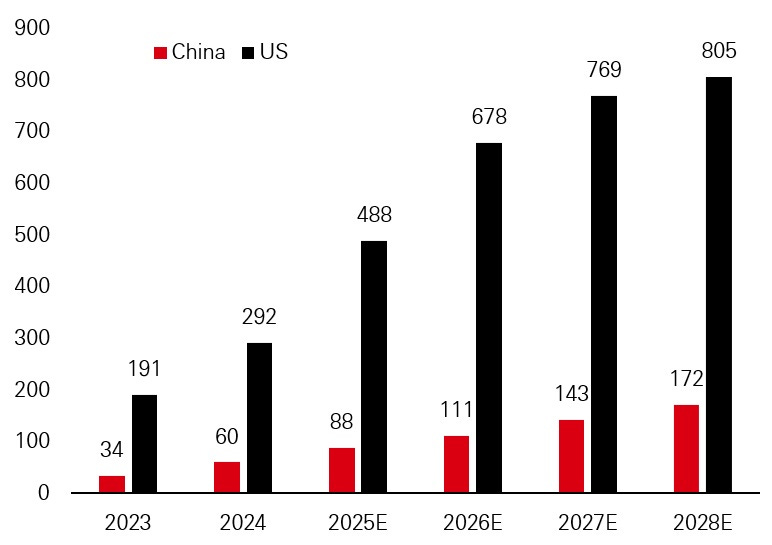

I’ll also note that compared to US hyperscalers, China’s total AI capex is tiny. The US is on track to spend $800 billion+ by 2028. China’s big four combined won’t even crack $200 billion.

And yet the models keep getting better, the cloud revenue keeps accelerating, and they’re doing it at a fraction of the cost. Whether the US is overspending or China is just more efficient is a conversation worth having, but either way, I know which side I’d rather own at these multiples.

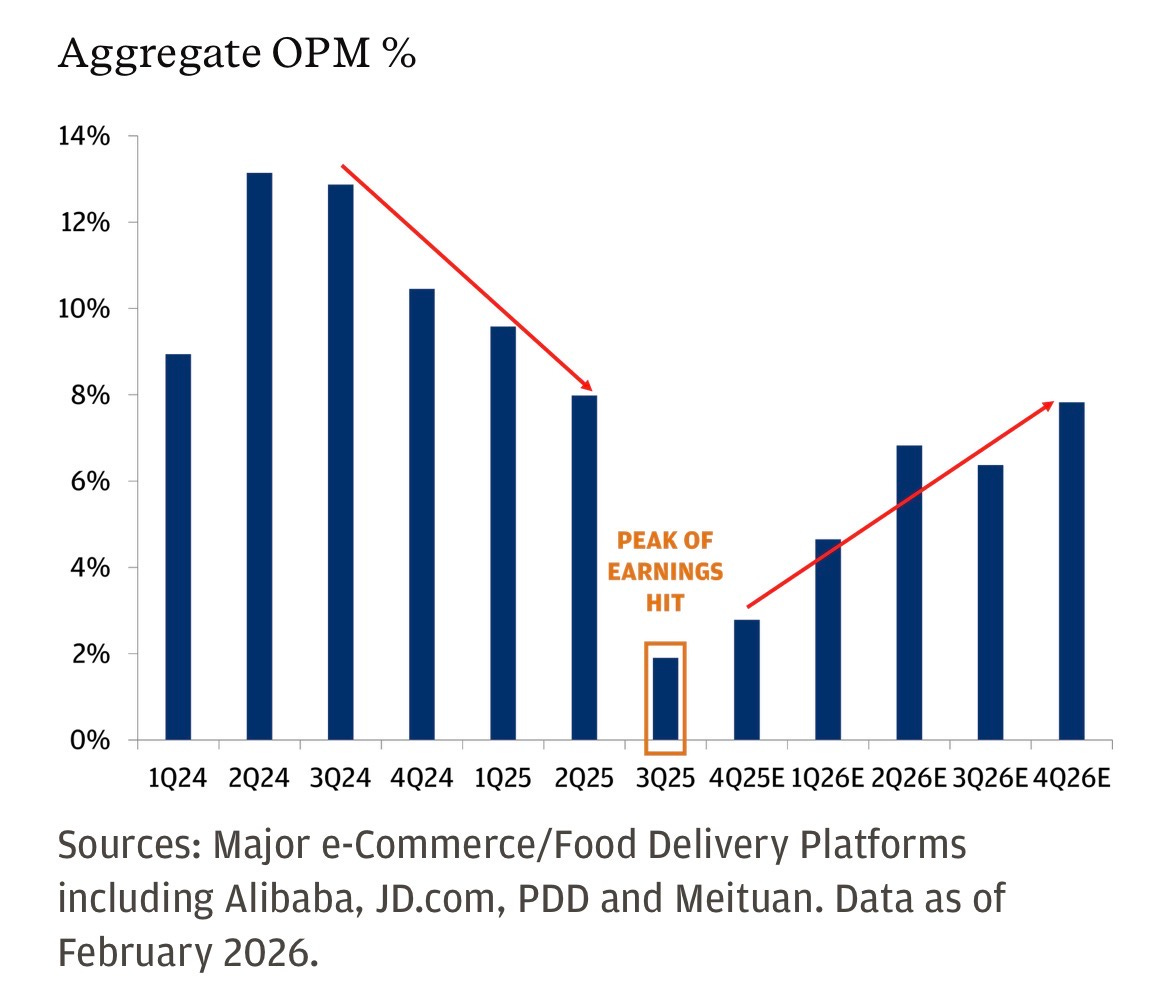

Margins

One of the more honest things in the JPM report is the acknowledgment that profitability is stabilizing, not expanding.