Coupang and the Korea Wealth Effect

The opportunity hiding in Coupang

So we finally have a number. After seven months of watching this data breach hang over everything, Korea’s privacy regulator came out and hit Coupang with a 624.7 billion won fine, about $409 million, the largest data breach penalty in the country’s history.

I’ll be honest, my first reaction was relief. Which is a strange thing to feel when a company you own just caught the biggest fine of its kind ever handed out, but if you’ve followed this saga you probably felt it too. Since last fall, every conversation about Coupang has really been a conversation about the breach, and now that’s finally over. There’s a number, and the number is far better than feared.

The market seemed to feel the same way, because the stock rallied the day the news hit.

Remember what people were tossing around this winter? A possible business suspension, even a forced breakup, with fine estimates running into the billions. What actually showed up works out to about just ~1.4% of revenue. Coupang is obviously appealing, and either way it will land in the Q2 numbers, but this is a bill they pay without breaking stride.

If you're new here, fair warning: I've written about Coupang a lot. There's the original deep dive from last November, the buying opportunity post from January when the breach had everyone panicking, and the Q1 earnings review in May that dealt with all the voucher noise. At this point Coupang is less a stock I cover and more a recurring character on this newsletter. So I won't rehash any of it. The short version is the business came through fine, and if you want the full saga, it's all there.

What’s been bugging me lately is something else entirely.

The breach is mostly behind us now, but the stock still hasn’t really moved on from it. That would be annoying on its own. What makes it harder to dismiss is what’s happening around it: Korea has suddenly become one of the hottest markets in the world, and Coupang has basically sat out the entire move.

Maybe the market is right and Coupang doesn’t deserve to be part of the Korea trade. I get the objection. This isn’t SK Hynix. It doesn’t make memory chips, and nobody is buying Coupang because AI capex is exploding.

But that’s also why it’s interesting to me. If the AI trade is making Korean households richer, if brokerage accounts are up, bonuses are getting paid, and people are feeling a little more comfortable spending, then Coupang should eventually feel some of that?

Maybe not immediately. Maybe not in some clean one-for-one way. But it’s hard for me to believe the company showing up at everyone’s door every day gets zero benefit from a country suddenly having more money.

Here’s the past twelve months performance for context. Korean market (KOSPI) in green, Coupang in blue…

At first, the underperformance mostly just annoyed me because I own the stock and, well, that’s how underperformance works. But now I’m less annoyed and more curious. Coupang is still near the bottom of its own valuation range while the country around it is having one of the strangest/largest wealth booms ever.

I know that sounds dramatic, but I don’t really think it is…

The KOSPI has roughly doubled this year alone, its best half-year on record, on top of a ~75% gain in 2025 that was already its best full year since 1999. SK Hynix is up something like ~340% and just passed Samsung as the most valuable company in Korea for the first time since 2000, a ranking Samsung is disputing, which tells you how close it is. Samsung itself is up around ~200%, and the two of them together now make up more than half of the entire index.

The whole country is levered to AI and the trade is working.

All of that money is going somewhere, and where it’s going is Korean brokerage accounts. Stock ownership in Korea went from about 6 million people in 2019 to over 14.5 million now, and JPMorgan estimates household stock wealth has grown by more than 1,000 trillion won this year. That’s a quadrillion won of gains in a country of 51 million people.

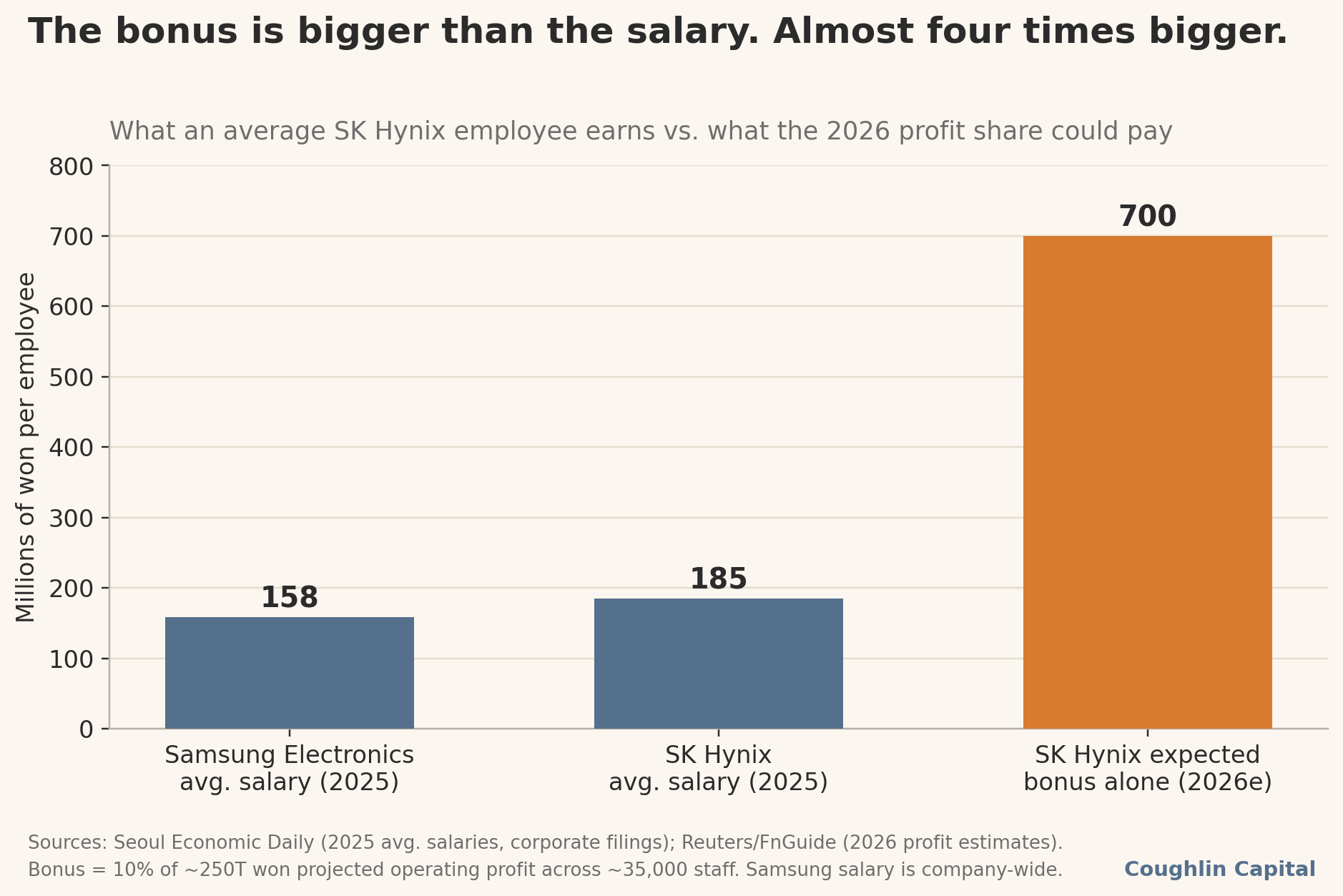

Then there’s the part that almost sounds made up. SK Hynix agreed to pay employees ~10% of operating profit as bonuses with no cap, which on this year’s expected profits comes out to roughly 700 million won per employee, about $460,000 on average.

Samsung’s chip workers spent months threatening strikes until they got a deal of their own, an average payout somewhere around $340,000.

It’s reached the point where the Korean press reports SK Hynix engineers have become the most sought-after bachelors in the country’s matchmaking market, suddenly ranked alongside doctors and lawyers, and the Bank of Korea is warning about bonus checks stoking inflation because card spending near the chip campuses in Gyeonggi is running visibly hotter than the rest of the country.

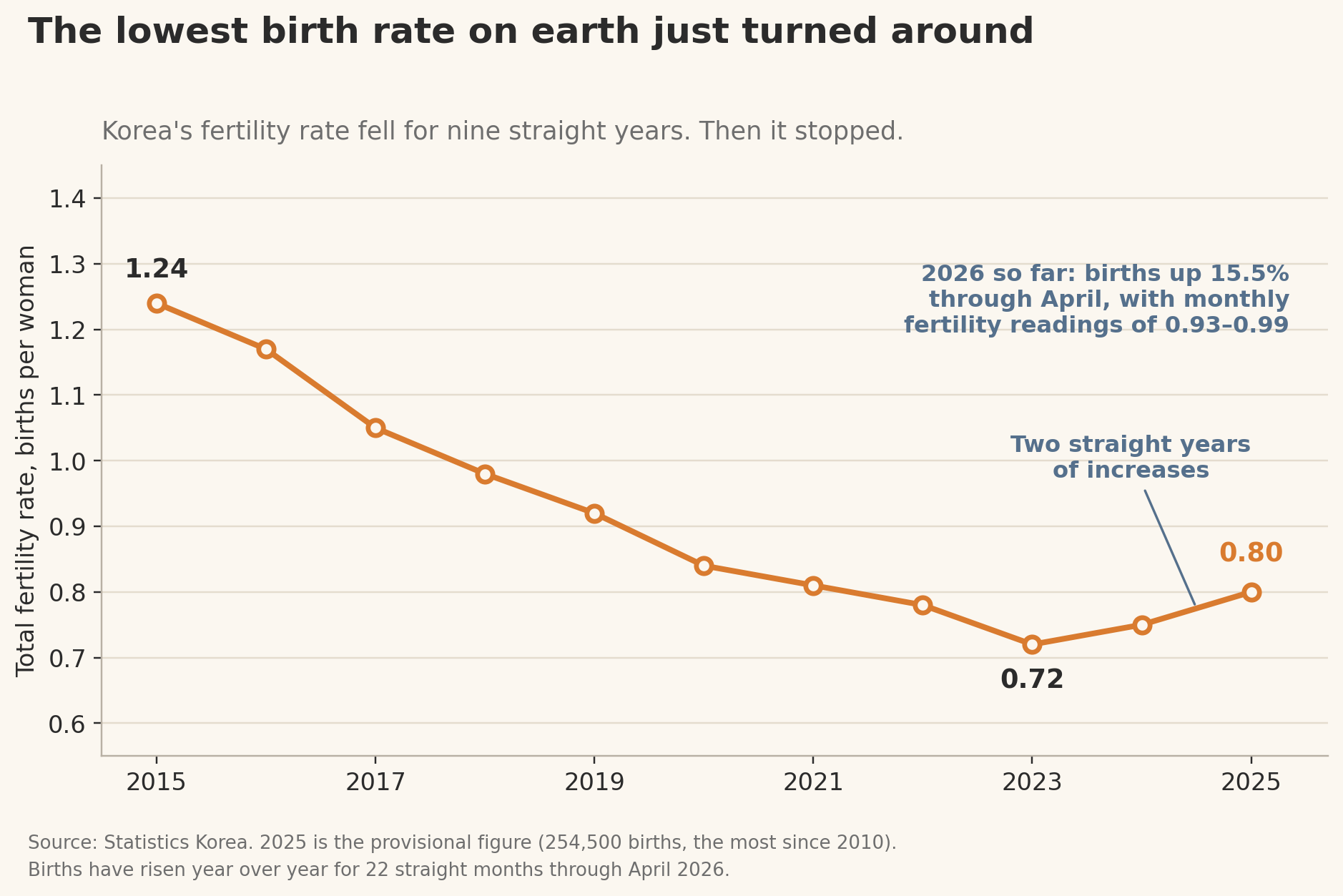

And apparently the matchmaking is working, because Korea is having babies again.

And again, this is Korea. Basically the global example everyone uses when they wants to talk about collapsing birth rates and long-term consumption problems. Births have now risen year over year for 21 straight months. March was up 19.4%, the biggest jump in over three decades, and the monthly fertility rate touched 0.99 in January, nearly back to a whole baby per woman!

Marriages are also at their highest level since 2018, and in Korea marriage is basically a two-to-three year leading indicator of births, so this probably isn’t done.

To be fair, the rebound started in mid-2024, before the rally, and demographers mostly chalk it up to post-COVID catch-up weddings and a big cohort hitting their early thirties, not the KOSPI. Fine. But a country full of newly minted millionaires can’t be bad for weddings, and every wedding and baby is a future Coupang household.

Overnight diapers were literally the original Rocket delivery pitch. The oldest knock on Coupang has always been that it’s the best retailer in a shrinking country, and for the first time in nearly a decade that curve is bending the other way.

So you’ve got millions of newly flush households, tens of thousands of workers getting life-changing bonuses, and now more weddings and babies on top of it. Somebody is going to sell those people more stuff.

My money, literally, is on the company that already sells Korea most of its stuff.

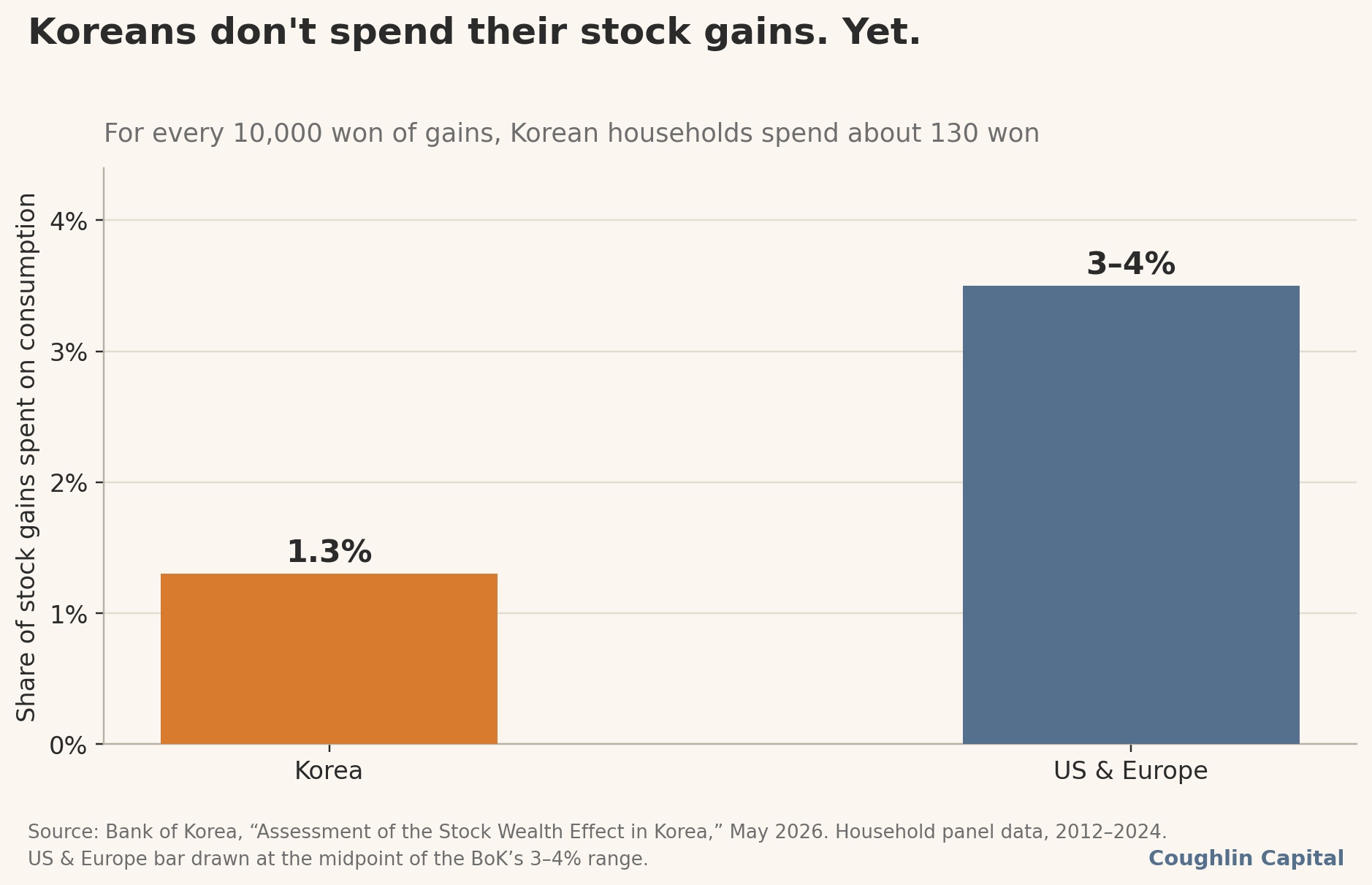

Now the pushback, because there’s a real one. Koreans historically don’t spend stock gains the way Americans do. The Bank of Korea’s own research says only about 1.3% of equity gains become consumption there, versus 3 to 4% in the US, because Korean wealth traditionally gets parked in apartments rather than spent at the mall.

And the spending that has shown up so far skews rich: department stores up 15%, luxury watches flying, jewelry up triple digits at stores near the chip campuses. The old knock, and I’ve leaned on it myself, is that Coupang sells diapers and bottled water, not Rolexes, so a luxury-led boom mostly passes it by.

Except that line is a couple of years out of date.

Coupang bought Farfetch for $500 million in early 2024, back when everyone treated the deal as a strange distressed detour, and has since dragged it to roughly breakeven. Then came R.Lux, the luxury vertical that started with high-end beauty in late 2024 and folded in Farfetch’s entire catalog about a year ago. Today it carries something like 1,400 luxury labels, watches and fine jewelry included, with import taxes baked into the price and WOW perks attached.

The timing worked out better than anyone could have planned, because Korea’s homegrown luxury platforms spent the past two years collapsing, Balaan into court protection, Trenbe and Must’It with revenue cut in half, right as the biggest per-capita luxury spenders on earth minted a fresh class of rich people. I won’t pretend R.Lux is about to rival the marble halls at Shinsegae, since most of this boom’s luxury money is still walking through department store doors. But Coupang built a net for high-end spending right before the fish showed up, which is not nothing.

Beyond the luxury angle, two more things keep me from letting the bear case kill the idea.

First, even the stingy 1.3% applied to a quadrillion won is about $28 billion of new spending, which happens to be JPMorgan’s estimate as well. Coupang’s Korean revenue runs around $29 to 30 billion, so it doesn’t need to catch much of that flow for the numbers to move. If it captures even a modest slice, roughly in line with its share of overall Korean consumption, you’re talking about a billion or two of extra revenue landing on a network that’s already built and paid for.

Incremental volume at Coupang shouldn’t cost what average volume costs. The network is already built, and more volume running through that network should come with better economics than the average order. On a company that earned about $200 million in net income last year, even a billion or two of extra high-quality revenue would change how the business looks pretty quickly. It’s the difference between the market yawning and the market repricing the stock.

Second, the 1.3% figure was measured in a world where every Korean windfall went into real estate, and the government is actively closing that door. The lending curbs and cooling measures rolling out right now exist specifically to keep this boom from becoming another housing bubble, and if the traditional destination for windfalls is blocked, more of the money leaks into daily life.

It’s also worth noting that the people making this money skew under 50, which is exactly the demographic that already runs its entire life through a WOW membership.

Is there any evidence yet, or is this all just me connecting dots? A little, and I’d call it early evidence with the emphasis on early.

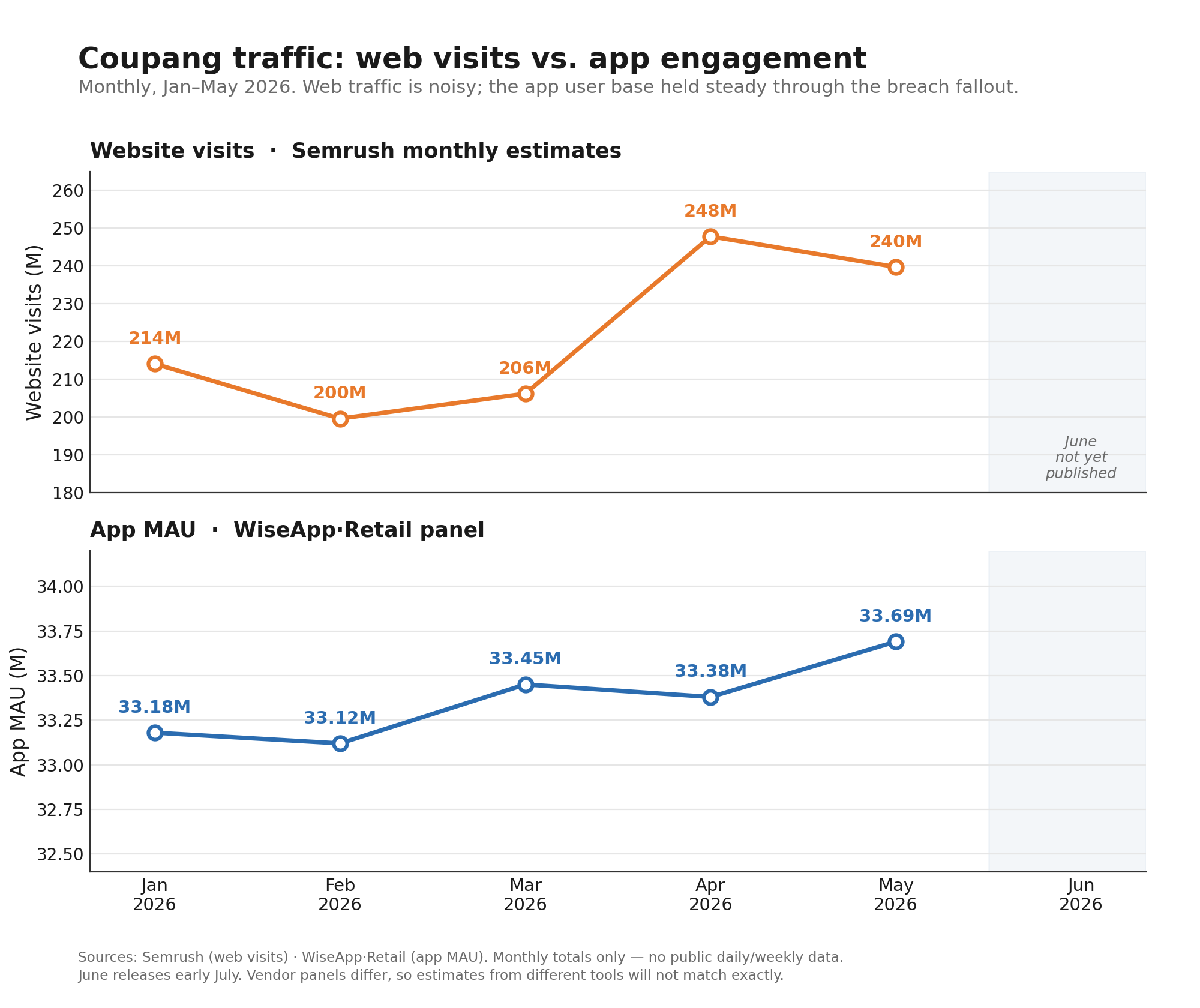

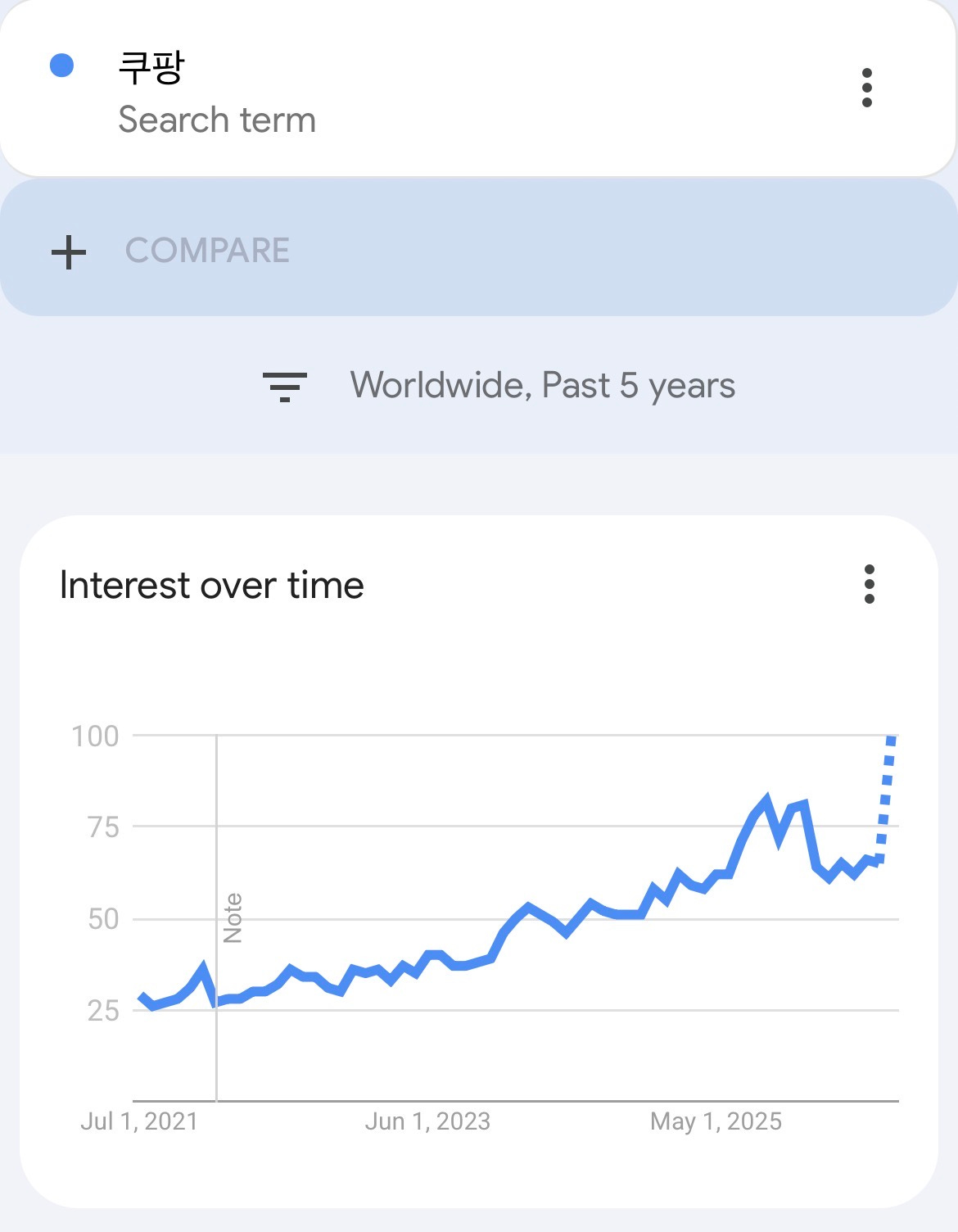

Coupang’s app user base held basically flat through the worst months of the breach and then made a new high in May at about 33.7 million monthly users. Web visits jumped from around 200 million in February to the 240 to 250 million range this spring. And Google search interest for 쿠팡 (Coupang) has been climbing for years but just spiked to a five-year high in the latest reading.

I’m not going to pretend a few months of third-party panel data proves a macro thesis, and some of that recovery is surely just people drifting back after the breach scare. But if Korean consumers were pulling back, or if the breach had done lasting damage, engagement is exactly where the cracks would show up first, and instead everything is pointed the same direction.

It’s not proof. It’s just what you’d hope to see if you were right, and so far it’s what we’re seeing.

To be clear about what I’m claiming here: the wealth effect is not my Coupang thesis.

The thesis is what it’s always been, an untouchable logistics network compounding year after year, now trading near the bottom of its range because of a scandal that just formally ended. The wealth effect is the free option sitting on top. If Korean consumption inflects, Coupang is the single most obvious beneficiary and nobody is modeling it, and if it doesn’t, I still own the best retailer in Korea at a price I like.

But it is a strange thing to watch. A country mints a quadrillion won in stock gains, the central bank starts worrying about bonus checks stoking inflation, and the dominant consumption platform in that country still trades like the breach never ended…

One of those two things is wrong. We’ll find out which sooner than later.

I publish this kind of thing most weeks. Subscribing is free, but paid unlocks the full archive of nearly 200 posts, plus every new writeup and research report going forward.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Nice. I am writing about Korea and my piece will come out on Monday.

I like the way you shifted the question from “is the breach over?” to “what second-order signal is the market still missing?”

The Korea wealth-effect angle is interesting because Coupang is not the obvious AI trade, but it may still sit downstream of the same capital cycle. If semiconductor wealth, bonuses, brokerage gains, weddings, and births are all moving in the right direction, the question becomes whether that eventually shows up in category mix, advertising intensity, R.Lux/Farfetch, or higher-frequency household spend.

Curious whether you think the first visible signal would show up in GMV growth, margin mix, or management commentary before the market really connects the dots.