Tencent (0700.HK): The Best Business Nobody Wants

Tencent Holdings — $TCEHY $0700.HK

Tencent is one of the best businesses in the world. I don’t think that’s a controversial thing to say.

It runs WeChat, and calling it a messaging app really undersells what it is. People message on it, pay with it, hail rides, order food, book doctor appointments, run entire small businesses, all without ever leaving it. More than a billion people open it every single day.

“WeChat has one of the widest moats I’ve ever seen.”

— John Huber, Saber Capital

There’s no real western equivalent and there isn’t a second app in China that comes close. That kind of position doesn’t get competed away. People have been trying to dislodge it for fifteen years and nobody’s gotten anywhere.

On top of that you’ve got the largest gaming business on the planet, an advertising machine that’s accelerating, a cloud and fintech arm, and a giant portfolio of stakes in other companies. The whole thing throws off enormous amounts of cash and earns very high returns on the capital it puts to work. This is about as high quality as large-cap tech gets, anywhere in the world.

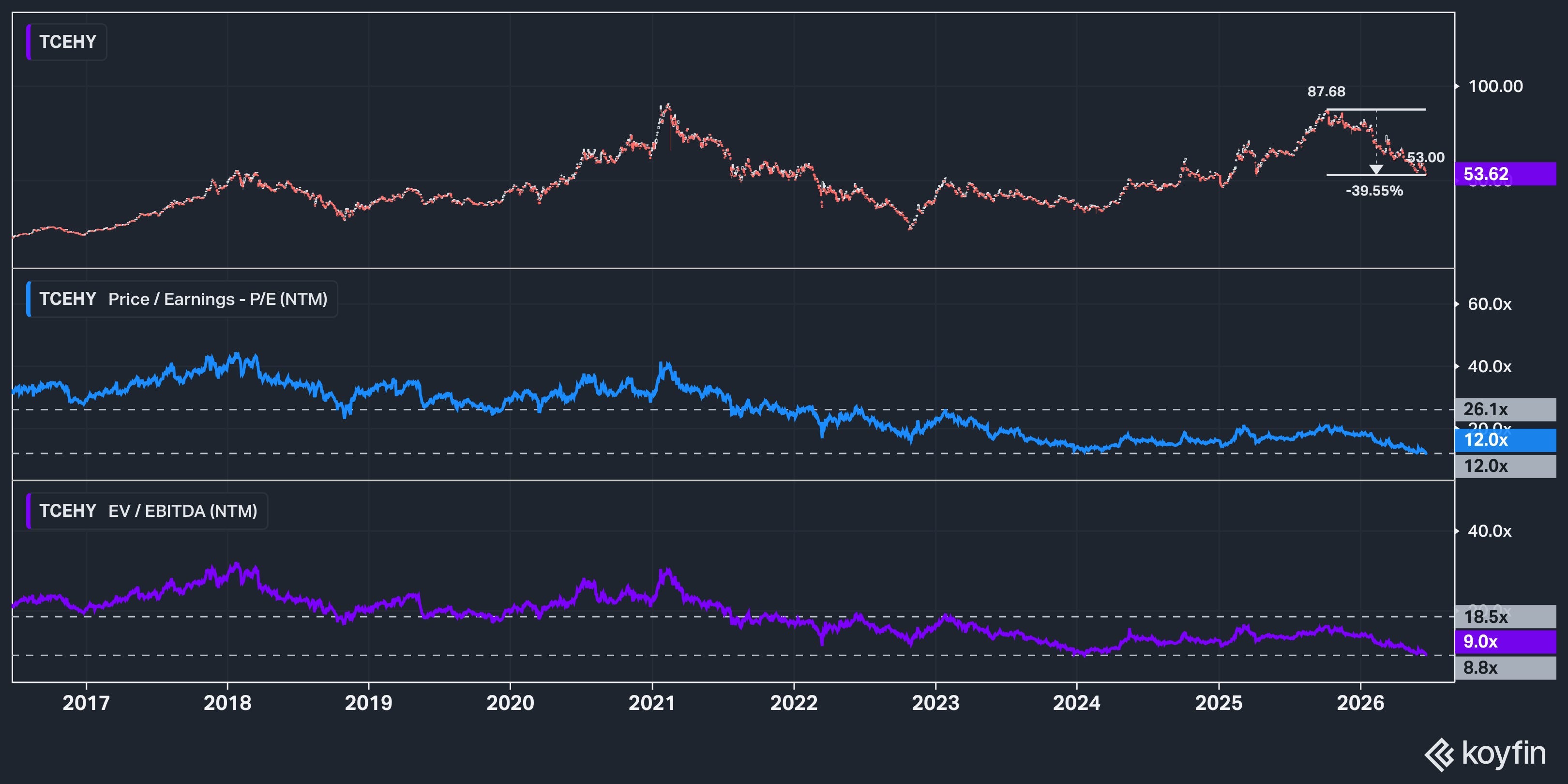

And the stock is sitting at 52-week lows. Down almost 40% from its October highs. Trading around ~12x forward earnings and ~9x EV/EBITDA.

I keep staring at this and I struggle to make it make sense.

Why is it so cheap?

I think it starts with the market Tencent trades in, but I want to be careful with how I frame this, because it’s not the same as 2022 or 2023.

Back then the whole China complex was basically radioactive. Nobody wanted anything. Mainland stocks, Hong Kong stocks, ADRs, internet platforms, consumer names, property-adjacent names, all of it got thrown into the same uninvestable bucket.

This time is a little different.

Mainland China stocks have actually been acting pretty well. A-shares have rallied, AI names have ripped, and there’s plenty of speculative energy in parts of the domestic market. Some of the mainland AI stuff honestly looks quite frothy at the moment. Money is chasing semiconductors, robotics, AI infrastructure, domestic replacement, and anything that smells like policy support.

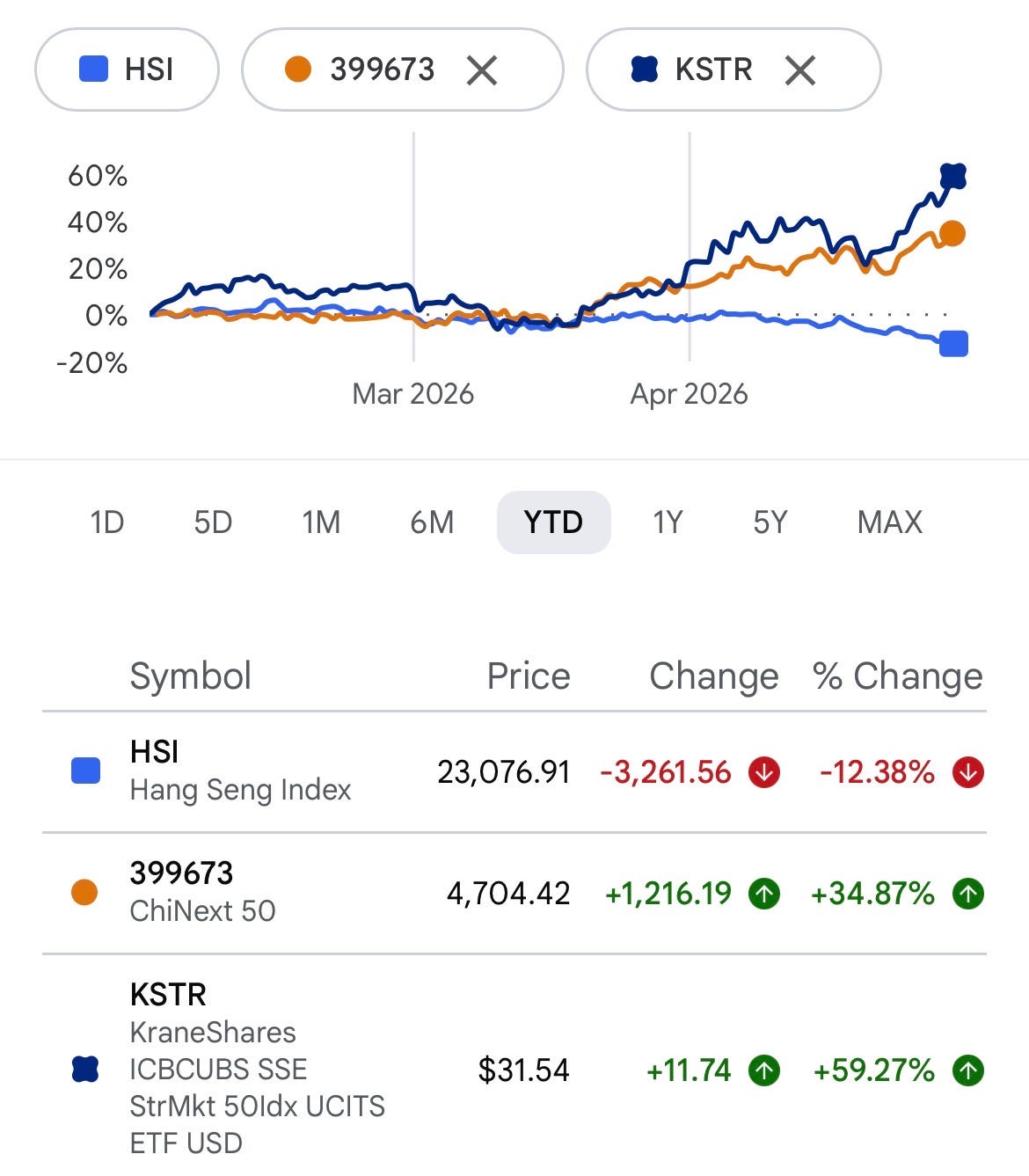

Hong Kong, on the other hand, has been left for dead.

Tencent, Alibaba, Meituan, Kuaishou, JD, and the rest of the group have been trading like investors want nothing to do with them. Some of that is macro. China’s economy has been sluggish and the consumer recovery hasn’t been nearly as strong as people hoped, myself included.

Property is still a drag, confidence is weak, and consumers remain very cautious.

I do think China eventually comes out of this, though more stimulus is probably needed. Right now the economy feels stuck in this odd half-recovery where certain parts are fine, certain parts are even hot, and the consumer still looks tired.

I publish this kind of thing most weeks. Subscribing is free, but paid unlocks the full archive of nearly 200 posts, plus every new writeup and research report going forward.

Then there’s the flow problem.

Money that might normally find its way into Hong Kong internet is getting pulled toward mainland AI instead. A domestic investor can look at a semiconductor name ripping in Shanghai or Shenzhen, then look at Tencent grinding lower in Hong Kong, and the short-term choice becomes pretty obvious.

Why sit in a cheap mega-cap internet stock when the party is happening somewhere else?

I get it.

But these rotations always feel permanent while they’re happening. The hated group gets cheaper, the crowded group gets more crowded. Then at some point the easy money in the hot stuff gets made, the valuation gap gets stupid, and people start looking around again.

Tencent is on the wrong side of that rotation right now. That’s painful if you own it. It’s also why the opportunity exists.

The other piece is the AI perception thing.

There’s been a narrative for a while that Tencent is behind in AI. And to be fair, a year ago that had some truth to it. Tencent was slow and cautious at the start of the AI boom while Alibaba, ByteDance, DeepSeek, Baidu, Moonshot, and a bunch of others were moving as fast as possible to cement their place as AI leaders

I don’t think that’s a fair read anymore.

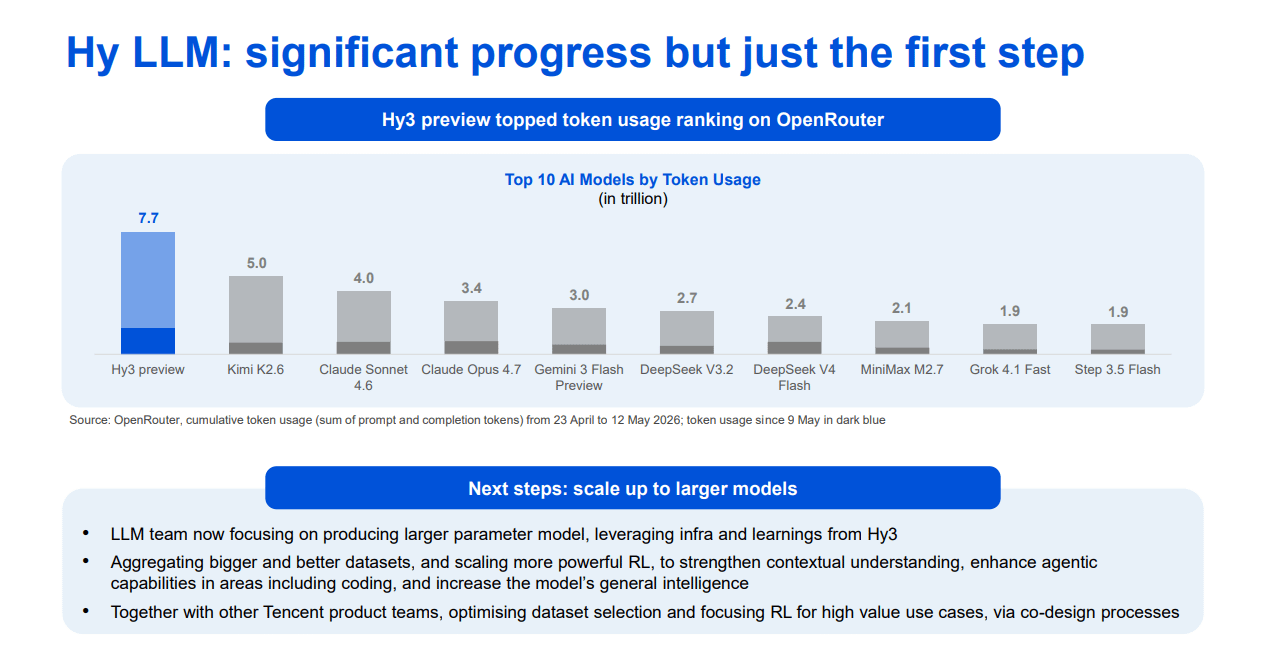

Tencent hired Yao Shunyu, a former OpenAI researcher, as its Chief AI Scientist last year, and reorganized the whole AI effort around Hunyuan. Then they launched the Hy3 preview model in April, and management has been clear that it’s now good enough to use across real products.

It’s been the top-ranked model on OpenRouter by token usage since late April, which is about as real-world a measure of developer adoption as you’ll find.

I’m not going to pretend I can tell you which Chinese model will be the best two years from now. But I also don’t think that’s really the Tencent story.

The advantage for Tencent is where the AI can go. They already own the place where people spend their time. That’s the part I care about.

It reminds me a little of Apple. Everyone has spent the last couple of years yelling that Apple is behind in AI, and maybe that’s true. But Apple has the device in your pocket, the operating system, the default apps, the payments layer, and the customer relationship. Being late matters a lot less when you already control the surface area.

Tencent has a version of that in China through WeChat.

Keep reading with a 7-day free trial

Subscribe to Coughlin Cap to keep reading this post and get 7 days of free access to the full post archives.