Burford Without YPF

$BUR

The market took a baseball bat to Burford Capital last week…

The stock got crushed after the YPF case went the wrong way in court. By the close, the market had basically written off the whole company, which honestly isn’t that surprising when YPF was the reason most investors I know owned it in the first place.

When your biggest catalyst disappears overnight, the stock is going to get hit hard. That part is pretty obvious.

What I’m less sure about is whether the selloff went too far.

I’m not saying YPF didn’t matter. You don’t lose half your market cap in a day over something that doesn’t matter. But Burford without YPF is still a real business.

Messy, yes. Hard to value, yes. Lumpy, absolutely. But still a real business.

I actually used to own this stock. I sold about a year ago, which in hindsight turned out to be one of the luckier exits I’ve had. But I’ve followed the company for a while and I think what happened on Friday is worth walking through for people who are either seeing this for the first time or trying to figure out what to do with their shares.

A lot of people know Burford through the YPF case, but the company itself is much broader than that.

At its core, Burford is a litigation finance business. A company has a legal claim that may be worth a lot someday, but it could take years to play out and cost a fortune to pursue. Burford provides the capital and takes a share of the outcome if things go their way.

Think of it like private equity for lawsuits.

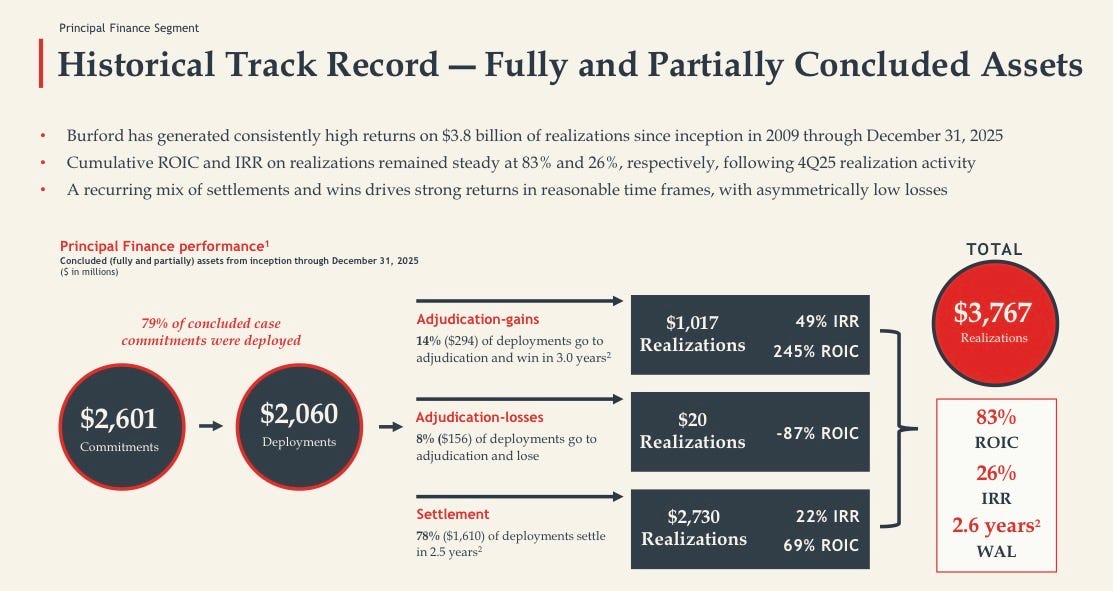

Their clients are big. They’ve received financing inquiries from 94 of the 100 largest U.S. law firms. The economics have been genuinely strong. Concluded cases have delivered an average 83% return on invested capital with a 26% IRR.

Most cases settle rather than going to trial and case outcomes are generally uncorrelated with broader markets.

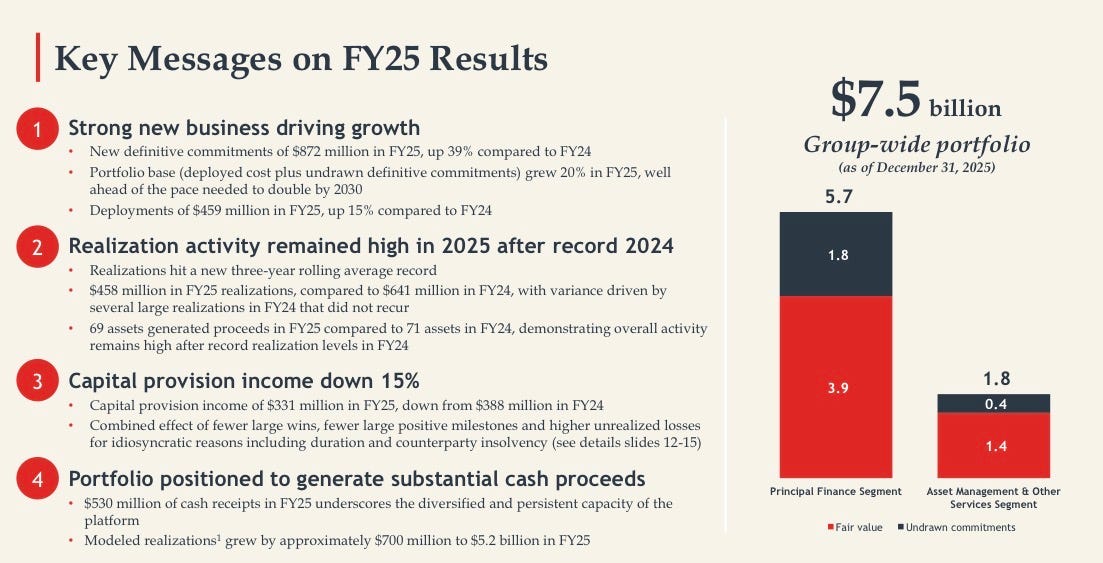

Christopher Bogart and Jonathan Molot, both attorneys, founded the company in 2009 and still run it. They collectively own about 10% of the stock. They’ve grown from a $130 million fund to a $7.5 billion portfolio.

The business generated over $500 million in cash receipts in 2025. Rolling three-year return on tangible common equity of 13%. There’s also an asset management arm managing about $2 billion of external capital and earning fees on top of all the direct investing.

It’s a real business. But the thing that made Burford a household name on fintwit, and the thing that drove most of the stock’s volatility over the past several years, was one single massive case.