A Microcap at 3x EBITDA, Growing >20%, 90% Insider-Owned

A Rare Asymmetric Opportunity With An Unusual Share Price To Valuation Disconnection

This is a first for the newsletter. I’ve never run a guest post before, but Mark Colin earned the real estate.

I’ve been watching Mark work on Meridian Holdings (MRDN) on X for a while now. The stock is down about 80% from where insiders effectively valued it in the 2024 merger. Since then, it’s gone through a reverse split, a CEO departure, and a full rebrand.

Mark hasn’t flinched. In fact, he’s been adding every week.

I know a lot of people will look at that and think he’s throwing good money after bad, but his argument is pretty simple: the company is fundamentally stronger than it was a year ago and the share price doesn’t reflect that.

He’s betting the execution catches up. Or, as he put it to me, he’ll look back at these prices as a gift... or he’ll be living down by the river.

That kind of conviction through that kind of pain/uncertainty is rare. Most people I come across can barely stay interested in a stock for more than a few months.

I don’t know MRDN as well as Mark does, but I’ve looked at it enough to find it interesting. It’s a profitable, insider-heavy gaming company trading at a fraction of its peers with some real catalysts ahead. But I haven’t done the deep work myself. Mark has. And I’ve looked at enough of his research to trust that he’s the right person to walk you through it.

What follows is entirely Mark’s work — his research, his position, his money on the line. I’m just giving him the space to lay it out. If you’d like to see more guest posts like this, let me know.

This post is free for everyone. If you want to support the work and get access to all my research, ongoing coverage of every name I follow, and full portfolio visibility, consider going paid.

Some recent work:

![[Update] BYD (BYDDY)](https://substackcdn.com/image/fetch/$s_!YXda!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fc43fccfc-c4fe-4244-9537-3a52f510e5de_1979x1070.png)

Meridian Holdings (Nasdaq: MRDN) — A Rare Asymmetric Opportunity With An Unusual Share Price To Valuation Disconnection

Meridian Holdings, after executing for decades, has become a high growth and international diversified gaming powerhouse with the necessary proprietary AI technology and synergistic acquisitions required to scale globally, increase revenue, and expand margins. They are a B2B and B2C industry leader with over 1200 employees, transforming the sports-betting and i-gaming industry with their omni-channel ecosystem made up of complimentary companies now reaching 20+ jurisdictions across five continents in regulated or supported markets.

Table of Contents

1. Story and Valuation

2. The Omni-Channel Ecosystem

3. Execution and Skin-In-The-Game

4. Profitability

5. Near-Term Catalysts

6. Global TAM

7. World Cup Brand Opportunity

8. A Long History of Execution and Profitability

9. Global Footprint, Moats, and Long-Term Sector Catalysts

10. Meridianbet’s AI Tech Advantage

11. Player Acquisition Cost Advantage

12. The Content Edge: Expanse Studios

13. Subsidiaries: RKings, MexPlay, and CFAC

14. Proven Leadership with Integrity

15. Risks

16. Disclosure

1.) Story and Valuation

In April of 2024, instead of selling their company to a larger operator, Meridianbet leadership chose to go public (Nasdaq) via a reverse merger with Golden Matrix Group. After years of negotiations they settled on a value of $330 million and accepted the majority of the acquisition compensation in shares at an approximate value of $35 per share (adjusted) demonstrating deep confidence in their ability to continue scaling into new markets, aligning themselves with shareholders, and backing up the CEO’s bold statement of “setting up for the next hundred years”.

Meridianbet and its subsidiary Expanse Studio’s value of $330 million, combined with Golden Matrix, GM-AG, RKings, and MexPlay’s value of $80 million equalled a combined value of $410 million.

This was before two of their more recent acquisitions, CFAC and Fairbet, as well as prior several new valuable licenses including a $6 million Federal Brazil Lic. Add in recent growth of all 6 subsidiaries with a projected annual revenue of nearly $200 million, combined with an industry rare .86 debt ratio with over $18 million in cash, and you have roughly a half billion dollar company valuation.

After the recent share price walked down to $6.88, the company market cap has dropped from nearly $500 mil to $86 million. In my opinion, this is a valuation disconnection that screams “undervalued”. A rare asymmetric set up. It is important to keep in mind, past dilution and debt were not operational but rather acquisition driven, the majority from the Meridianbet merger, to create the ability for growth in the sector for decades to come.

2.) The Omni-Channel Ecosystem

MRDN Holdings is not a one-trick-pony but an entire omni-channel ecosystem including:

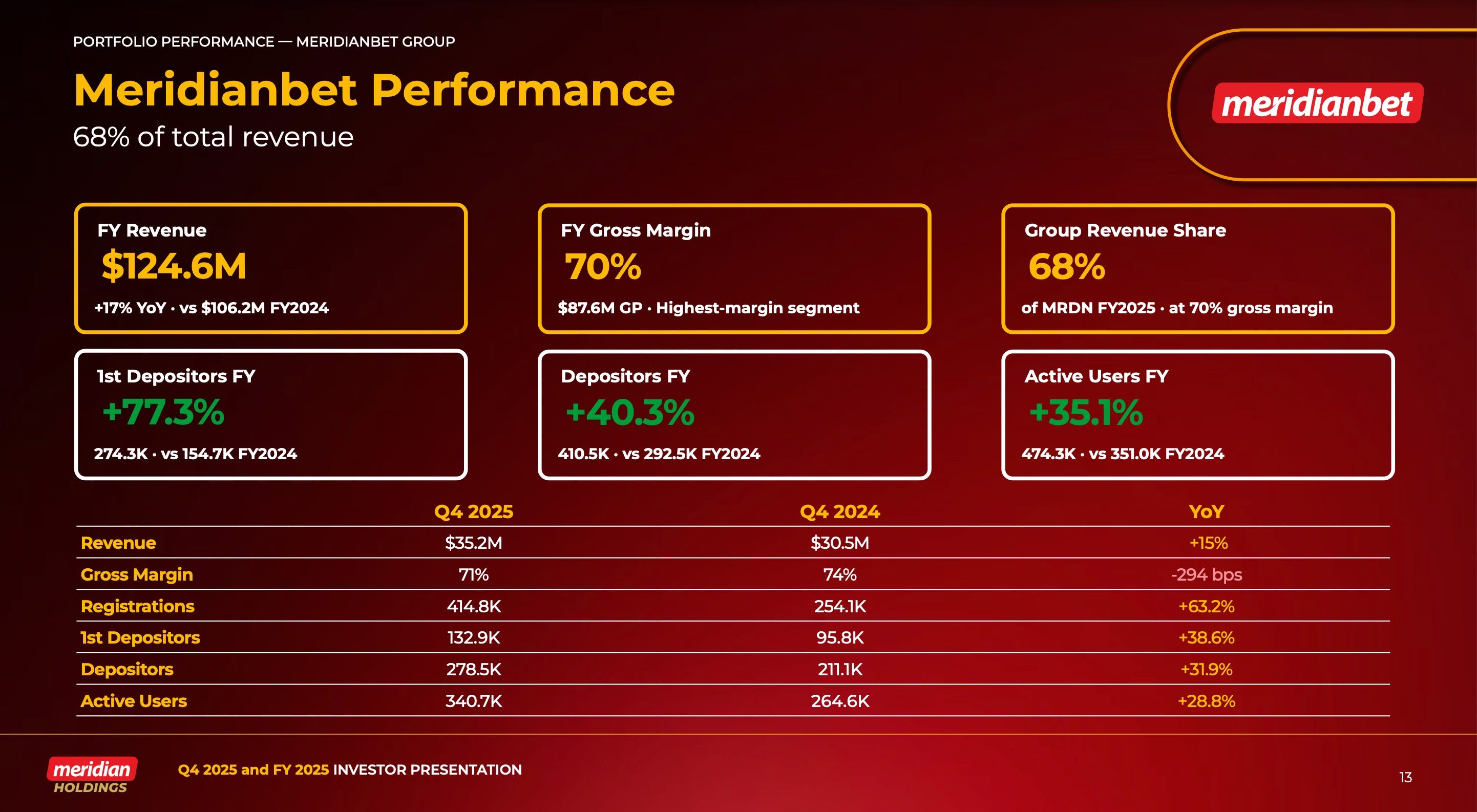

Meridianbet: Its legendary flagship brand and a leading operator in 18+ regulated markets across Europe, Africa, and South America.

RKings & CFAC: Specialists in high-volume UK-based digital competitions and Australian trade promotion lotteries.

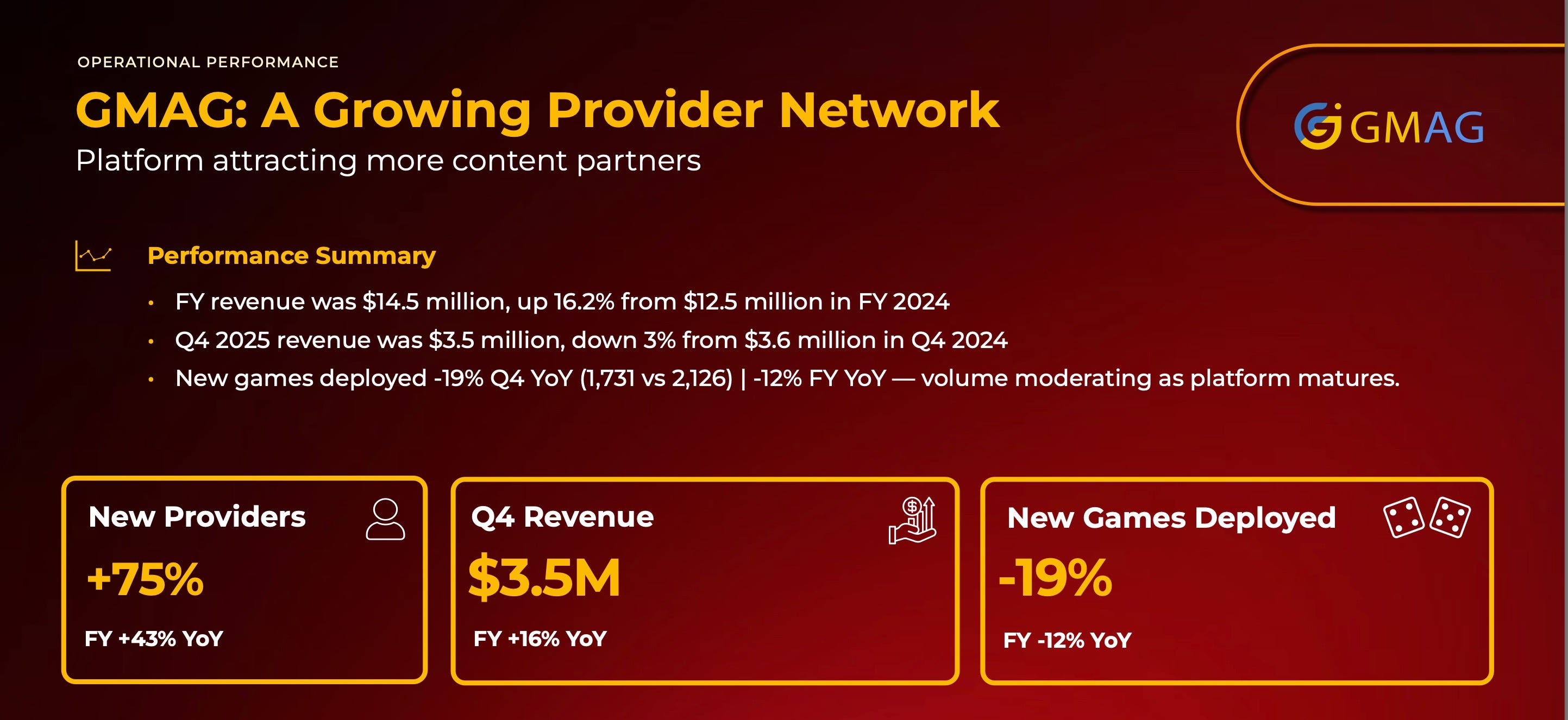

GMAG: A core B2B segment providing advanced iGaming platform solutions and “white label” solutions.

Expanse Studios: A top-tier proprietary game developer fueling growth with over 70 original titles and growing at over 400% annually.

MexPlay: A fully regulated online casino and sportsbook capturing the expanding Mexican market.

3.) Execution and Skin-In-The-Game

With a proven 27-year history of private execution, Meridianbet, along with its decentralized accretive subsidiaries, are now Nasdaq listed and operating with dedicated CEOs and founders who have meaningful skin-in-the-game (nearly 90%) creating multiple growing and diversified B2B and B2C revenue streams.

Meridian Holdings is built for the future of digital entertainment. With years of double digit growth, record revenues and an aggressive vision for expansion into Brazil and other high-growth territories, MRDN represents a uniquely positioned opportunity for investors seeking an established operator with cutting-edge technological advantages in an early and enduring sector driven by global industry tailwinds.

Consider:

Consistent history of double digit growth

Industry low 0.82 debt ratio with one-offs in the rear view

Conservatively estimated to generate $210 - $220+ million in 2026

12.5 million OS shares x $6.88 = market cap of $86 million

Trading under 0.4X revenue in a 2.5X+ average sector

At 2.5X, MRDN would have a $500 million market cap — or ~$40/share — representing nearly 600% upside

Share Structure:

12.5 million OS shares

~90% insider ownership = 1.2 million shares remaining

4% institutional = ~700k retail shares

Remove 2 top shareholders (~200k shares) = ~500k shares actually available

A single large investor could buy the entire remaining float for under $4 million

In our current market, micro/small-caps are trading on sentiment and momentum rather than fundamentals. A single large investor could buy the entire remaining open float for under $4 million. That is not a huge investment. Whoever the first large investor is, they are certainly going to pay far less than the second, third, and following investors as Meridian Holdings keeps expanding and executing.

With such limited shares available, any visibility or discovery will likely cause MRDN share price to run-up quickly. Any substantial Brazil Market capture, profitability, or an earnings beat could trigger MRDN to re-rate and rip similar to RSI that ran $2 to $20 when they turned profitable after years of consolidation while executing.

With a half dozen decentralized subsidiaries operating in over 20 jurisdictions with multiple diverse B2B and B2C revenues streams and currencies, I won’t even begin to attempt to model a valuation based on DCF or rear view numbers as they can be reverse engineered and modeled to support any thesis.

I will point out the company and all its subsidiaries are growing, paying down the majority of acquisition debt, and after a long period of share price consolidation their disruptive tech is being adopted as the company turns profitable.

4.) Profitability

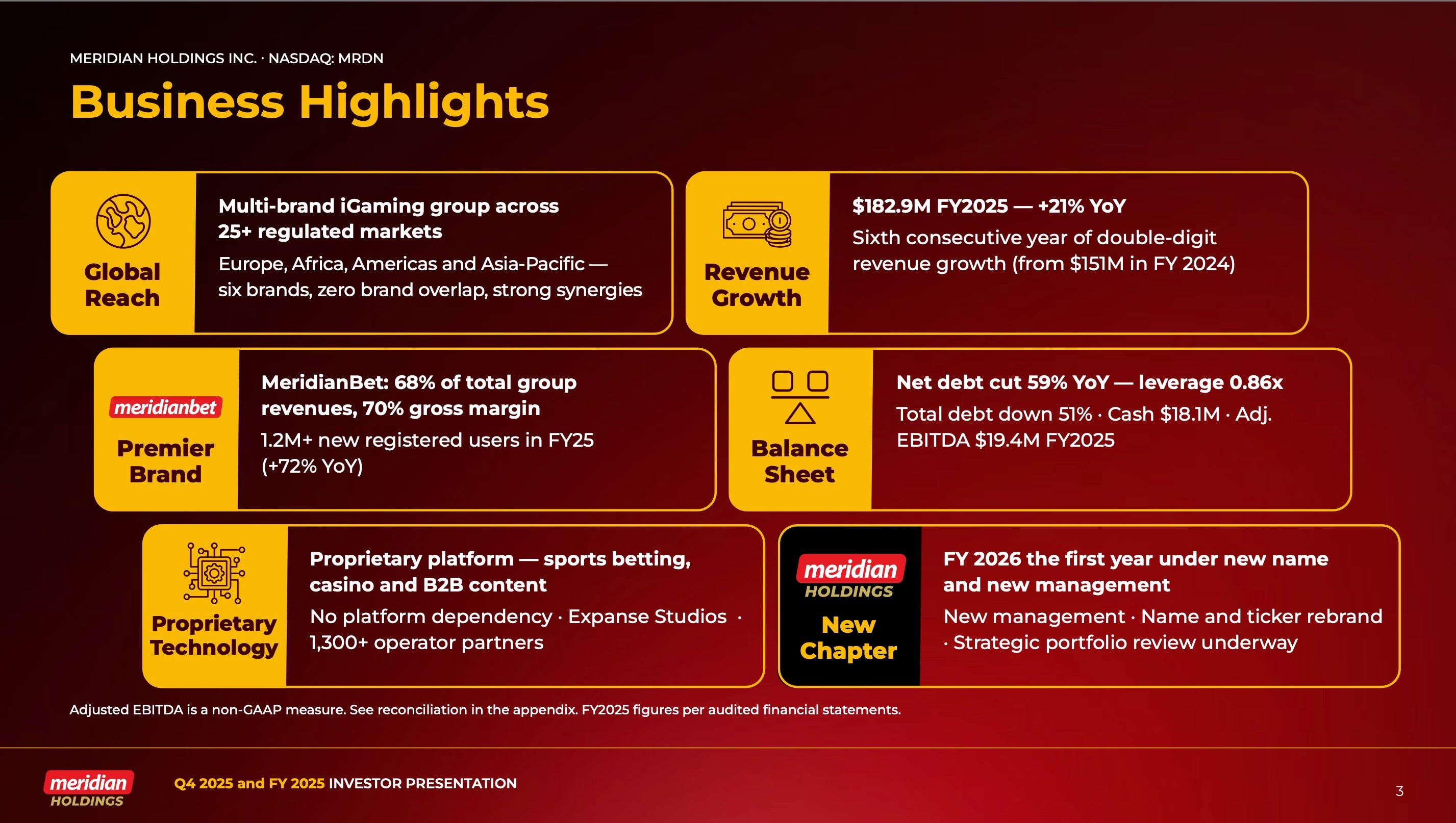

Meridian Holdings was actually profitable last quarter reporting record Q4 2025 revenue of $49.6 million, adjusted net income of $3.4 million or $0.29 per share, full-year 2025 revenue of $182.9 million, up 21% YoY and beating analyst expectations.

Their balance sheet loss was due to US GAAP principles that required Meridian Holdings to write off a huge 88.4 million “Goodwill” impairment due to their share price drop that decreased the companies market cap/valuation substantially on paper. This one time non-cash goodwill and intangible asset impairment charge is a non-cash accounting adjustment with zero impact on cash flow, operations, or debt covenants.

In short, the business was profitable on an adjusted/operational basis with record revenue and positive adjusted earnings, but the GAAP net loss and big negative EPS were driven almost 100% by that one-time non-cash goodwill write-down. This is a common situation in public companies when stock prices decline sharply and does not reflect underlying business performance.

Personally, I have never seen a fiscally responsible company that is growing, decreasing debt, and doing the right thing, not eventually reflect their execution in the share price.

5.) Near-Term Catalysts

Meridian Holdings has some major catalysts including being recently granted a coveted Federal Brazil Gaming license, the upcoming expanded FIFA World Cup, and the completion of rolling out their “Atlas” AI platform in all regions. They do not have the marketing money of the bigger companies for customer acquisition, but they now have the advantage of 5 accretive subsidiaries allowing them to begin cross-marketing and scaling into their newly licensed regions.

I anticipate steady “organic” growth and estimate they start showing considerable net profit beginning 2026 Q3/Q4 earnings after the 2026 FIFA World Cup exposure boosts their brand recognition. With any new Brazil market capture or subsidiary growth, we are looking at a realistic annual revenue of $220 - $250 mil with $10 - $20 mil net or an EPS of .80 - $1.60 within the next few years.

6.) Global TAM

It is worth noting many stock promotors in this sector quote an inflated global industry TAM of $200 billion or more to show the highest possible runway. A more realistic, company-specific serviceable addressable market (SAM) for Meridian Holdings is estimated at around $15 billion. Although this number is much lower, even capturing a small percent of Meridian Holding’s realistic regional TAM would be transformative.

With that said, it is worth noting that the 2026 World Cup wagering is projected to exceed $70 billion, roughly 3X the approximately $23 billion total US 2026 Super Bowl wagering.

With a 60% increase in matches this event is set to eclipse the Super Bowl betting handles by 200 - 300%, offering smaller firms a unique stage to capture a massive global audience & establish their brands in an industry-defining moment on a worldwide stage.

7.) World Cup Brand Opportunity

The FIFA World Cup presents a monumental revenue & branding opportunity for the online gaming companies that own and control their own high-performance AI tech.

Meridianbet is one of those companies with their 5th generation “Atlas” AI tech rolled out, as well as being one of less than one hundred operators able to obtain a full Federal Brazilian Gaming Lic allowing sports-betting, i-gaming as well as retail locations.

8.) A Long History of Execution and Profitability

Meridianbet was built over 25 yrs privately with zero borrowed money and profitable the majority of their history. Unheard of in the sector. As discussed earlier, they could have sold their company and exited with $330 million but they wanted Nasdaq traded GMGI shares at a value of approximately MRDN $36. After the close of the merger in April 2024 insiders continued to buy and convert shares, now owning nearly 90% of outstanding shares. IMO, there is no way they would keep acquiring shares if they were not confident they can and will continue to execute and grow.

Over a decade ago Meridianbet, wanting to control their own tech and not spend on outsourcing, took the more expensive and difficult route to hire programmers and create their own AI system, knowing it would allow them to capitalize on “micro” and “live” B2C betting, create their own B2B content. They saw the tech advantages of having the ability to personalize each player’s account and collect valuable data that would ultimately increase margins as well as help them to comply with vast regulatory and tax requirements.

9.) Global Footprint, Moats, and Long-Term Sector Catalysts

Meridian Holdings operates in over 20 countries with different currencies, languages, and regulations, processing between a handle of between $2 - $3 billion in annual bets. They have the advantage of a proprietary tech stack as well as a closed loop ecosystem that captures value at every stage. They own their sports-book. They own their odds setting engine. They own their risk management algorithms. They own their casino platform. They own their content. These advantages are rare and will allow them to scale without 3rd party costs, thus driving higher margins in the long run.

Meridian Holdings is an emerging player with multiple B2B/B2C rev stream diversity, a large regulatory and geographic moat in a rapidly growing sector, in an international market with outstanding CAGR of 12%-15%. MRDN has positioned themselves early, as governments globally are fast tracking legislation to obtain the tax revenue while internet access, 5G, and cell service buildout allow for a long runway of access to capture a massive TAM.

Meridian Holdings not only has a regulatory and geographic moat but it is positioned to scale faster due to its proprietary tech advantages. When investors hear a name like DraftKings they immediately think of the sheer size and massive revenue generated, however Meridianbet, as small as it is, actually has comparable AI tech and a sports betting engine that exceeds DraftKings and most others in sheer volume and global breadth of betting markets.

10.) Meridianbet’s AI Tech Advantage

Meridianbet offers over 11 million betting markets per month, pre-match + live/in-play across 20,000 events, covering 800+ leagues worldwide with a deep focus on lower-tier soccer, regional competitions, and niche sports. In contrast, DraftKings offers several thousand markets daily and concentrates primarily on major U.S. leagues and high-profile events.

Meridianbet benefits from a lower-cost player acquisition strategy through its hybrid omni-channel online platform plus nearly 740 retail “Betshops” creating organic traffic and physical presence in 15+ jurisdictions.

Meridianbet, unlike DraftKings, creates their own tech & B2B content, as well as owns multiple synergistic subsidiaries while operating 5 synergistic businesses that deliver revenue diversification and scalable cross-synergies.

In the US, DraftKings and FanDuel, at 80% of the market, are clearly “The Big Dogs”, but Meridianbet’s exceptional diversity, AI-powered personalization Bet Recommender + assistant, and more efficient model, gives Meridianbet a clear competitive advantage for sustained growth in international sports betting and iGaming markets outside the saturated U.S. market.

Globally Meridianbet’s disclosed volume puts it in the top tier for sheer number of events and markets. Bet365 is the only major operator consistently described as having equal or greater breadth across lower-tier and niche sports.

In Brazil, top players Betano, Bet365, and Sportingbet dominate market share and offer deep coverage of Brazilian leagues + major international soccer, but none publicly claim higher raw event counts than Meridianbet’s 20,000/month. Meridianbet’s strength in lower-tier, regional, and niche events gives it an edge for bettors seeking variety beyond the biggest matches.

This difference matters because Meridianbet’s model emphasizes extreme breadth + AI personalization across many smaller events, while larger Brazilian-focused operators prioritize depth/odds quality on high-traffic leagues where most betting volume occurs.

The bottom line is Meridianbet is already an early leader in publicly reported event volume and global diversity. In Brazil and other emerging regions they compete head-to-head with or exceed most peers on raw numbers of betting opportunities, especially outside the major European/U.S. leagues. Bet365 remains the primary global peer in overall market depth.

11.) Player Acquisition Cost Advantage

Meridian Holdings enjoys a significant player acquisition cost advantage that drives superior unit economics compared with industry giants. The CEOs have repeatedly highlighted that the company acquires customers at a fraction of the industry norm, approximately $2 per customer in its sweepstakes operations, $7.60 per player on the RKings and CFAC tournament platforms, with the core B2C sports-book and casino business also far below peer averages although no exact sports-betting/casino CAC number has been made public.

In contrast, larger U.S. operators like DraftKings routinely spend $300 - $1,000+ per player while generating only around $300 in lifetime value, resulting in negative economics for many new users. The much lower CAC for MRDN stems from its hybrid retail/online model in less-competitive emerging markets, proprietary AI-driven personalization, decades of proprietary player data, and efficient sweepstakes-style entry points, delivering strongly positive lifetime value and sustainable profitability where many larger peers continue to burn cash on customer growth. Meridian Holding’s CEO Milosevic has flatly stated “we will not operate in an area at a loss”.

A Starkly Different Player Acquisition Strategy

Meridian Holdings, under CEO Zoran Milosevic, takes a fundamentally different approach to player acquisition than U.S. giants like DraftKings and FanDuel. While the larger operators pour hundreds of millions, and often over $1 billion annually into high-cost celebrity endorsements, influencer campaigns, and blanket digital advertising to drive volume in saturated markets, MeridianBet builds brand recognition and customer trust organically by embedding itself in the communities it serves.

Through its deeply ingrained ESG/CSR philosophy, explicitly described by Zoran as “not a slogan, but how we operate at scale” the company has executed nearly 300 CSR initiatives across 25 markets in 2024 alone, focusing on sports, education, youth programs, healthcare, environmental projects, and responsible gaming. These efforts include customer-involved “Meridian Donate” campaigns, employee ambassadorship, partnerships with regional governments to promote safe and ethical regulations that actively help to reduce illegal and predatory black-market operators.

Complementing this grassroots strategy are its 740+ company and franchised retail “bet shops” across Europe, Africa, and Latin America, which provide tangible local presence and foster long-term loyalty at far lower acquisition costs than the big players’ promotional-heavy models. This culture-first philosophy, supporting both internal employees and external communities, not only differentiates MeridianBet but creates sustainable, trust-based growth that many larger operators simply cannot replicate.

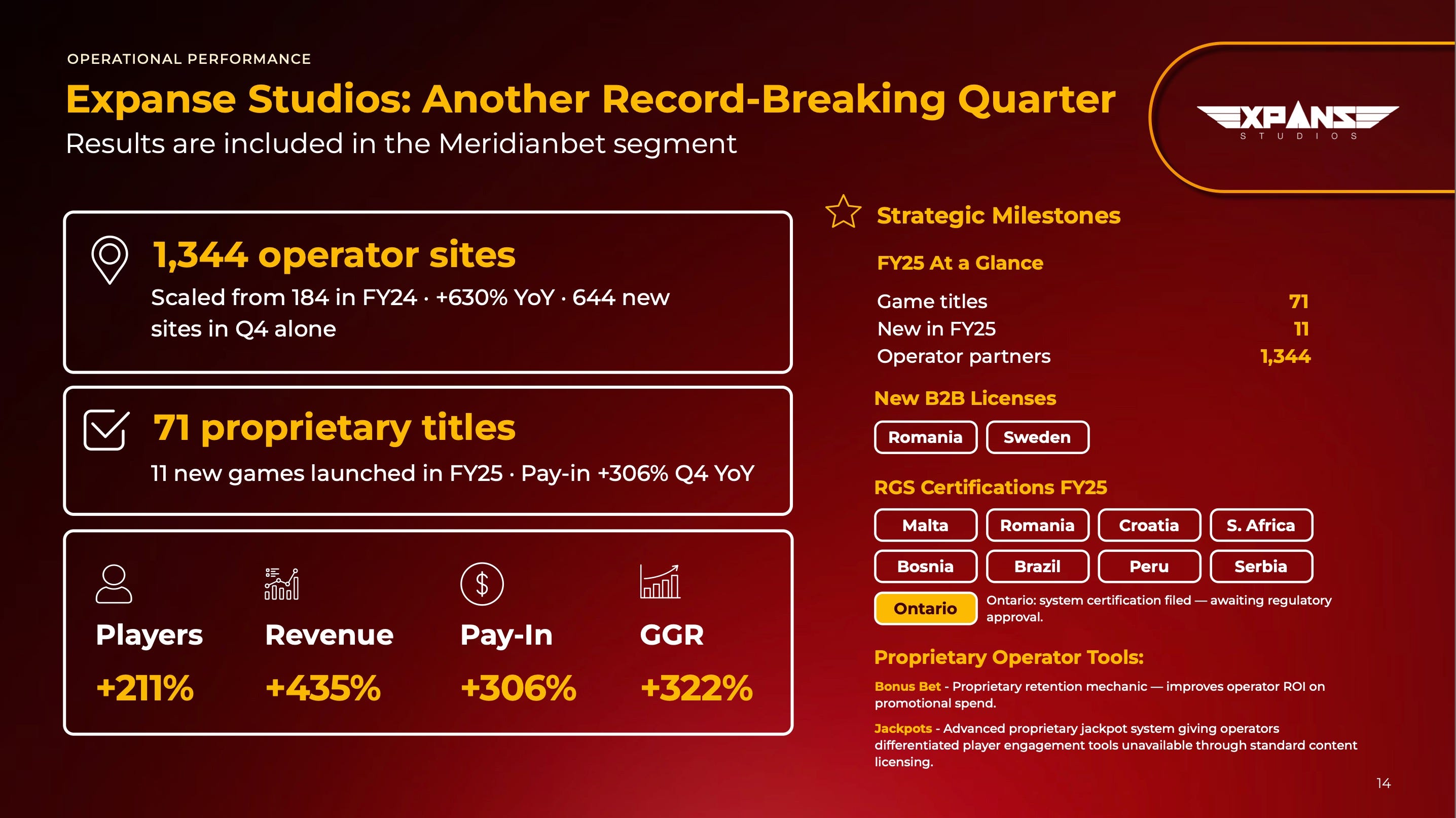

12.) The Content Edge: Expanse Studios

Expanse Studios, Meridian Holdings content making company, lead by CEO Damian Stamenkovic is literally inking a new B2B partner every few days, topping 1,300 operators last year and shooting for 3000 this year. Now in over 20 countries with recent entrance into Romania, Peru, Africa, Sweden, Croatia, US, Brazil with Canada in the process. With 440% yoy growth they are doing it all: AI, Prediction Bets, Crash Games, Social Games, Casino Games, Sweepstakes Games, Mobil first, etc. In-house content creation as well as outsourcing possibilities will create new revenue streams and only expand margins.

13.) Subsidiaries: RKings, MexPlay, and CFAC

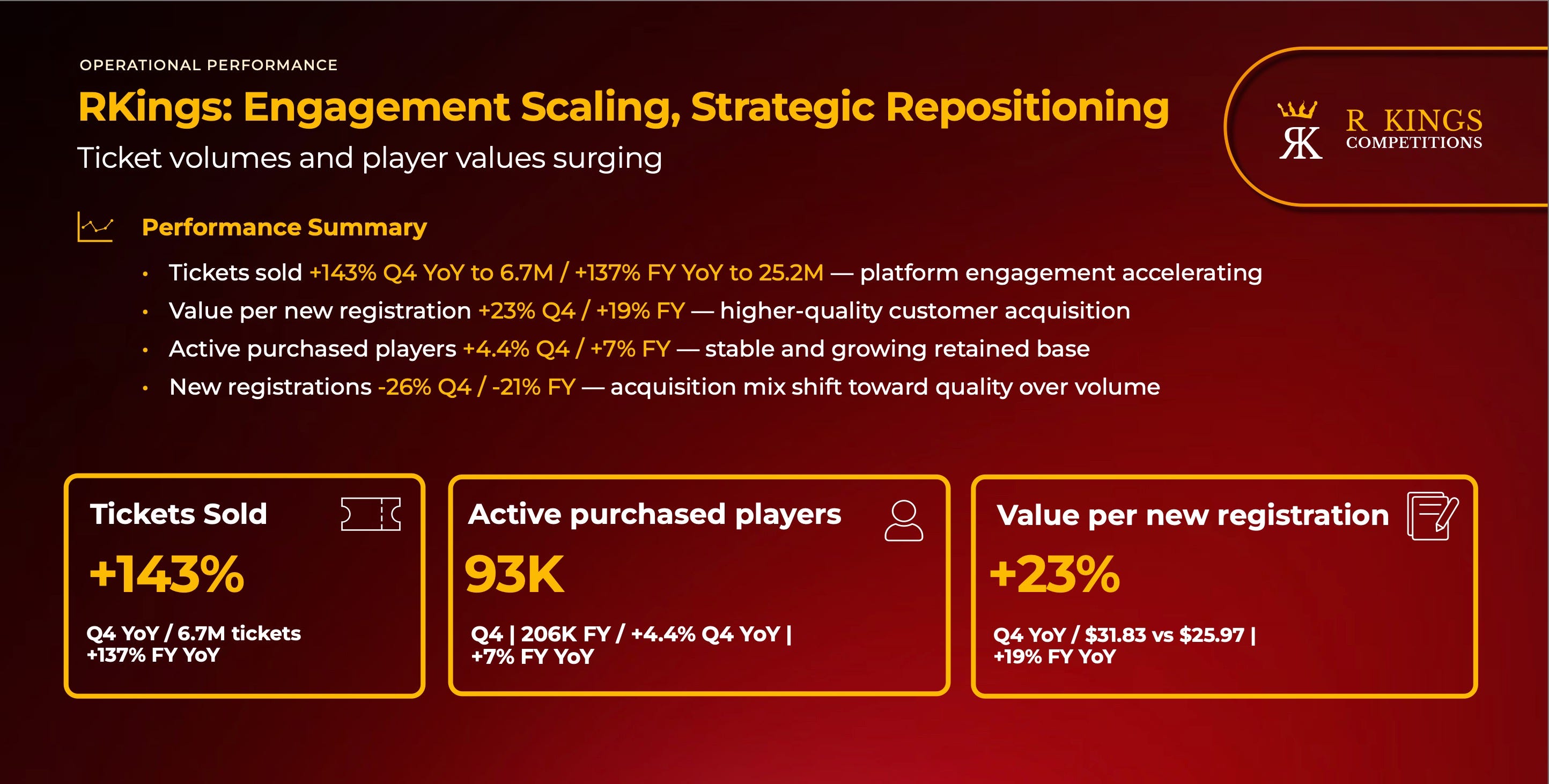

Meridian Holding’s subsidiary RKings Competitions in UK and now Ireland’s #1 competition, is led by founder Mark Weir and has doubled revenue since acquisition and is continuing to grow. Recent revenue came in at $35.1M and 25.2M ticket volume, up +137%.

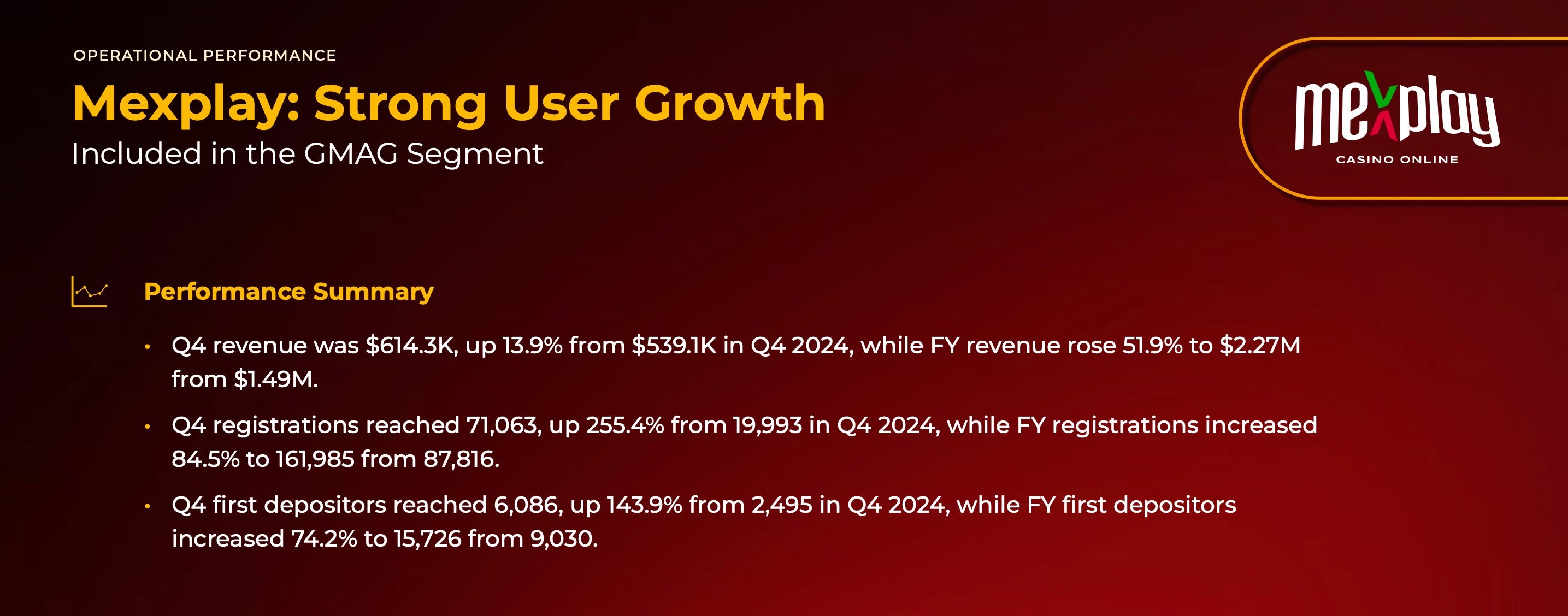

Meridian Holding’s subsidiary MexPlay is its regulated online casino/sports-book in Mexico, exciting with huge growth room as it delivered 52% revenue growth in 2025 amid 85% more registrations in a fast-expanding market also with 15%+ CAGR, low competition, and expecting a 2026 FIFA World Cup boost.

Meridian Holdings CFAC or “Classics For A Cause”, their more recent and smaller accretive acquisition is continuing to scale and increase revenue contributing $8.7 mil full year growing to $2.3 mil in Q4 alone.

These acquisitions are “decentralized” acquisitions rather than “roll-up” acquisitions, meaning the CEO or Founder and team responsible for their success was left in place to do what they do best — continue to execute and grow.

14.) Proven Leadership with Integrity

Leadership is one of the most important factors determining MRDN Holdings success. Meridianbet, by far the largest of the 5 MRDN companies CEO is Zoran Milosevic. Zoran is a steady, deliberate leader defined by an “infrastructure-first” approach. Zoran is the definition of a fiscally responsible, no-hype “execution-based” CEO, emphasizing Meridianbet is not a promised based company but an execution-based company. Exactly what I look for in a CEO.

Zoran champions capital discipline and long-term value creation. Unlike many competitors that rely on high-burn capital raises, he focuses on organic profitability and finding niche markets where the company can maintain margins. He has mentioned several times how Meridianbet simply will not operate in an area at a loss, and emphasizes mitigating risk by owning and controlling their own technology stack.

Meridianbet is not a company that is going to compromise anything to fluff the next earnings numbers. They repeatedly state they are NOT looking at the next quarters earnings, they are looking at the next 100 years. They have no intention of selling their shares and that is a big concern considering the amount they own.

Zoran has a rare strong moral and ethical code explicitly aligned with his business ethics. With Zoran at the helm, there is no “grey” area. He believes Meridian Holdings can increase value for shareholders at the same time as they increase value for society at large by placing an emphasis on responsibility, community impact, and long-term thinking.

As we discussed in marketing earlier, aligning with Zoran’s philosophy, MRDN is second to none when it comes to making a community impact in the regions they operate. Meridianbet conducts nearly 300 CSR, ESG, community impact initiatives, and public service programs per year across 25 markets, delivering massive impact as well as via its Meridian Donate Platform that lets players directly fund healthcare, education, sports, and social projects, thereby building brand loyalty and trust in every community it serves. Unlike others, they don’t spend a large amount of money blanketing media with expensive celebrity ads. They support making authentic positive and needed changes in their regional communities.

15.) Risks

In my opinion, Meridian Holdings is a multi-decade story. A misunderstood, undiscovered asymmetric opportunity. Is there risk? Absolutely, but I try to minimize risk by investing in companies w/a long history of fiscally responsible execution, profitable or turning profitable, multiple revenue stream diversity, a large amount of insider skin-in-the-game, and a share valuation that has not yet run-up. With that said, let’s discuss and address some of the risks associated with Meridian Holdings.

AI Risk

Full disclosure, I am not an expert when it comes to AI disruption or technology threats, but from my research I can find no scenario where AI disruption poses any significant near term material risk to Meridianbet Holdings.

Meridian Holdings recently finished rolling out their most advanced 5th generation platform “Atlas”. They own and control their entire end-to-end tech stack. Real-time operations serving hundreds of thousands of simultaneous bettors demands highly specialized, deeply integrated AI systems far beyond generic tools. These systems must instantly calculate live odds, manage risk, personalize offers, and comply with diverse regulations.

AI programs are tightly coupled with enterprise-grade cybersecurity to protect against fraud, cyber attacks, and money laundering, something off-the-shelf solutions are not near replicating. Most critically, superior performance requires seamless integration of decades of proprietary regional and individual player data that only MeridianBet has accumulated through years of live operations. New entrants or competitors lack this data moat and cannot simply “train” equivalent models overnight. As a result, MeridianBet’s scale, vertical integration, and in-house AI capabilities actually turn the technology into a competitive advantage for personalization, retention, and efficiency, protecting margins and demand across every layer rather than exposing them to commoditization.

Regulatory Compliance Risk

Meridian Holdings CEO Milosevic’s “no grey area of operation” philosophy has gained Meridianbet an impeccable regulatory history with zero “red flags”. The last thing I want to see is media headlines with my investment involved in legal trouble. Meridian Holdings decreases legal and regulatory risks by being actively involved in their regions of operations governments regulatory efforts to decrease predatory black market operators and add credibility to the industry.

Complete Loss of Capital Risk

Personally, I can handle the inherent volatility of micro/smalls as well as waiting the long, sometimes 5+ year timeline for a smaller company to raise cap, execute, scale, pay down debt, disruptive tech to one adopted, and revenue to hit the bottom line, HOWEVER I do not want to lose my entire investment.

As far as a risk profile for complete capital loss (not uncommon in the micro/small cap arena) Meridian Holdings would need to stop growing after 25+ yrs of expansion into 20 countries right after they achieved Nasdaq listing and rolled out their 5th gen AI tech platform “Atlas” that will increase margins. Also, right before the two largest catalysts in their history: World Cup 2026 and being granted a coveted Federal Brazil igaming/sportsbetting license. Highly unlikely.

Expanse Studios, that is growing on steroids, pumping out new games, and on the way to doubling their partnerships would need to suddenly stop acquiring new partners. RKings, now Ireland’s #1 and is growing double digits, would need to come to an unexpected halt and MexPlay, Golden Matrix’s GM-AG, Fairbet and Australia’s CFAC would need to stop growing in their incipient stage.

Original Golden Matrix CEO Departure

It should be noted the original parent company Golden Matrix (Nasdaq GMGI), after an extended 60 - 70% share price drop, recently did a 12/1 split and rebranded from Golden Matrix Group to Meridian Holdings (MRDN) to remain Nasdaq compliant and better reflect their parent brand Meridianbet.

The original Golden Matrix CEO Brian Goodman stepped down but all remaining operational CEOs have been left in place to do what they do best. In the last 5 years Goodman was able to accomplish a number of milestones including a Nasdaq listing and the acquisition of a number of accretive and synergistic companies that brought revenue from approximately $2 million to $185 million however, just as a coach loses too many games, if the share price does not reflect the execution, the coach bears the responsibility and Goodman stepped down.

Recently Goodman has come under fire for selling a fraction of his shares. To put this is context, Goodman has sold around 84k of his nearly 16 million pre-split adjusted shares ( about 50% held in Luxor Capital ) while Meridianbet insiders; Founder Aleksandar Milovanovic, CEO Zoran Milosevic, COO Snezana Bozovic, and CFO Richard Christensen have all purchased open market or converted close to 9,850,000 pre-split adjusted shares. That is massive confidence by Meridian Holdings.

Insiders typically only buy shares for one reason but often sell for many reasons. Goodman has expressed he has full confidence in Meridian Holdings future and would not be surprised if his small sales have something to do with his departure, tax purposes, raising capital for his new venture, or most likely, trying to decrease his ownership stake to under 10% for regulatory purposes. At this point I simply do not know but there will always be speculation. If the amounts were much larger I would be more concerned.

Addressing The Share Price Drop

As far as Meridian Holdings share price drop, large micro/small-cap share price drops are not unique to MRDN in our current speculative and sentiment based trading environment that largely ignores fundamentals in favor of AI and hot sector stocks with social media buzz. I believe the prolonged drop was largely due to a combination of targeted shorting and traders walking SP down into bid. This behavior is inherent with low volume micro/smalls and effectively increases negative sentiment which in turn fuels downward momentum and sentiment based trading algos with gasoline.

This negative momentum cycle and a huge short order, coupled with a lack of US visibility, zero awareness, and no significant shares available for any meaningful institutional positions (leaving mainly emotional retail sellers) are all large negative factors.

Lastly, the dilution required for Golden Matrix to acquire Meridianbet, although non-operational dilution and a common practice with growth-by-acquisition companies, is an easy narrative for traders to spin as a net-negative event to fuel more bad sentiment and downward share price momentum.

16.) Disclosure

I am a long term investor and own shares of MRDN. I am not an advisor. I am not in marketing. I have no affiliation with Meridian Holdings. I do not trade. I do this for fun and consider myself somewhat of a small-cap sleuth as I have now invested for over 35 yrs. I have made large amounts of money and lost large amounts of money. High rewards come with high risk.

I do my best to decrease risk but micro/small-caps are inherently risky. They are often illiquid and their low volume makes them subject to manipulation and difficult to exit. Their long hold timelines require inordinate patience and a tolerance for extreme volatility- but they can at times create life changing wealth.

These are simply my personal opinions and not a recommendation to buy the stock. I do my best to be as accurate as possible but there are quite possibly errors in my article. I am not a professional and advise investors to seek professional guidance.

Feel free to reach out on X (@uboat159) or comment below.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

That setup can work.

But when insiders own that much, the float gets thin.

And thin floats can move on attention, not just fundamentals.