Shift4 (FOUR): Pain and Opportunity

It’s been a rough year to be a Shift4 shareholder. There’s really no sugarcoating it.

The stock is down over ~60% from its highs and now trades at a nearly 13% FCF yield, which for a payments business growing 25%+ is about as cheap as it gets.

Every quarter feels like it should be the one that turns sentiment, and every quarter the market finds a new reason to sell. CEO transition. Global Blue noise. Guidance confusion. Pick your poison.

At some point you do start to wonder if the market knows something you don’t…

Sure, a lot of the skepticism is fair. There are real questions and concerns here. But when you look at the actual results and the valuation the market is putting on this business, and it’s really hard to take the sell-off seriously.

That said, if you’ve been following my coverage of FOUR, you know this is one of my largest positions. You probably also know this isn’t the first time I’ve had to sit here after earnings and explain why I’m not selling.

But as usual, I’ll walk through the results and give my thoughts.

So What Happened?

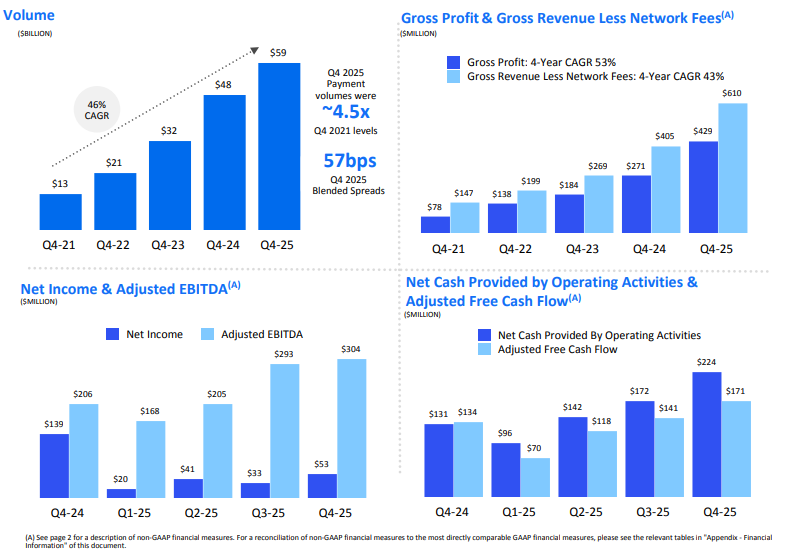

I’ll keep the results quick because they don’t deserve much debate. The core payments business continues to hum. Volume was $59 billion in Q4, up 23%, and Shift4 has now grown volume at a 46% four-year CAGR. The Americas business is growing mid-teens organically, the international payments business is growing in the high-20s, and the company now has over 80,000 merchants outside of the Americas.

For the full year, GRLNF came in at $1.98 billion, up 46%. Adjusted EBITDA was $970 million, up 43%. Free cash flow was $500 million. These are strong/healthy numbers.

So why did it sell off? I think there’s a few reasons…

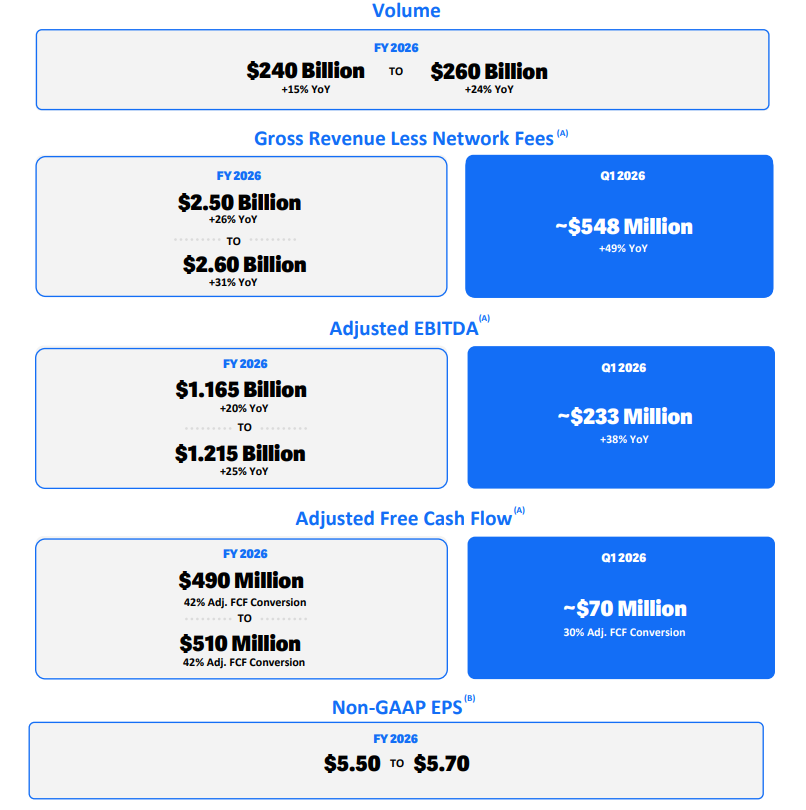

First, the 2026 guidance came in lighter than what the street was hoping for. Management guided to $2.5-2.6 billion in GRLNF (26-31% growth), $1.165-1.215 billion in adjusted EBITDA (20-25% growth), and $490-510 million in adjusted free cash flow at a 42% conversion rate. Non-GAAP EPS guidance of $5.50-5.70 was a full dollar below the consensus estimate of ~$6.45. On the surface, that’s a whiff.

The implied EBITDA margin at the midpoint is about ~47%, down from Q4’s ~50%. That looks like margin compression, and for a market that is already deeply skeptical of payments stocks, that was enough to hit the sell button. But that 47% isn’t the business deteriorating. It’s the business absorbing the largest acquisition in its history. More on that in a minute.

Second, the $1 billion free cash flow target that management had been dangling? That’s now on the back burner. They’ve shifted the framing to FCF per share instead of absolute FCF, and they’ve been plowing capital into buybacks rather than paying down debt.

The logic makes some sense. But the messaging was clumsy, the slide just disappeared, and the market read it as a retreat from a target they’d been promised. I have a lot more to say about this, so I’ll come back to it.

Third, and this is the one that I think people are overstating: Global Blue. The CEO (Taylor Lauber) was upfront about it.

“The acquisition of Global Blue represented a step-function increase in the pace of progress for Shift4. We have acquired a highly unique product capability that is deeply intertwined within the critical workflows of many of the world’s most well-known luxury brands. We have the benefit of an excellent team operating all over the world, and we view 2026 as an important year given it will be our first full year as a combined company. We are currently scaling our go-to-market cross-sell efforts throughout Europe, and remain excited about the opportunities to unlock meaningful revenue synergies in the months and years ahead. In the near term, Global Blue is gross margin accretive, but slightly dilutive to our adjusted EBITDA margins and also to working capital. However, as revenue synergies are realized, I anticipate Global Blue’s adjusted EBITDA margins will begin to trend towards that of Shift4, which in turn will benefit our adjusted FCF conversion levels.”

This is where I think the market is being way too impatient. The Global Blue deal closed in July. It’s been less than eight months. The company is integrating an international tax-free shopping business that operates in 75+ countries into a payments platform that was primarily U.S.-based until recently.

That takes time.

Personally, I never expected Global Blue to be meaningfully accretive this quickly. If you bought this stock expecting the biggest acquisition in the company’s history to boost margins within two quarters, I don’t know what to tell you. That 47% EBITDA margin in the 2026 guide? That’s the integration math working through the P&L. It’s temporary, and it’s exactly what you’d expect.

The organic growth in Global Blue’s TFS business is running mid-single-digits on a pro forma basis, which is below the high-single-digit growth they expected when they underwrote the deal. Some of that is macro. China and Japan tourism dynamics, FX headwinds on translation. And some of it might just be conservatism in the guide.

I’d flag this as something to monitor. If it doesn’t reaccelerate as cross-border travel normalizes, that changes the math on the deal.