Why I'm Buying Kaspi (KSPI)

I’ve started a new position in Kaspi. It’s still small, but one I plan to add to over time.

I’ve started a new position in Kaspi. It’s still small, but one I plan to add to over time.

The appeal is straightforward: here’s a company that dominates its home market, continues to grow both the top and bottom line at a healthy clip, and does it while staying highly profitable.

What makes it REALLY interesting is that, despite those strengths, the stock trades at just ~2.9x EBITDA with a FWD P/E of ~6.7x.

That disconnect is what caught my eye.

If Kaspi just keeps doing what it’s been doing, the compounding alone sets up attractive returns. If at some point the market decides to pay even a little more attention, the upside only improves.

Business Overview

Kaspi was founded in 2002 as a bank, built around a network of physical branches and traditional lending. For years it looked like a fairly standard financial institution. The turning point came in 2007 when Mikheil Lomtadze joined as CEO. Lomtadze, who came out of Baring Vostok private equity, steered the business away from being just another Kazakh lender and toward building a digital ecosystem.

The company spent the next decade rolling out products that gradually pulled more of daily life onto its platform. First came payments—utility bills, peer-to-peer transfers, and eventually QR acceptance for merchants.

Then came the marketplace, giving consumers a way to shop for everything from groceries to smartphones inside the same app they were already using to pay. Once those pieces were in place, Kaspi layered on fintech products: point-of-sale lending, BNPL, and working-capital credit for merchants.

That strategy worked out exceptionally well. Kaspi has transformed into a “Super-App” and is now the dominant digital platform in Kazakhstan.

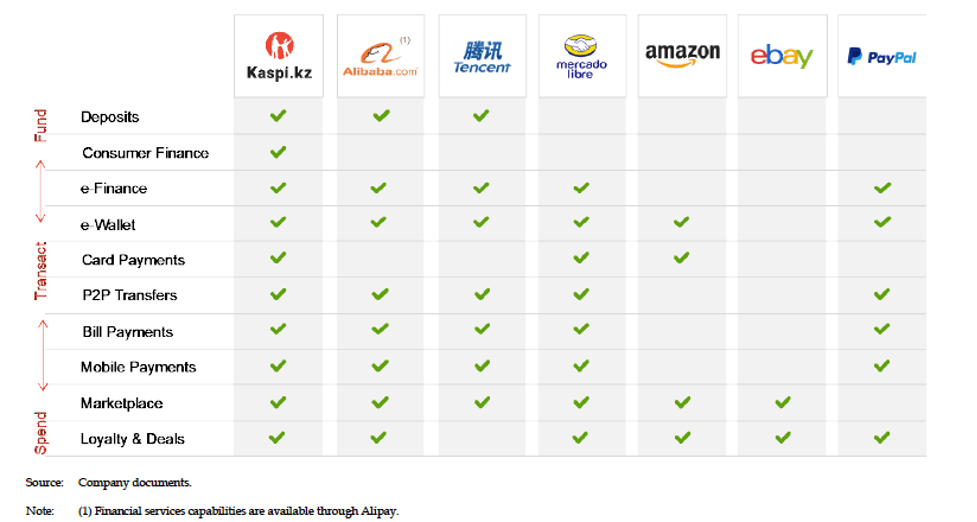

It operates through two apps—Kaspi.kz for consumers and Kaspi Pay for merchants—and everything flows through the three core businesses: Payments, Marketplace, and Fintech.

On the consumer side, Kaspi.kz is where you pay bills, send money, shop, order delivery, and finance purchases. On the merchant side, Kaspi Pay provides QR acceptance at checkout, in-app storefronts, advertising, delivery, and short-term loans. It’s an ecosystem that handles both sides of a transaction.

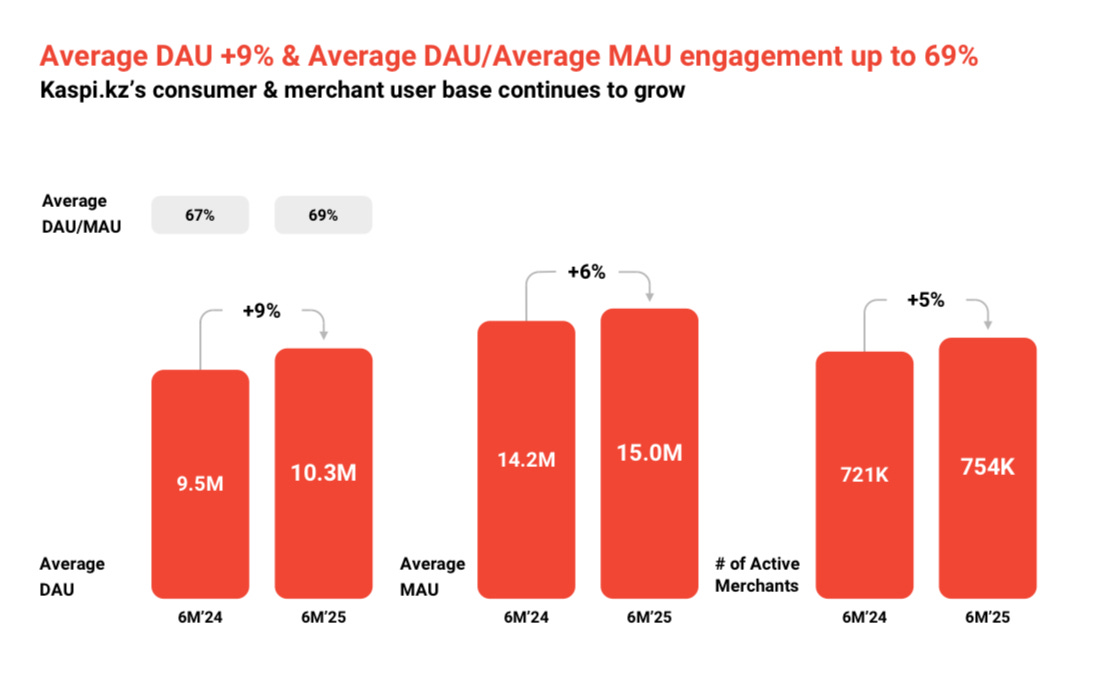

Penetration is extraordinary for a country of just 20 million people. Kaspi has about 15 million MAUs, with daily engagement around 65–70%.

Those customers average 75 transactions a month. Those aren’t casual users, that’s deep integration into daily routines. Once people build that kind of muscle memory, it’s almost impossible to pry them away.

The biz model is fairly simple but obviously, very powerful. Payments are the foundation, giving people a reason to open the app every day. Marketplace builds on that engagement, offering merchants storefronts, delivery, classifieds, and ads that turn activity into revenue. Fintech ties it together with BNPL, POS loans, and merchant credit, underwritten using the data Kaspi sees flowing through payments and commerce.

Each piece feeds the others, creating a loop that’s hard for competitors (or even traditional banks) to replicate… And unlike most fintech names, Kaspi has been consistently profitable for years.

Management has made a point of stressing discipline. When they acquired a 65%+ stake in Hepsiburada just a few months ago (Türkiye’s leading marketplace), co-founder & CEO Mikheil Lomtadze emphasized:

“Hepsiburada’s management team are focused on profitable growth rather than growth at all costs.”

That’s exactly how Kaspi built dominance at home, and it’s the same framework they’re applying abroad.

They’ve also taken smaller steps outside Kazakhstan. They looked at acquiring Uzbekistan’s Humo payment system, and in August 2025 partnered with Ant’s Alipay so Chinese tourists can pay at Kazakh merchants through Kaspi QR. Not huge in revenue terms today, but proof the platform can extend beyond its borders.

What Kaspi has built is simple at its core: high-frequency use cases that lock in consumers, multiple ways to monetize those interactions, and a management team that refuses to chase growth for its own sake. From its roots as a traditional lender to becoming the country’s digital operating system, Kaspi has executed with consistency. And now it’s testing that same playbook in larger markets like Türkiye.

Financials and Valuation

Kaspi’s numbers look like what you’d expect from a market leader with real scale: steady growth, strong margins, and consistent cash generation.

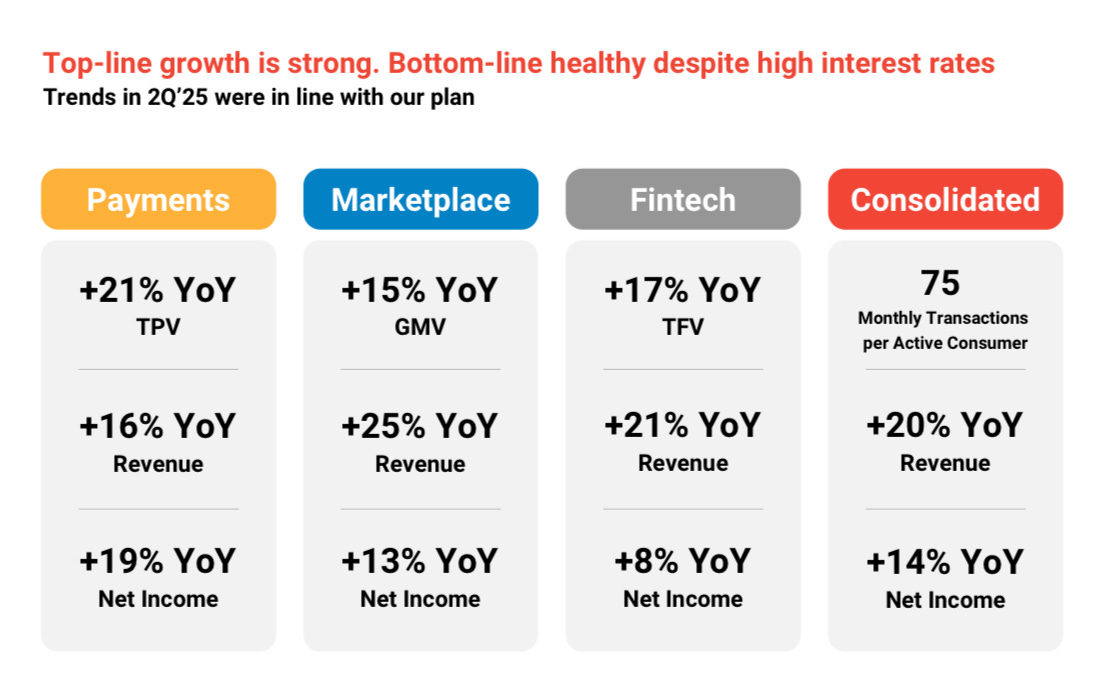

Q2 / 1H 2025 results:

Q2 revenue: ₸734 billion (+20% YoY)

Q2 net income: ₸276 billion (+14% YoY)

1H revenue (ex-Türkiye): +20%

1H net income (ex-Türkiye): +15%

Payments and Fintech: both growing in the high teens

Marketplace: revenue growth outpacing GMV thanks to services like ads and delivery

Advertising: +91% YoY in the first half, now a real driver

That’s the kind of report you’d expect from a market leader with entrenched distribution. It's clear Kaspi isn’t in the “grow first, figure out the economics later” camp, it’s been consistently profitable for years. Margins remain fat, return on capital is high, and the model keeps throwing off cash.

Despite that kind of performance, the stock trades at only ~6x NTM earnings. When you compare that to its “peers”, the valuation gap becomes obvious.

Kaspi is growing faster than all of them, more profitable than most, and arguably just as entrenched in its home market as MELI is in Latin America. The gap isn’t about fundamentals—it’s about geography. Investors don’t want Kazakhstan exposure, so they apply a permanent discount.

The question is whether that discount is already too extreme. At today’s multiple, the stock can work purely on compounding. If earnings keep growing mid-teens or better, you don’t need a re-rating to make money.

If sentiment ever shifts and the multiple expands even modestly, the upside gets much more interesting.

My Investment Thesis

Kaspi is priced like a risky bet when it’s really a dominant franchise. The business is entrenched, profitable, and still growing, yet the market treats it like a coin flip because they operate in Kazakhstan.

At ~6x earnings, the setup is asymmetric. If the multiple never changes but earnings keep compounding at a mid-teens clip, the stock works. If the multiple moves even modestly higher, the returns get a lot more interesting. And if the multiple somehow compresses further, the downside is limited. It’s already priced as if something’s broken.

I don’t need Kaspi to conquer new markets for this investment to work. All it has to do is keep executing the same playbook that got it here: grow transaction volumes, monetize marketplace services, and lend responsibly with the data edge it already has. Türkiye gives it a bigger runway, Alipay+ validates its rails, and optionality in places like Uzbekistan could come over time. None of that is required for the thesis, but it’s nice to have.

The backdrop is also pretty interesting. Markets are crowded into the Magnificent 7, paying 25–30x earnings for growth that doesn’t look meaningfully better than Kaspi’s. Liquidity is herded into the same handful of U.S. names, while a business trading at 6x earnings with high returns on capital and fat margins gets ignored.

That cycle won’t last forever. When sentiment shifts, investors will go looking for quality compounders at a discount, and Kaspi fits that profile perfectly.

For me it’s pretty simple: the business is excellent, the valuation is absurd, and the risk premium is mispriced. Worst case, the compounding alone pays me.

Best case, the market eventually gives Kaspi credit for being what it already is—a dominant, profitable platform with years of growth ahead.

That’s why I own it, and why I’ll keep building the position over time.

Could very well be another one of those investments that goes nowhere for next 2 years, and then when it hits $150 in year 3, all analysts will all of a sudden turn bullish.

Hello. You got in with common stock only or are you also looking at options? I would look at options form the risk perspective (not to lose more than the premium). Thank you