Why I'm Avoiding (Most) U.S. Equities

History Doesn't Repeat, But It Sure Rhymes

I haven't owned a meaningful position in U.S. stocks for two years. While everyone else chased the AI boom, I've been buying Chinese tech giants at single-digit multiples and forgotten compounders trading at reasonable prices.

This contrarian bet has already paid off—my portfolio delivered solid returns despite missing the U.S. rally entirely.

But I think the real payoff is just getting started.

When you're paying $36 for every dollar of free cash flow in the S&P 500, but can get the same dollar for $12 in emerging markets, the choice becomes obvious. At least, it should be.

Yet here we are in 2025, with U.S. stocks trading at their most expensive levels in decades while the rest of the world sits on clearance.

The Most Expensive Party in History

Let's start with the uncomfortable truth. U.S. equities are expensive. Not "a little pricey" expensive—historically, dangerously expensive.

The S&P 500 trades at 22.3x forward earnings as of late May 2025, well above its 20-year average of 16.7x. That puts the index roughly 50% above normal valuations.

The few times we've been this stretched (e.g., 1999 and briefly during the pandemic euphoria) haven't exactly been followed by stellar returns.

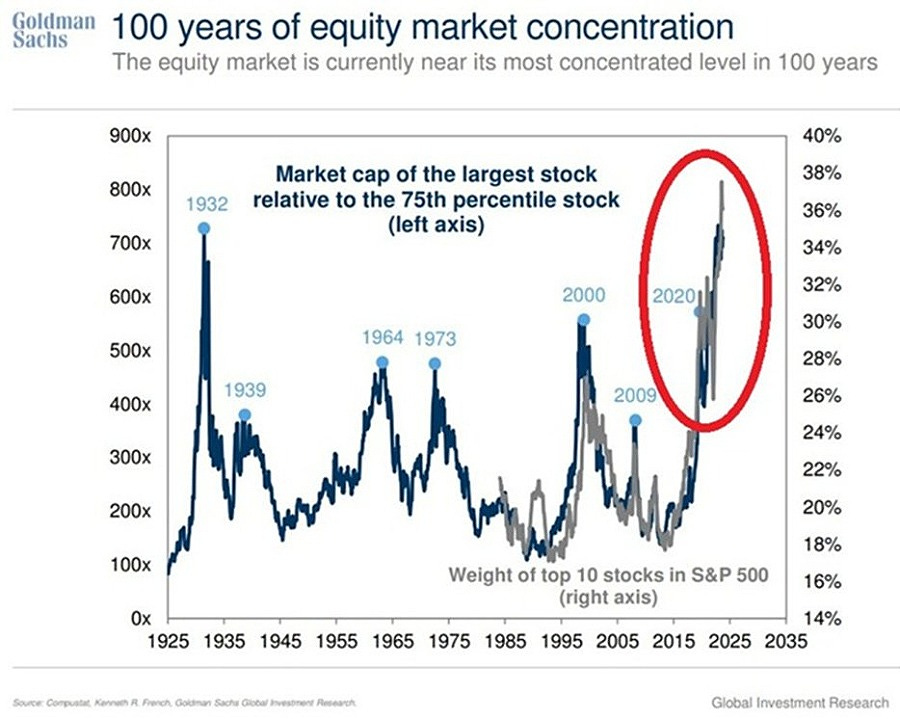

But it's not just the multiple that worries me. It's the concentration. The top 10 stocks now represent nearly 40% of the S&P 500's market cap. That's the highest concentration we've seen in over a century.

Seven companies control more than one-third of the index's performance. This level of concentration extends far beyond index investing—it permeates the entire U.S. equity market, where these same mega-cap names dominate every conversation and most portfolios.

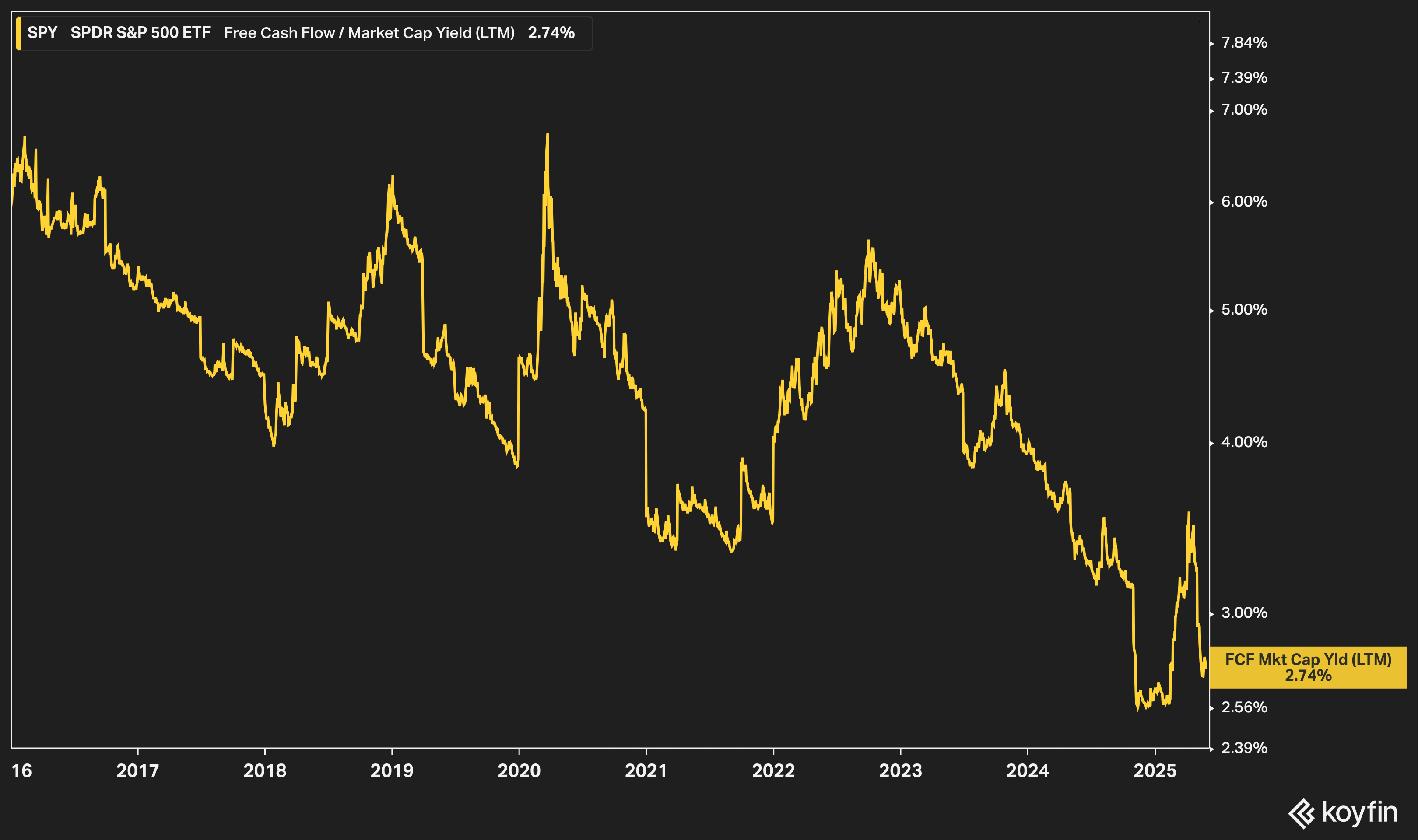

The free cash flow yield tells the same story.

The S&P 500's free cash flow yield has collapsed to just 2.74%—the lowest level in two decades.

Level up your investment research with Koyfin's powerful market analytics platform. Try Koyfin today using my referral link and get 20% OFF any paid plan!

Try Koyfin Now!

You're paying $36 for every dollar of free cash flow generated. Compare that to emerging markets, where you can get the same dollar of cash flow for roughly $12.

This isn't about being anti-American or pessimistic about innovation. It's about math. When the broad U.S. market trades at these levels, you're betting that either earnings will grow dramatically faster than historical norms, or you're comfortable with below-average returns for the next decade.

History suggests neither is particularly likely.

I just can't get excited about paying these prices when there are so many better opportunities elsewhere.

Where the Real Opportunity Lives

While investors obsess over the same seven mega-cap names, the rest of the world is on sale.

Emerging markets trade at just 12.7x forward P/E versus 22.3x for U.S. stocks. That's roughly half the valuation for companies projected to grow earnings significantly faster over the next three to five years.

The discount is even wider on a price-to-book basis, where emerging markets trade at a 40% discount to developed markets. But nowhere is the disconnect more obvious than in China.

Chinese equities are trading at their deepest discount to global markets in over a decade. MSCI China is now trading at just 0.6x the valuation of MSCI World on a forward P/E basis. That's about one standard deviation below the historical average.

Think about what that means. You're getting Chinese companies—many of which are global leaders in their industries—at half the multiple of the rest of the world.

The same companies that dominated e-commerce, gaming, and digital payments globally are now priced as if they're about to disappear.

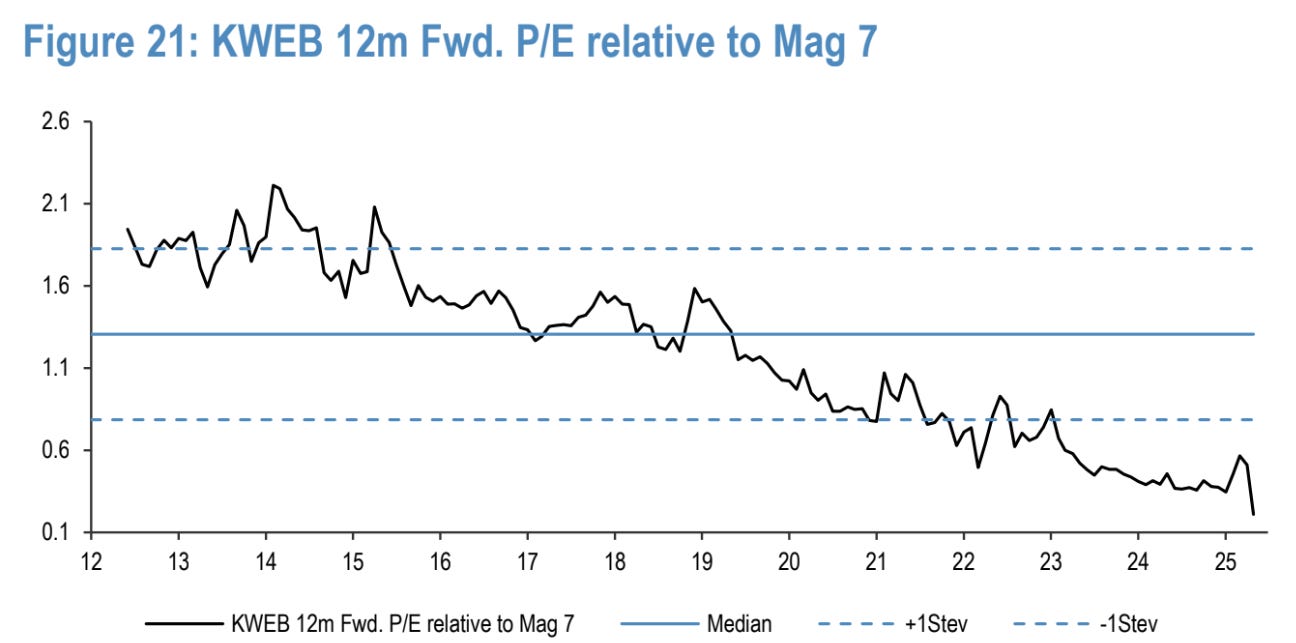

It gets even more extreme when you look at how cheap Chinese tech has become relative to U.S. tech. The KWEB ETF, which tracks Chinese internet companies, is trading at just 0.3x the forward P/E of the Magnificent Seven. That's the lowest relative valuation we've ever seen.

We're talking about companies generating massive free cash flows, sitting on fortress balance sheets, and operating in the world's second-largest economy. Yet they're priced as if they're penny stocks.

The regulatory overhang that kept these valuations depressed is finally lifting, with Beijing signaling a much more supportive stance toward the tech sector.

I've been adding to Chinese positions steadily over the past two years. While most investors chased AI hype at 40x sales, I was buying category-leading businesses that actually generate billions in free cash flow at single-digit multiples.

The irony is thick.

Everyone's paying premium prices for American tech stocks they've owned for years, while equally compelling businesses trade at a fraction of the price.

History Doesn't Repeat, But It Sure Rhymes

For the first time since the financial crisis, I genuinely believe we’re at an inflection point where international markets are set to outperform U.S. stocks.

The early signs are already visible.

In 2025, international equities have started to pull ahead, with European stocks posting their strongest monthly performance relative to the U.S. in January in more than a decade. Emerging market funds are finally seeing net inflows after years of outflows, the dollar has softened from its peak, and global strategists are boosting international allocations across the board.

History shows these leadership cycles are inevitable. Since the mid-1970s, U.S. stocks have typically outperformed international markets in 7–8 year stretches before the baton passes.

The current run, which began in 2010, has now lasted over 14 years—by far the longest stretch of American outperformance on record.

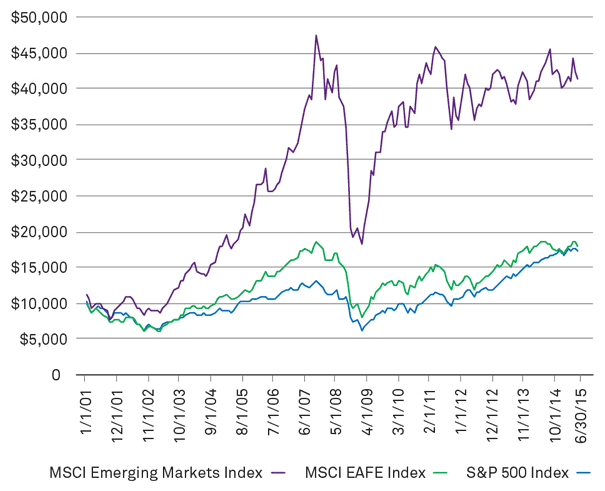

It wasn’t always this way. During the 2000–2009 “lost decade,” the S&P 500 posted a total return of about -1%, while emerging markets delivered annualized returns of over 10% per year—more than doubling investor capital.

Even when you zoom out to the past 25 years (2000–2025), which includes this recent stretch of U.S. dominance, the results are much closer than most realize. Both the MSCI Emerging Markets Index and the S&P 500 have delivered high single-digit annualized returns.

From 2000 through the early 2010s, emerging markets actually outperformed the U.S. by a wide margin—especially during the 2000s, when the S&P 500 flatlined and EM surged. It wasn’t until the second half of the last decade—primarily after 2016—that the S&P 500 really separated itself and pulled ahead in cumulative returns.

The setup today feels like the late 1990s in reverse. Back then, emerging markets were the expensive, high-flying growth stories while the U.S. market quietly offered value.

Now, it’s completely flipped. Most major forecasting firms expect emerging markets to outperform U.S. equities over the next decade, and the current valuation discount provides a substantial margin of safety.

The Bottom Line

This isn't a market timing call or a prediction of imminent doom. It's a simple recognition that valuations matter for long-term returns, and most American stocks are priced to disappoint.

I'd rather own dominant Chinese tech companies at 8x earnings than American tech companies at 30x. I'd rather buy emerging market leaders growing 15% annually at 12x multiples than pay 25x for 5% growth in the U.S. And I'd rather construct a portfolio of individual businesses trading below intrinsic value than chase momentum at historic premiums.

Look, there's no compelling reason to be overweight U.S. stocks right now. The valuations don't make sense. The concentration risk is extreme. And there are genuinely attractive alternatives trading at much more reasonable prices all over the world.

The beautiful irony?

In five years, when this positioning looks obvious in hindsight, everyone will claim they saw it coming. But over the past two years, while it actually mattered, most investors kept buying American stocks at 20-30x earnings and calling it prudent diversification.

My new dollars have been going where valuations still matter, and that's been almost everywhere except the United States.

Disclaimer: This is not investment advice. I'm sharing my personal research and positioning—always do your own due diligence and make decisions that align with your financial goals and risk tolerance.

Thanks Brian. A great article, and I agree 100% with you.

I live in Malaysia, but for me personally my markets are both China and Singapore.

For those who disagree and say China is uninvestable, my usual response is go and have a look.

Visit China, believe me it will rock your socks!

Agree - I have been collecting EM names for a few years now. And the potential is enormous.