The Most Asymmetric Bet in China AI

The Landlord of China’s AI Boom

If you’ve been reading me for any amount of time you know where I stand on China and AI.

I’ve written about it a lot, probably too much… but demand for AI compute over there is not slowing down. If anything it’s accelerating.

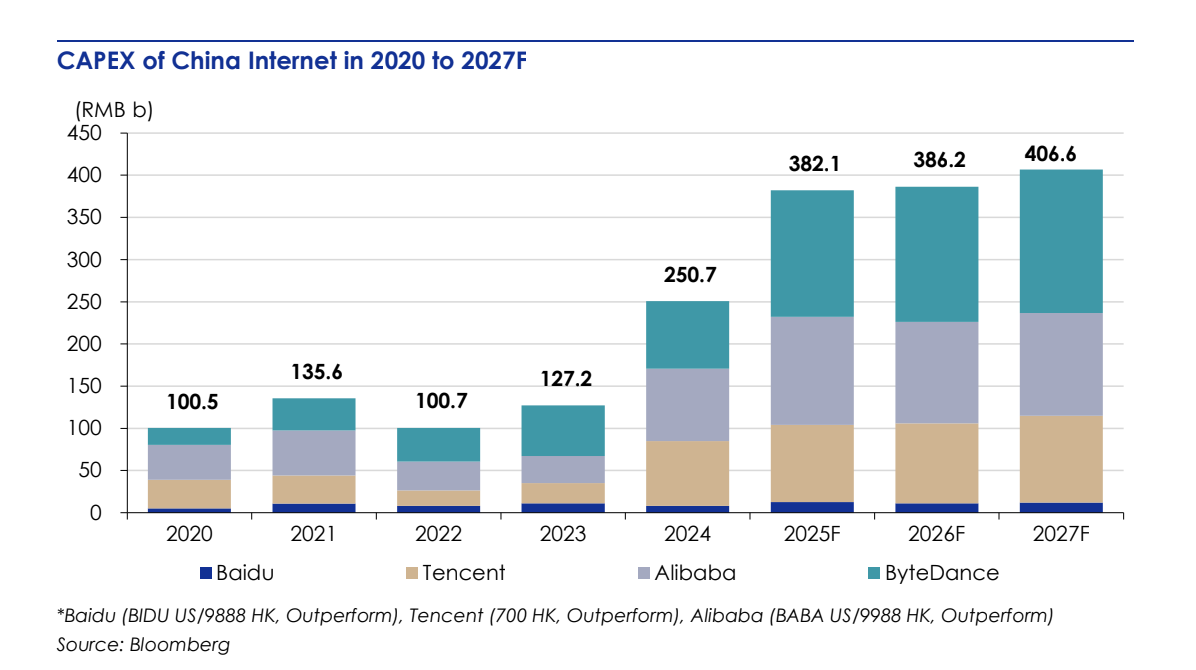

Alibaba is rationing GPU access. ByteDance keeps raising capex. Between the four of them, China's big tech giants are on track to spend over RMB 380 billion a year on AI infrastructure. The demand for physical compute capacity is massive and shows no signs of letting up.

Which brings me to VNET Group VNET 0.00%↑

VNET runs over 50 data centers across 30+ cities in China. They're carrier-neutral, cloud-neutral, and when ByteDance or Alibaba or Tencent needs somewhere to put all that compute, a lot of them are calling VNET.

And just a couple weeks ago, ByteDance signed a 500MW data center deal with VNET, the largest order in company history.

I first came across the name through jukan05 on X a couple months ago. If you’re interested in the data center and semiconductor space he’s definitely a must-follow.

Once I started looking into the company, I was immediately intrigued. I then reached out to P14 Capital, who I knew had been following the name closely, and he was kind enough to share his work with me. Turned out we'd arrived at pretty much the same conclusion independently, so rather than write my own version we decided to collaborate.

A lot of the detailed modeling and industry work below is his, with my commentary and framing layered in throughout.

If you’re not already following P14, you should be. He writes about SMID-cap opportunities on Substack and knows this name inside and out.

Coughlin Capital has a partnership with Koyfin (the research platform I personally use), through which you can get 20% OFF any plan. Use this link to claim yours.

You'll get institutional-quality charting, comps, screening, and financial data all in one platform.

Business Overview

Founded in 1996, VNET (formerly 21Vianet) launched the first carrier-neutral data center in China in 1999. Before that, most data centers were owned directly by state-run telecom companies. It went public on NASDAQ in 2011 and today runs three segments.

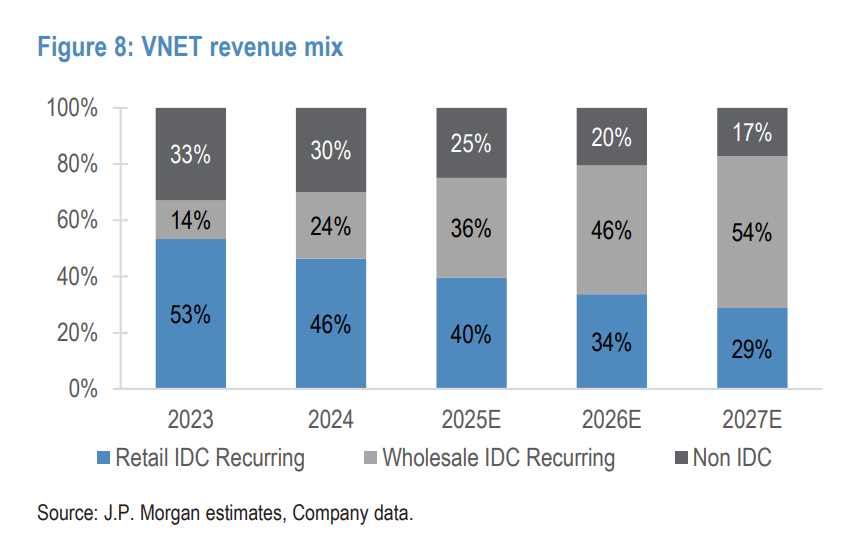

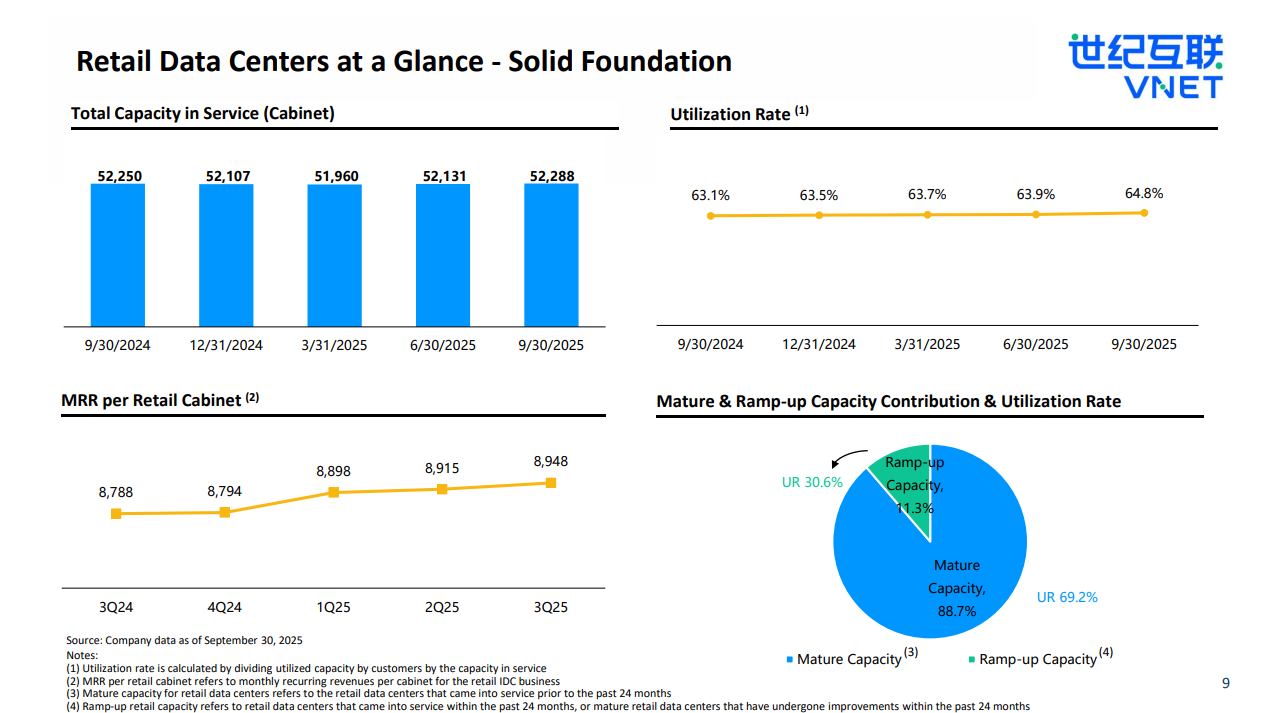

The retail IDC business makes up about 40% of trailing revenue. Think cabinet space rented to banks, Microsoft Azure, and SMBs. Stable, recurring, growing at low single digits. As of 3Q25, VNET operated about 52,288 retail cabinets with utilization ticking up 170 basis points year-over-year to 64.8%. Their Retail MRR has been gradually rising as legacy cabinets get repurposed for higher-performance workloads like fintech and autonomous driving.

The wholesale IDC business is the most intriguing. It’s about 36% of trailing revenue but growing at ~96% year-over-year. This is the large-scale, customized capacity measured in MW that hyperscalers like ByteDance, Alibaba, Tencent, and Baidu lease under multi-year contracts.

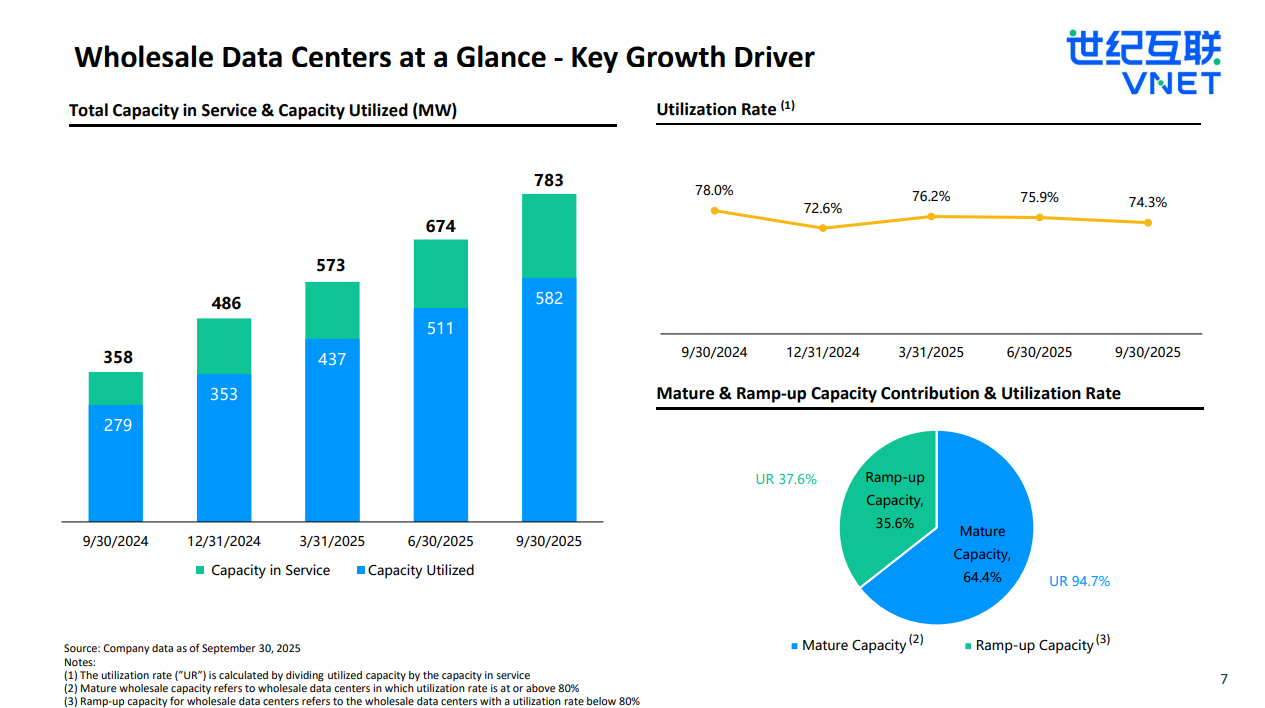

Wholesale capacity in service has gone up roughly 2.7x in three years to 783MW as of 3Q25, and those 400-450MW of deliveries in 2025 are 100% supported by orders on hand.

VNET’s customer move-in timelines have compressed from 24 months down to 6-12 months, which means wholesale customers are reaching maturity much faster. Management says mature IDCs are inching toward 95% utilization.

As P14 notes, wholesale IDC earns monthly recurring fees under long-term contracts, typically 3+ years.

“Hosting fees make up most of the monthly bill, while consumption fees reflect variable usage tied to power consumption and utility pass-throughs.”

Pricing is hard to isolate cleanly because rapid capacity additions cloud MRR per MW, but the bottom line from P14’s work is that:

“It is safe to assume that there is no pricing pressure in the industry.”

Given the demand environment right now, that tracks.

You’ll notice revenue spikes in the summer months for both retail and wholesale because increased cooling needs and higher seasonal electricity tariffs get passed through to the customer. And in the wholesale business specifically, VNET benefits from billing by consumption because domestic AI chips are less power-efficient than global alternatives, consuming roughly 70% more electricity for the same workload.

That translates directly into higher revenue per unit of compute. It's a weird dynamic where US chip restrictions end up being a tailwind for the data center operator.

There’s also a non-IDC segment at about 25% of revenue (cloud solutions, VPN services). Decent margins but not the growth engine.

The revenue model is roughly 90% recurring. Multi-year contracts and monthly billing. As the wholesale mix keeps growing, the overall margin profile keeps improving. Gross margins have expanded nearly 350 basis points since FY22, and EBITDA margins have followed.

Management is guiding for about 30% adjusted EBITDA margins in FY25, with the trajectory clearly pointed higher as wholesale takes a bigger share.

The Industry

China’s data center market is being pulled by two forces pointing the same direction: demand acceleration from domestic AI and supply relocation driven by national policy.

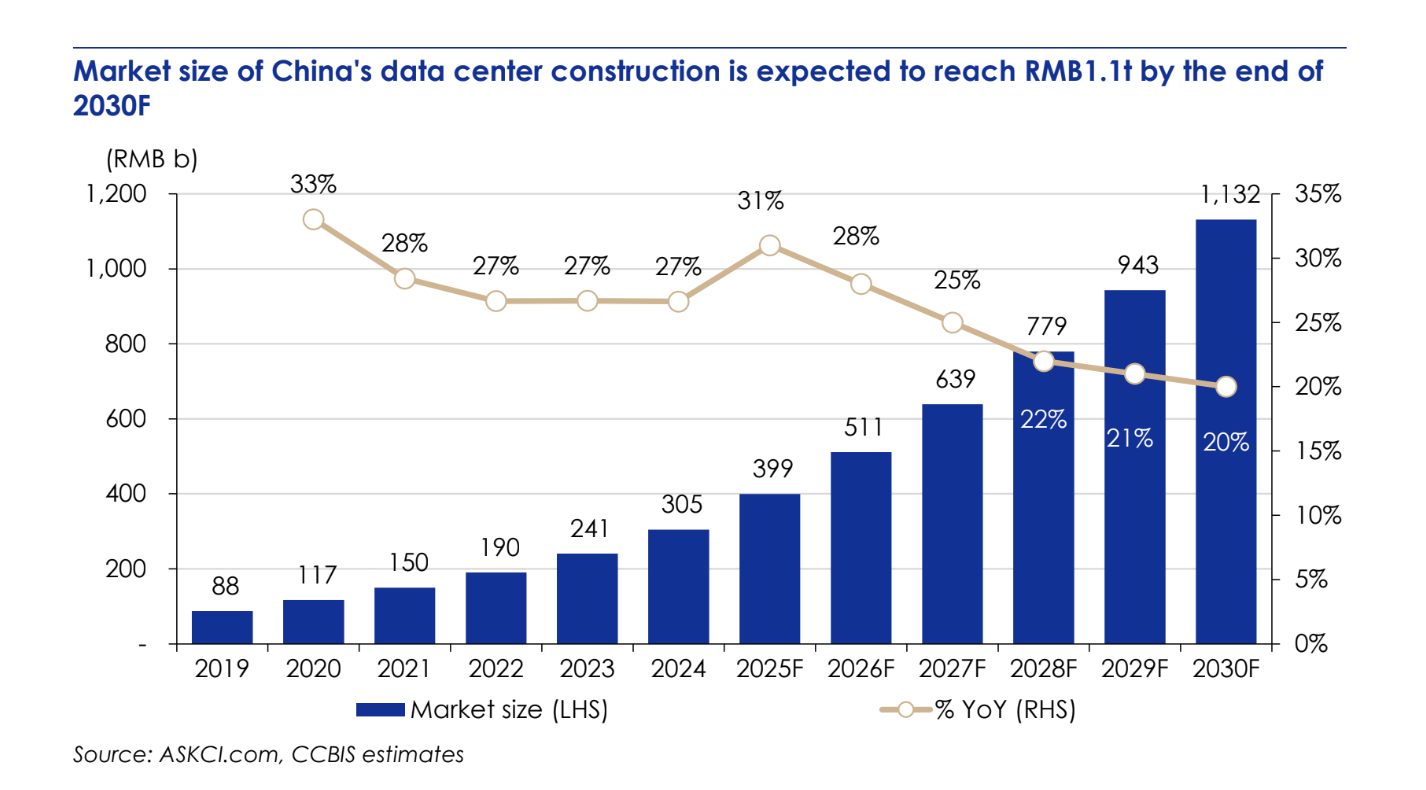

The sector hit a step-change in 2025. China's data center construction market reached roughly RMB 399 billion (~$55 billion) with 31% growth, the fastest year on record. AI-specific infrastructure accounted for over 80% of new IDC investment in the first half. And the growth doesn't stop there, the market is projected to nearly triple to over RMB 1.1 trillion by 2030.

China's recently released 15th Five-Year Plan places explicit emphasis on AI infrastructure, and the "AI Plus" initiative is expected to generate trillion-yuan-scale markets by integrating AI across manufacturing and services.

Beijing alone is targeting a core AI industry value of RMB 1 trillion (~$140B) by 2030 versus about RMB 450B in 2025. The government is backing it with R&D tax deductions (200% in some cases), a national AI fund ($8.2B annually), and energy subsidies.

On the supply side, the “East Data, West Computing” policy introduced in 2022 established eight national computing hubs to balance data demand with resource availability. Third-party operators like VNET have benefited because they’re more agile in navigating the regulatory approval process.

The central government’s “window guidance” through the NDRC has tightened new power quota approvals to about 10% of submitted projects to prevent overbuild. So the available supply in attractive regions, where power costs are significantly lower, is constrained. Pricing has stayed healthy as a result.

And the cost differential between regions is massive. Electricity in western regions like Inner Mongolia runs about RMB 0.32/kWh versus Tier-1 cities at RMB 0.60-0.80/kWh. The government also enforces differentiated power tariffs based on Power Usage Effectiveness (PUE), which raises the bar for new entrants and benefits operators with strong green energy credentials.

At Coughlin Cap, I cover the companies, themes, and macro trends I think matter most. Subscribe to get full portfolio visibility, in-depth research, and ongoing updates as my positions evolve.

It’s obviously not a secret that Hyperscalers want to build some in-house capacity, but they’re increasingly leasing from third parties because of faster time-to-power and balance sheet flexibility. The industry structure has shifted accordingly.

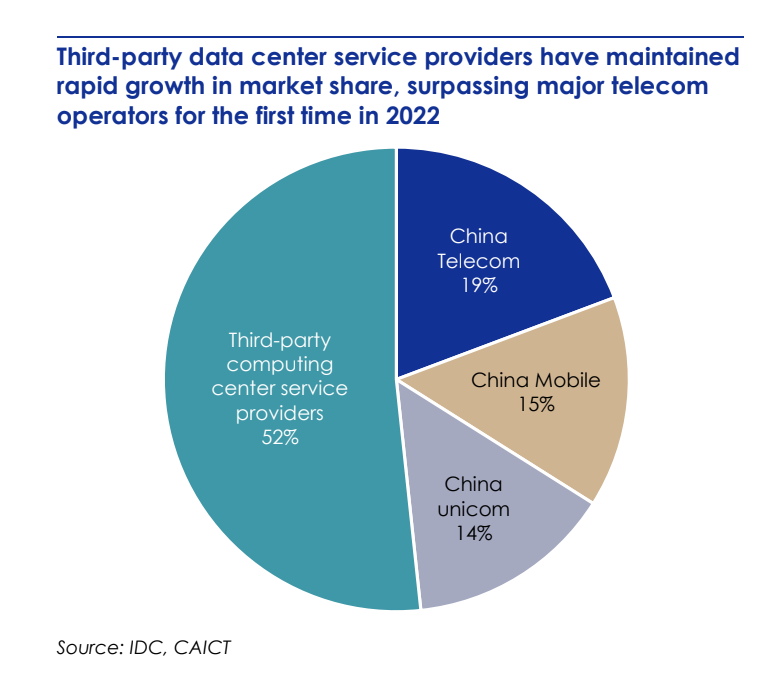

Third-party providers now control over half the market. That's a full inversion from a decade ago when state-owned telcos ran the show. China Telecom, China Mobile, and China Unicom still combine for about 48%, but they've been losing share steadily as hyperscalers have gravitated toward carrier-neutral operators who can move faster and build to spec. VNET sits in that 52% bucket, and the share shift is still going their direction.

VNET also has a unique edge that’s easily overlooked…

| A guest post by

|