[Update] Shift4 (FOUR): Still Way Too Cheap

operational strength, growing cash flow, and a management team that continues to act like owners.

Shift4 reported earnings yesterday, and after initially jumping about 10%, the stock finished the day red… The overall market was down big, which likely dragged it lower, but the quarter itself couldn’t have been better. I used the dip to buy more shares.

This quarter was everything I want to see from my largest position: operational strength, growing cash flow, and a management team that continues to act like owners.

This wasn’t just a good quarter. It was a statement.

Revenue, margins, and cash flow all moved higher, and management followed it up with a bold new $1 billion buyback authorization—a serious number for a company still trading around a $7 billion market cap. It tells you exactly how they view the stock: deeply undervalued.

If you missed my original write-up on Shift4, it’s worth a read before this one.

![[New Position] Shift4 Payments (FOUR)](https://substackcdn.com/image/fetch/$s_!PiaE!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F6bfbe39a-ee06-4b63-bb2f-30884fa4e88b_2048x1452.jpeg)

Another Quarter of Execution

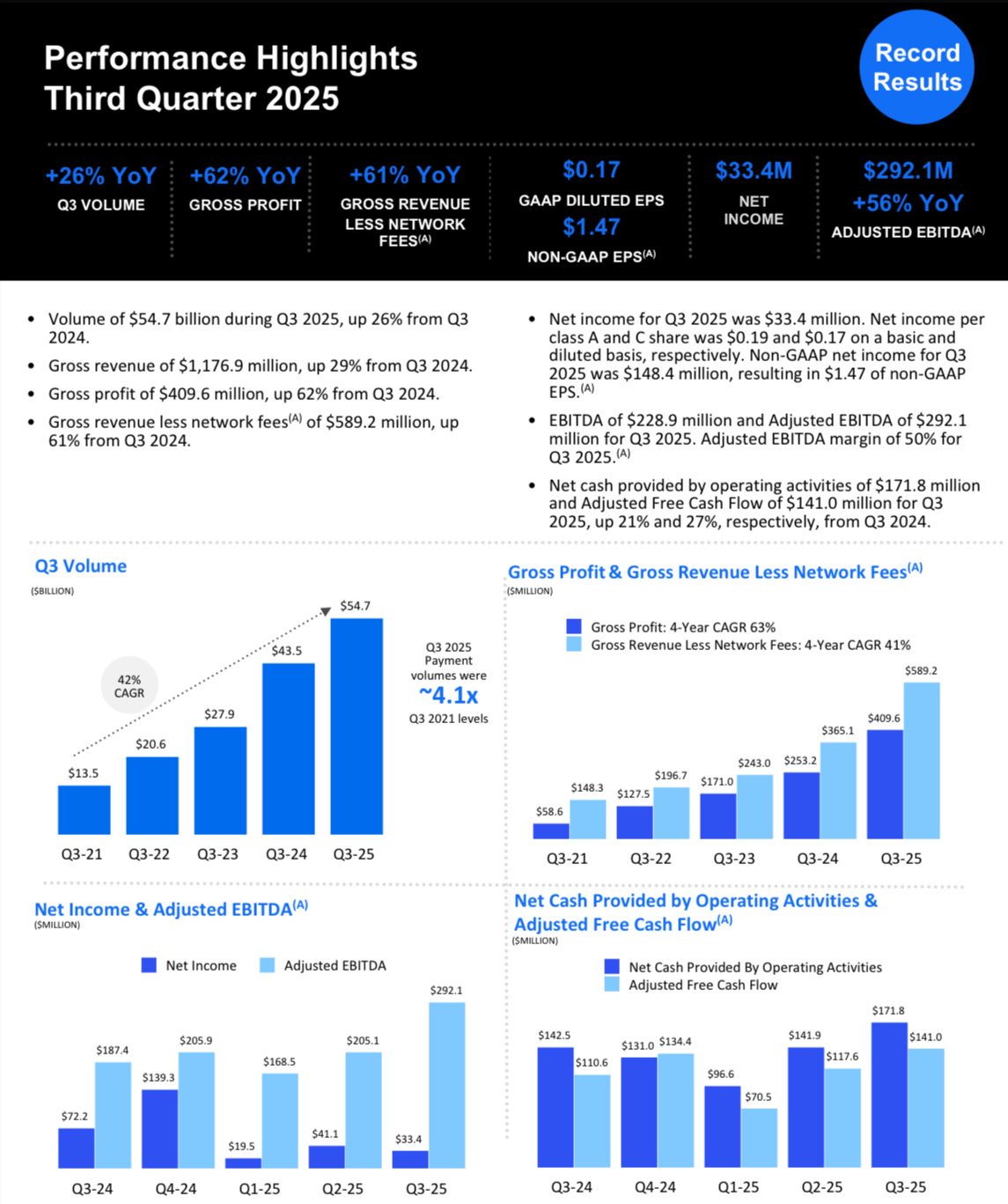

Shift4 reported $54.7 billion in end-to-end payment volume, up 26% year-over-year, with gross profit up 62% and adjusted EBITDA up 56% to $292 million.

Non-GAAP EPS came in at $1.47, which was up sharply from last year’s $0.98, and free cash flow jumped to $141 million for the quarter.

Every major metric is trending in the right direction: volume, margin, and cash conversion.