[Update] Shift4 (FOUR)

The valuation right now makes absolutely no sense to me.

I’ve written about Shift4 twice now. The original write-up back in September, and an earnings update in November after they announced a $1 billion buyback. Since then, the stock has steadily drifted lower while the fundamentals have only gotten better.

The valuation right now makes absolutely no sense to me.

As of writing, FOUR is trading around $66. On my math, that’s under ~6x 2027 FCF using management’s $1 billion FCF target and a share count that should come down meaningfully if they execute the buyback anywhere near these prices.

The stock has badly underperformed this year while the broader market has rallied. The weakness has been attributed to leadership transition noise, some cautious macro commentary from management, and lingering skepticism around the Global Blue acquisition.

None of that changes what matters: the business is executing.

Gross profit grew about ~62% last quarter. Margins expanded roughly 700 basis points with Global Blue now consolidated. Pro-forma topline growth is running above ~30%.

The $1 billion buyback authorization covers roughly 17% of diluted shares outstanding at today’s prices, and annualized cash flows look like they can fund 70–85% of that authorization.

This is a company growing 30%+ that the market is treating like a melting ice cube.

The Math Isn’t Mathing

I keep running the numbers different ways and arriving at the same place…

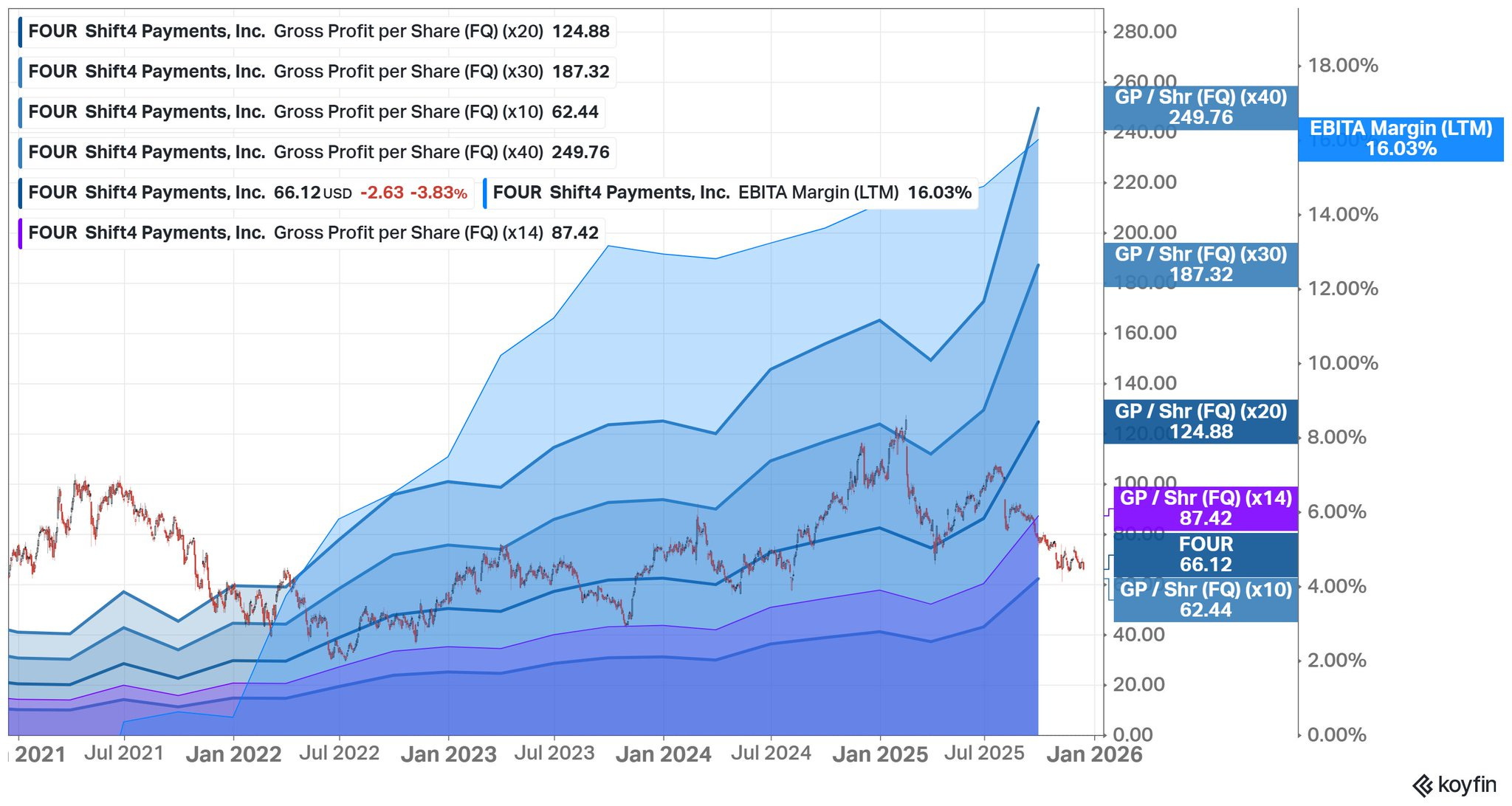

One way to see that clearly is by looking at gross profit on a per-share basis over time, and where the stock has traded relative to that. The chart below, put together by William (FundasyInvestor), plots Shift4’s stock price against various annualized gross profit multiples.

What jumps out immediately is where the stock sits today relative to its own history. Historically, Shift4 has bottomed around a ~3.5x annualized gross profit multiple. At current gross profit levels, that floor sits around $90 per share.

The stock is at $66.

The stock has essentially consolidated for five years while per-share gross profit has compounded steadily higher. At some point, the price has to catch up to the fundamentals. When it does, the move could be fast.

At 5x annualized gross profit, the stock would be worth around $125. At 7.5x, it’s $187. Those aren’t stretched multiples. Shift4 traded at 7.5–10x gross profit during the more expensive periods in 2021 and early 2022. Today it’s sitting below 3x.