[Update] Markel Group (MKL)

Markel reported Q3 results last week, and the stock’s up about 8% on what I’d call a classic Markel quarter.

Nothing crazy, just steady progress where it counts.

Operating revenue was up ~7%. Adjusted operating income grew ~24%. The insurance engine ran better. Cash generation stayed strong. Buybacks kept rolling. That’s really all I ask from this business.

What did change a bit is the way management tells the story. They cleaned up the reporting so it’s easier to see the core operating engines without the mark-to-market noise from the equity book.

It might sound like a small accounting tweak, but it matters. It lets long-term owners judge what’s repeatable and what’s just market fluctuation.

Insurance: Still the Foundation

The combined ratio came in at 93%. That’s the headline. Better underwriting and higher investment income did the lifting. A 93% ratio means they’re writing insurance profitably before any help from the portfolio. That’s how you earn the right to compound float. It’s not exciting, but it’s exactly what you want from the base of the pyramid.

Two main things stood out to me. Pricing discipline in specialty lines. No evidence of chasing growth by loosening terms. The improvement came from higher earned premiums and underwriting profits, not one-offs. That’s the slow, durable version of good.

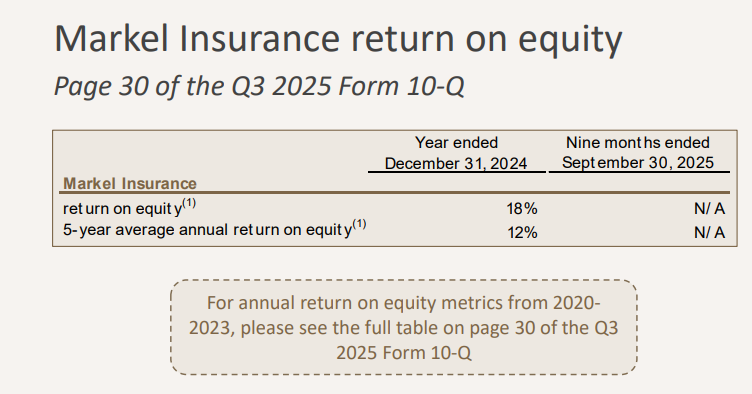

This feeds straight into returns. Insurance ROE was 18% in 2024, with a 12% five-year average. For a conservative writer that runs with low leverage, that is excellent. It says the core book is earning well above its cost of capital without financial engineering.

By division, U.S. Specialty did most of the work again with solid retention and firm pricing. International stayed profitable as marine, energy, and professional lines improved. Programs remained steady. Global Re is a smaller contributor now, but it still adds float.