[Update] Ferrari (RACE)

A couple months ago I published a post on Ferrari and mentioned that I had started a small position.

I used that write-up to walk through how I think the company works and why it tends to get valued differently than most things with four wheels.

![[New Position] Ferrari (RACE)](https://substackcdn.com/image/fetch/$s_!nRo8!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F85401831-2cb1-4294-b508-92d50be4d420_2400x1701.png)

TLDR; Ferrari lives and dies by control. They decide how many cars exist, they keep demand running ahead of supply, and the waiting list stays long on purpose. Over time, the compounding shows up through price and mix, with volume treated as something to protect rather than chase.

In that post I called it “scarcity is the product,” and I still think that’s the cleanest way to explain what makes the whole thing work.

So why am I back on it now?

Because the stock keeps sliding, and it’s finally starting to feel like the market is doing that thing it does with “perfect” businesses: it falls in love at 60x, gets bored at 45x, and starts nitpicking at 35x.

Meanwhile the underlying business is still… Ferrari.

What changed (and why the stock is selling off)

The catalyst for the reset was Ferrari’s Capital Markets Day and the 2030 plan. Management basically told the market: we’re going to keep executing, but don’t expect some crazy growth curve just because “EV” is a popular word this decade.

Two things landed poorly:

1) Lower long-term growth expectations.

Ferrari’s 2030 plan targets around €9B of net revenues and roughly ~5% revenue CAGR into 2030.

That’s not bad. It’s just not what a stock priced like a luxury tech platform wants to hear.

2) A more conservative EV mix.

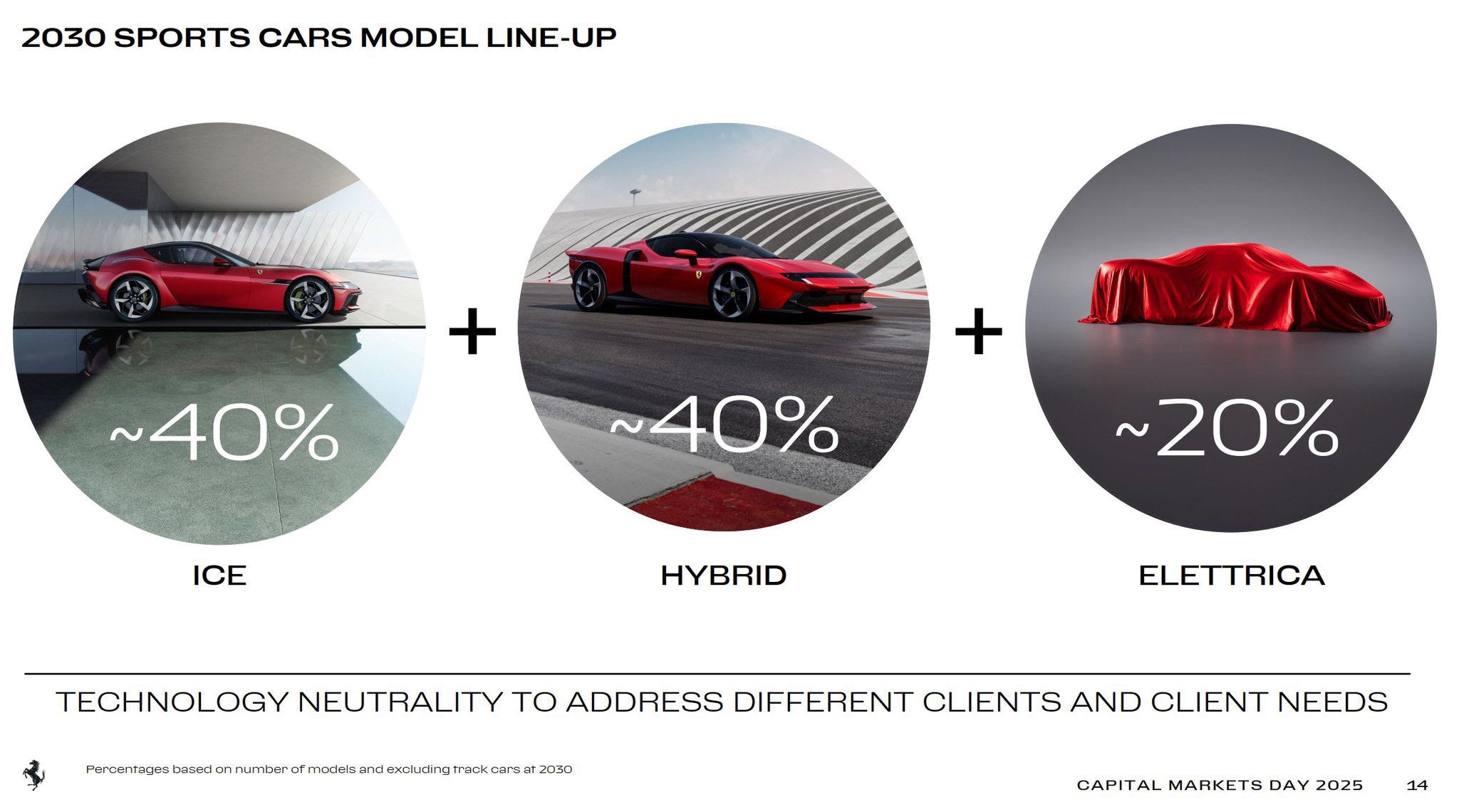

They also laid out a 2030 product line-up of 40% ICE, 40% hybrid, 20% electric.

In my opinion, that’s Ferrari protecting the franchise and matching what their clients actually want. But I get why the market initially threw a tantrum. “Only” 20% EV by 2030 doesn’t fit the typical narrative arc.

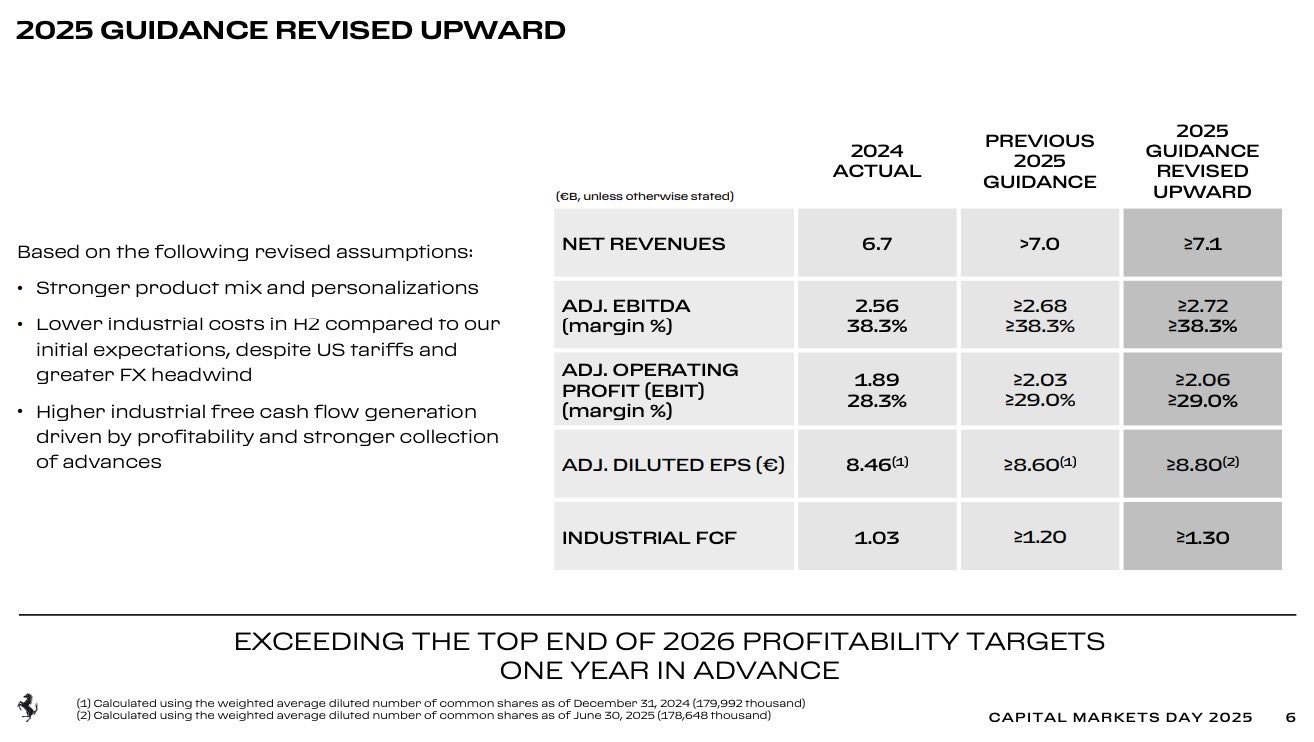

The funny part is they actually raised FY near-term guidance. Ferrari’s own commentary around Q3 2025 was “consistent execution,” with margins still looking absurd for anything that ships on four wheels.

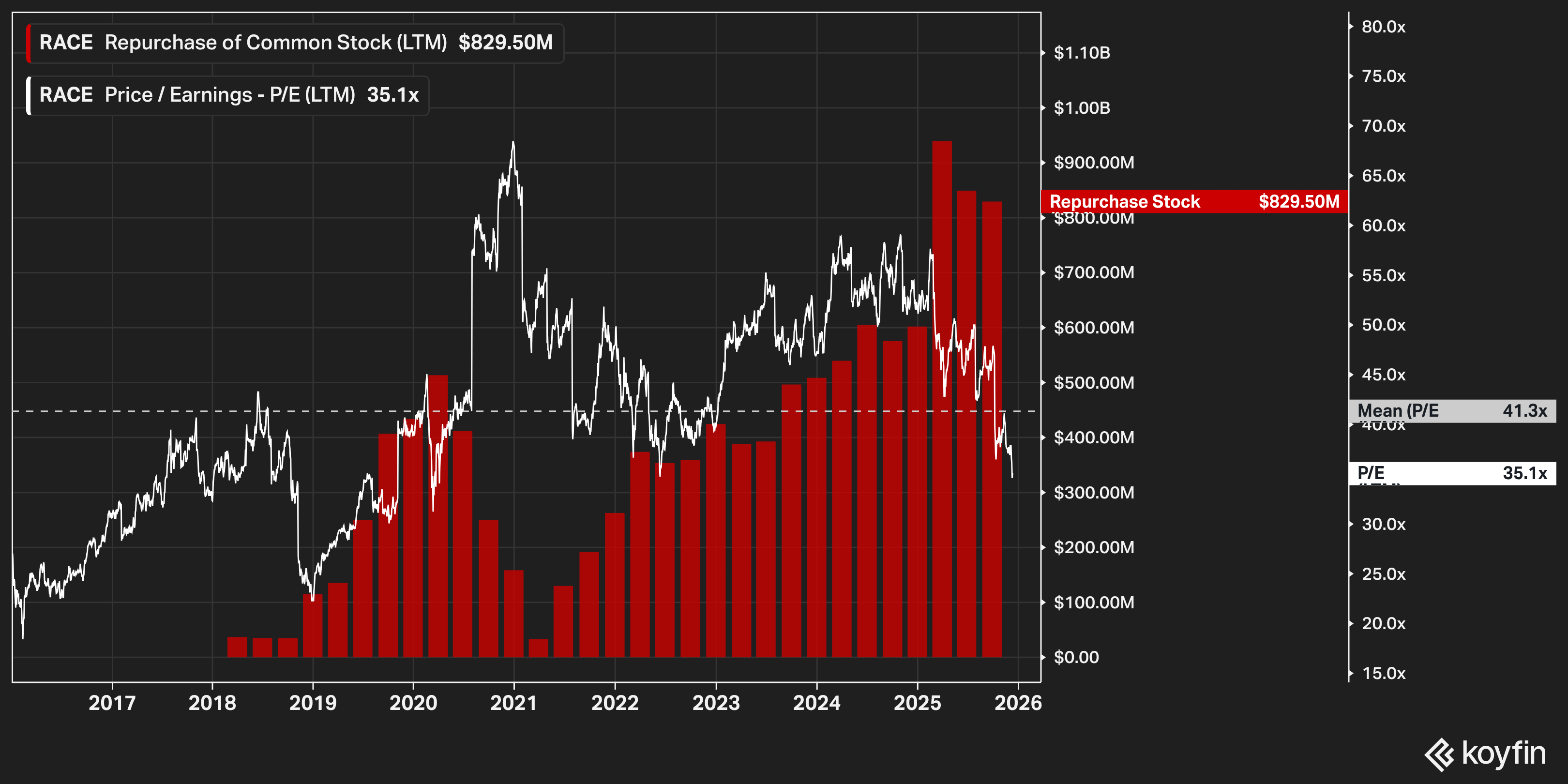

They’ve also continued buying back stock in size, including the eighth tranche of their multi-year program, with periodic updates through early December.

So the simplest explanation for the selloff is also the most common one: multiple compression.

This was a premium-multiple compounder that got even more premium during the “quality at any price” phase, and now the market is doing the reverse. It’s happening to lots of the usual suspects. Ferrari just isn’t used to being treated like a normal stock.

The business is still the business

Ferrari’s edge is not complicated, but it is rare.

They decide how many cars to make, they decide who gets them, and they protect the ladder that turns a first-time buyer into a repeat buyer into a “special series” buyer. In my prior write-up, I leaned heavily on the idea that Ferrari grows even when volumes don’t, because mix and personalization do the heavy lifting.

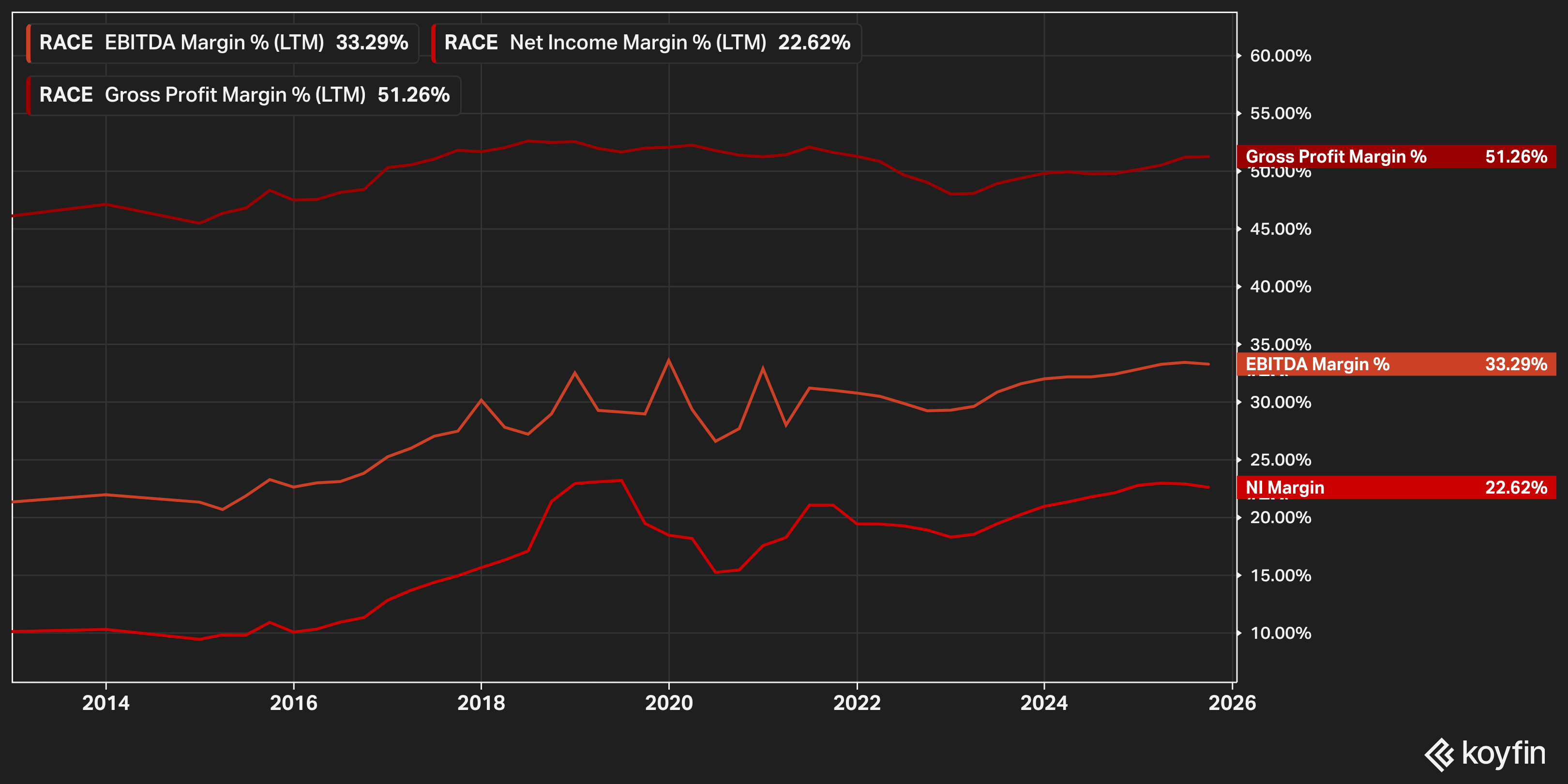

If you want to sanity check that this is real, don’t overthink it. Look at profitability.

Those are luxury-brand economics. Not automaker economics.

What the market is worried about (fairly)

I think there are a few legitimate worries hiding underneath the “multiple compression” headline:

Luxury demand risk. Even Ferrari isn’t immune to global wealth effects. If we get a real risk-off tape, luxury can wobble. The company is better insulated than most, but not magically immune.

China / region mix. Ferrari has been careful not to become overexposed to China, but luxury data out of China has been choppy across a bunch of brands. I don’t have perfect visibility into how much that matters quarter-to-quarter, but it’s in the stew.

The EV narrative premium is gone. This is the big one. Ferrari basically told the market it will move at Ferrari speed, not market speed. That’s probably the right decision for long-term brand equity, but it changes who owns the stock at the margin.

Shareholder overhang / positioning. There was also a notable event earlier this year: Exor sold a 4% stake in Ferrari in a large block, which can pressure a stock in the short term even if the long-term story is unchanged.

None of those break the thesis for me. They just explain why the stock can drift lower even while the business prints.

Capital allocation: they’re behaving like owners

When the stock is melting and the multiple is shrinking, buybacks can either disappear or get bigger. Ferrari’s have gotten bigger. That’s the version of buybacks I actually care about.

They already spend where they should spend: product, R&D, racing, and the stuff that protects the brand over decades. After that, the business still produces a lot of cash.

There just aren’t that many sensible places to put incremental capital without risking what makes Ferrari Ferrari. They’re not going to build a bunch of extra capacity and flood the market, and they shouldn’t.

So if the choice is between sitting on excess cash or retiring shares, I’m fine with them leaning into buybacks, as long as the price makes sense.

I don’t love buybacks at 50x earnings. Around 30x, I get it. At that point you’re buying a larger slice of the same franchise at a meaningfully better price than the market was offering a year or two ago, and that flows straight through to per-share compounding over time.