[Update] Coupang (CPNG)

I’ve been following Coupang for a while now, and after this quarter, I’m still convinced they’re one of the more quietly impressive stories in e-commerce.

Q2 wasn’t a massive blowout, but it was another solid step forward. Revenue came in at $8.5 billion, up 16% year-over-year. Gross profit hit $2.6 billion, and margins ticked up again.

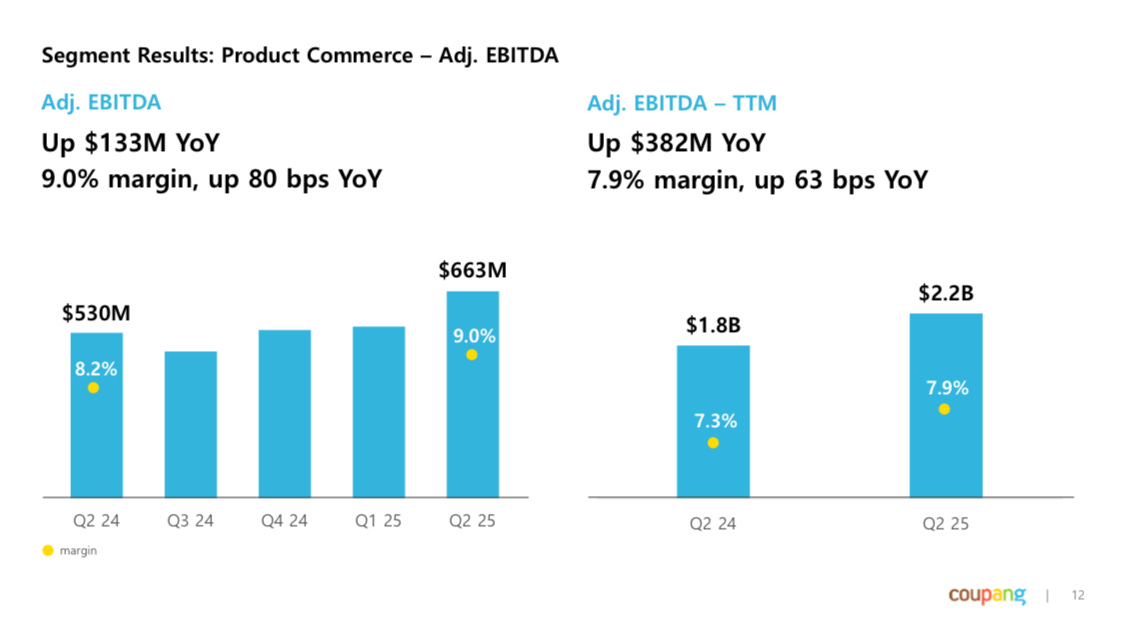

The real standout: their Product Commerce segment (the core business) posted 9% EBITDA margins. And that’s while still investing heavily in automation, AI, and international expansion.

So, what actually matters here?

Let’s start with the basics. Coupang’s bread and butter (the Rocket delivery platform, same-day and dawn shipping, first-party logistics) is still doing exactly what it’s supposed to do: deliver growth and throw off more cash as it scales.

Product Commerce revenue grew 14% YoY to $7.3 billion. More importantly, gross margins expanded by over 200 basis points to 32.6%. It’s coming from better tech, more automation, and a richer mix of high-margin categories like Fresh and FLC (their 3P logistics product).

But it’s also a reflection of their moat—the infrastructure they’ve spent a decade building, and the pricing power that comes with it. When you control the fastest and most reliable logistics network in the country, you don’t need to compete on price alone. You win on service, and you can hold pricing without losing share.