[Update] Alibaba (BABA)

There’s been a lot of noise around Alibaba over the past week and earnings are just around the corner. I want to walk through what actually happened, what matters, and what I’m watching heading into the print.

Some of this you’ve probably already seen. But the drama is worth unpacking because there’s genuine confusion around the name right now, and honestly, a fair amount of it is warranted.

Alibaba is a name I cover frequently here at Coughlin Capital. If you missed my last two posts on the company, here they are:

1260H List

You know how some movies get sequels that nobody asked for? This is that…

We saw it in November with the White House memo. We saw it Thanksgiving week with the Feinberg letter. And now we’re seeing it again. The timing is always suspicious.

Around 8 AM on the Friday before Valentine's Day, Walter Bloomberg tweets that the US is expected to add Alibaba to the Pentagon's list of firms allegedly aiding the Chinese military. Stock immediately starts selling.

Less than an hour later, the Pentagon actually publishes the updated 1260H list on the Federal Register. Alibaba is on it, along with BYD, Baidu, Huawei, NIO, and a handful of others.

Then, roughly an hour after that, the entire list gets yanked. No explanation…

I want to explain what this list actually is, because I think a lot of people see “Pentagon” and “military” in the same headline and assume the worst — even though, as of now, Alibaba is not on the list.

The 1260H list is basically a name-and-shame list. It bars the Pentagon from buying goods and services from companies on it. That’s it. It doesn’t restrict US investors from owning shares. It doesn’t trigger sanctions. It doesn’t trigger trading bans.

It is not the NS-CMIC list, which is the one that actually restricts securities purchases. Those are two very different things. And Alibaba has said publicly they do zero business with US military procurement, so even the one thing this list actually does is completely irrelevant to them.

We have a recent precedent for exactly how this plays out. Tencent and CATL were both formally added to this same list in January 2025. They both initially fell on the news but recovered. Both went on to make new highs. Both are operating today with zero business impact from the designation. Tencent literally called it “clearly a mistake” and went about their day.

Alibaba’s response was nearly identical. They said there was “no basis” for the designation and hinted at legal action. Xiaomi went through this exact process a few years ago, challenged it in court, and won.

Worth noting: the Feinberg letter behind all of this was written on October 7th — three weeks before the Trump-Xi trade truce. Months later it still hadn’t been formally acted on. And now it resurfaces right as Trump is actively de-escalating with China ahead of his expected April visit. The administration has spent months negotiating Nvidia chip sales to Chinese companies and shelving a proposed ban on China Telecom. The whole trajectory is “let’s make a deal.” And then someone publishes a list adding China’s biggest tech companies, it causes a selloff, and gets pulled within the hour?

I think somebody jumped the gun and somebody higher up wasn’t happy about it.

When something like this happens and the stock immediately dumps, I do find myself wondering who was positioned for it. Maybe that’s too cynical. But a list that briefly appears, causes a wave of selling, and disappears without explanation is awfully convenient timing for someone.

I’m not telling anyone what to do. But the algos don’t read context. You should.

China’s AI Landscape

That’s the headline that rattled the stock on Friday. Now let me talk about what’s actually been going on in China over the past two weeks, because it’s way more interesting than any Pentagon list.

The Lunar New Year kicked off what I would call “The AI War.” Every major Chinese tech company is burning cash to get consumers hooked on their AI platforms.

Alibaba committed 3 billion yuan (about $430 million) to promote Qwen through red envelope giveaways and subsidized shopping. Tencent put up 1 billion yuan for Yuanbao. Baidu dropped 500 million yuan on Ernie. ByteDance partnered with the CCTV Spring Festival Gala — think China’s Super Bowl — where they literally gave away luxury cars through their Doubao chatbot.

The Qwen campaign numbers are impressive. Within six days, the app processed over 120 million consumer orders and daily active users hit 58 million. That’s a 7x increase from baseline. Nearly half those orders came from people in smaller cities and rural areas. And about 1.56 million people over the age of 60 made their first online purchases through the app.

It’s wild to me that so many people over 60 were buying something online for the first time because of an AI chatbot… AI is already changing behavior in ways that I couldn’t even imagine for Alibaba.

What they’re really testing here though goes beyond a holiday promotion. The goal is to collapse the app layer into an AI agent layer. Instead of opening Taobao, searching, comparing prices, adding to cart, and checking out — you just tell Qwen what you want and it handles everything. Execution wasn’t perfect…

The system got confused on some orders (delivering Cudi when someone asked for Luckin Coffee is a rough start), merchants couldn’t keep up with volume, and some features still kicked you back to the underlying app. Growing pains. But the core pipeline worked at massive scale, and that’s the part that matters.

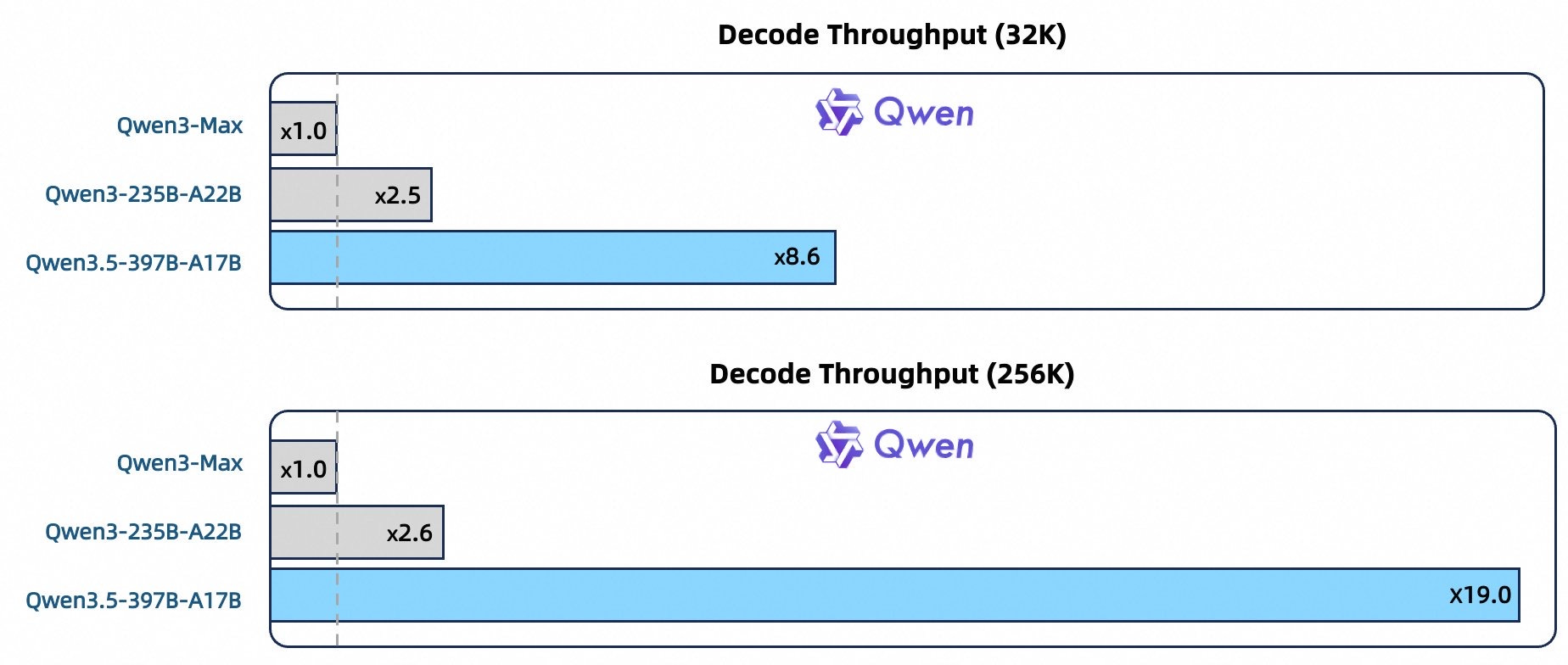

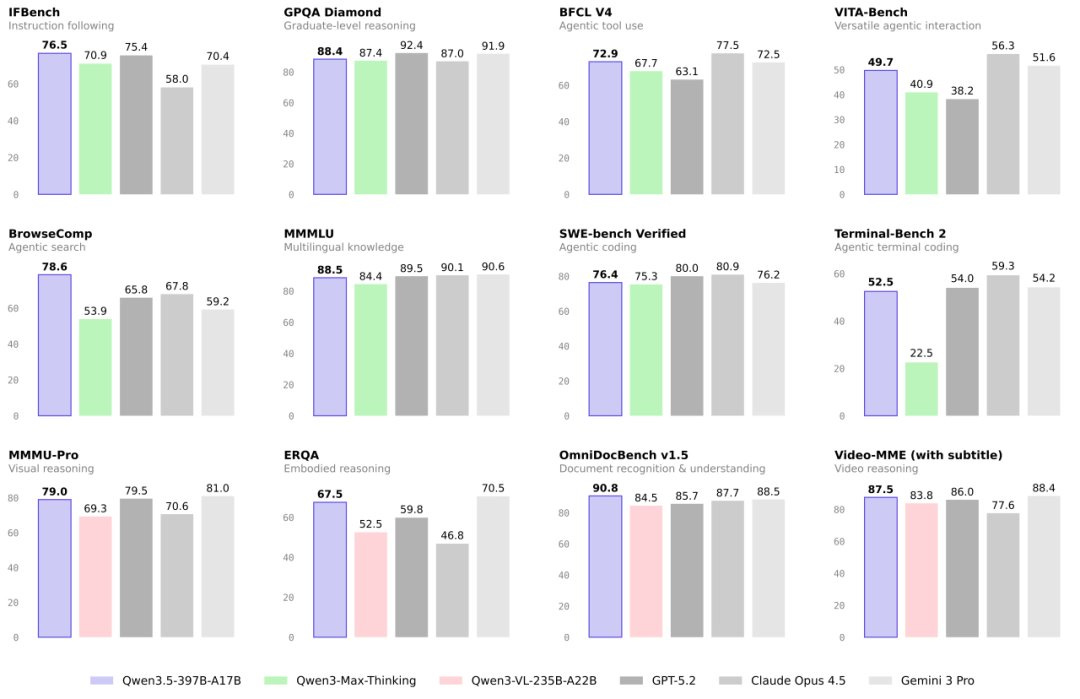

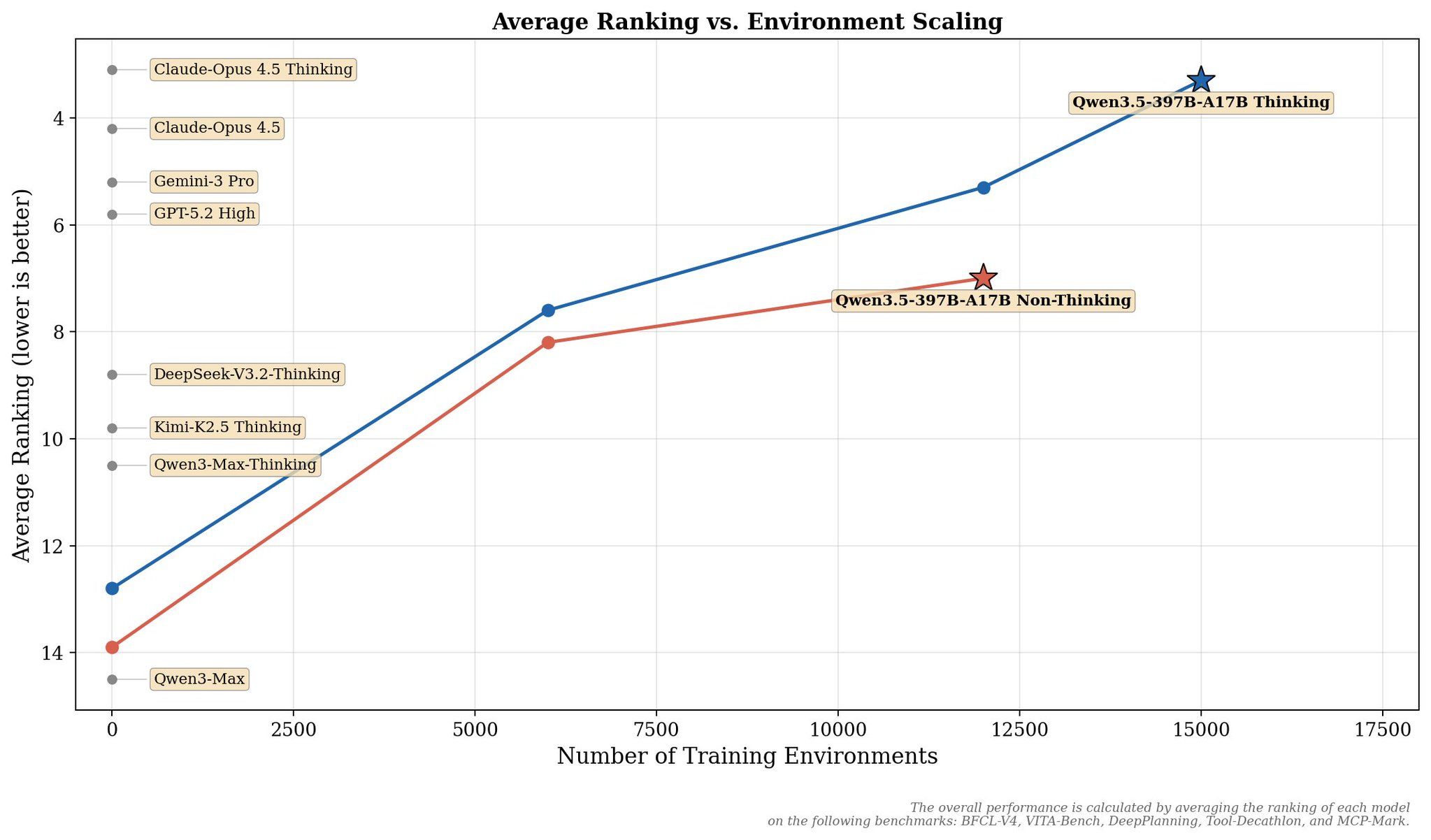

On the model side, Alibaba dropped Qwen 3.5 last Sunday. It’s a 397 billion parameter model built on a sparse mixture-of-experts architecture — only 17 billion parameters are active per query, which is how they get it to 60% cheaper and 8x more efficient than its predecessor.

Alibaba claims it outperforms GPT-5.2, Claude Opus 4.5, and Gemini 3 Pro on several benchmarks — but those are self-reported numbers, so take them directionally.

The honest picture is it’s strong on vision and agentic tasks, trails a bit on pure coding and math. Either way, this is top class model and it’s open-weight. Qwen’s open-source models have now crossed 900 million downloads globally, making them the most downloaded open-source AI models in the world.

This comes right after ByteDance released Doubao 2.0, also claiming to match frontier US models. ByteDance also dropped Seedance 2.0, a video generation model that went viral and drew immediate comparisons to DeepSeek’s breakout moment last year. Alibaba’s DAMO Academy unveiled RynnBrain, an AI model built for robotics. And DeepSeek is expected to release their next-generation model any day now.

Think about the DeepSeek moment from January 2025. One model release from one Chinese AI lab shook global markets and completely rewired how people thought about Chinese AI. That was one company. We’re now watching Alibaba, ByteDance, Baidu, Tencent, Zhipu, and DeepSeek all dropping major model upgrades inside the same two-week window. Another DeepSeek-type moment during this cycle wouldn’t surprise me in the slightest.

A year ago the consensus was “Chinese AI is behind.” Good luck saying that with a straight face now.

What This Means for Cloud (And Margins)

The AI excitement is real, but I think some people are going to miss the margin picture heading into earnings.

On the demand side, everything looks great. Alibaba Cloud is the largest cloud provider in Asia. Revenue grew 34% last quarter. AI-related products have posted triple-digit growth for nine consecutive quarters. They’ve committed at least $53 billion to AI and cloud infrastructure over three years.

You also have the Apple Intelligence partnership for China which is still sitting in regulatory purgatory — announced over a year ago, still not launched, which is getting old — but the deal isn’t dead.

And the Nvidia H200 situation continues to go back and forth. Beijing gave conditional approval for Alibaba, Tencent, and ByteDance to purchase over 400,000 units, but the terms keep shifting, some approvals reportedly aren’t converting to actual purchases, and there’s a domestic chip purchase requirement layered on top. Every week there’s a new headline and nothing ever feels fully resolved. Welcome to investing in China.

The competitive dynamics on the supply side, though, are intensifying and it’s going to show up in the numbers.

I covered this in my guidance call piece. ByteDance stockpiled high-performance chips before US export restrictions hit and is now using that excess capacity to undercut enterprise cloud customers at basically any price. Alibaba is matching in some cases just to protect key accounts.

And on top of that, everyone is spending like crazy on AI infrastructure at the same time — Alibaba, Tencent, Baidu, ByteDance, DeepSeek, all of them, all at once. Long-term that’s bullish because it means the ecosystem is maturing and compute demand keeps growing. Short-term it means pricing pressure and margin compression.

None of this should be a surprise though. Management already told us. They guided cloud growth to “in excess of 35%” when analysts were around 38%, and flagged that “Other Businesses” losses would widen due to investment in Qwen and AutoNavi. If cloud margins come in soft, just remember what’s actually happening — it’s a spending war, not a demand problem. Those are very different things.

I think it’s fine. This is a land-grab moment and the companies that build infrastructure and lock in users now are the ones that win the next decade. Alibaba has the scale, the ecosystem, and 600 million open-source downloads to show for it. Messy margins for a few quarters is the cost of playing offense.

Earnings

I’ve gotten a lot of questions about when earnings actually drop, so let me address it — because this comes up every single quarter without fail.

There is always confusion around Alibaba’s earnings date. Various sites are throwing around February 19th, the 20th, the 24th. IG has one date, Wall Street Horizon has another, TipRanks has another. Half the internet says “confirmed” and the other half says “estimated.”

Every. Single. Time.

Alibaba always officially announces the date with a press release at least a week in advance. As of right now, I haven’t seen that press release. Until I do, nothing is confirmed. My best guess is we’re looking at the first or second week of March. If they were reporting on the 19th or 20th, we’d already know about it.

Whenever it does land, the setup is about as negative as I’ve seen from this team. In my guidance call piece that I mentioned earlier, management walked down expectations across the board on their pre-earnings calls with the major sell-side shops — e-commerce slowing, quick commerce losses not narrowing, cloud growth “only” 35%, buybacks decelerating.

I said at the time I thought they were sandbagging. I still think that.

Cloud demand is outpacing supply. Eddie Wu said on the last call that they’re rationing GPU access because they can’t deploy servers fast enough. Quick commerce share has hit nearly 50% and unit economics have improved meaningfully since October. Regulators cracking down on subsidy wars effectively locks in Alibaba’s gains.

When management goes out of their way to walk everyone’s numbers down while the underlying business is steady improving, they’re either genuinely worried or setting up a beat.

The stock has pulled back to about $155 which is well off its highs of $190+ from last October. That’s roughly ~14x EBITDA for the largest cloud provider in Asia, the most downloaded open-source AI models on the planet, a dominant quick commerce position that didn’t exist a year ago, and a pending deal to power Apple Intelligence in China whenever that finally gets through regulators.

I know what I own and why I own it. Earnings can’t come soon enough.

Disclaimer: I’m just one investor thinking out loud. This isn’t financial advice. I own BABA and several other Chinese names. Do your own work before buying or selling anything.