Trip.com (TCOM): Cheap, Durable, Overlooked

A dominant, cash-rich platform quietly compounding as China’s middle class expands.

Some stocks need a story to work. This one doesn’t.

It benefits from something far more durable: people moving around again. You can see it in airports, train stations, and hotel lobbies. The behavior isn’t rebounding anymore, it’s normalizing at a higher level.

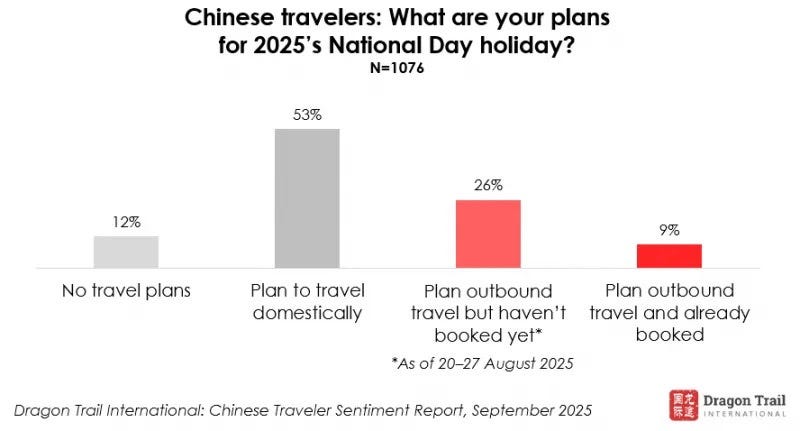

During the National Day holiday, which overlapped with the Mid-Autumn Festival and stretched to eight days, China recorded 888 million domestic trips, according to the Ministry of Culture and Tourism, up 123 million from last year’s seven-day break. Spending reached 809 billion yuan (about $114 billion), up 108 billion yuan year on year. That’s not a reopening bump anymore. That’s habit.

Flights are back above 2019 levels, rail traffic keeps setting records, and cross-border travel is steadily climbing. Incomes are rising, habits are sticking, and travel has become a line item in the average household budget.

That’s the backdrop for a company I’ve been watching closely. I don’t own shares yet, but it sits near the top of my watchlist. It’s the clear bellwether for China’s travel and consumption recovery, and maybe the cleanest way to own the long-term growth of the Chinese middle class.

If China grows GDP at even a modest 3–5% a year over the next decade (which I think is almost a sure bet) then travel will grow in tandem. Few companies stand to benefit more directly than Trip.com.