The Trucking Squeeze

Food for thought on freight, flatbed, and a short list of ways to play it.

I’ve been thinking about trucking/freight the last few days and wanted to write up some thoughts before I lose them. The more I poke at it, the more I think there’s a really intriguing opportunity here.

It started on the Insteel Industries (IIIN) earnings call last week. The stock fell about ~30% after the print, and I actually ended up starting a small position on Friday, but that’s besides the point…

If you don’t know the company, they make steel wire products. Boring business, sleepy call. But the CEO spent close to four minutes on flatbed tender rejections and freight costs. Steel wire CEOs don’t usually volunteer four minutes on freight. That did grab my attention.

“Freight costs, whether inbound or outbound, have risen substantially following the conflict with Iran, and it happened extremely quickly. It coincided with other factors that reduced driver availability. The practical impact is much higher diesel costs and fewer drivers, which means our costs have gone up, and many of our loads have been rejected by carriers who can find loads that pay more...

I was reading that in the flatbed sector, more than 40% of loads tendered to carriers have been rejected across the economy. We are dealing with something out of our control, but it is our responsibility to manage it from a cost point of view. We debated surcharges versus price increases, and we have elected to increase our prices.” — H.O. Woltz

A few days later I was scrolling X when a post from Unemployed Value Degen (@SFarringtonBKC) made me pause.

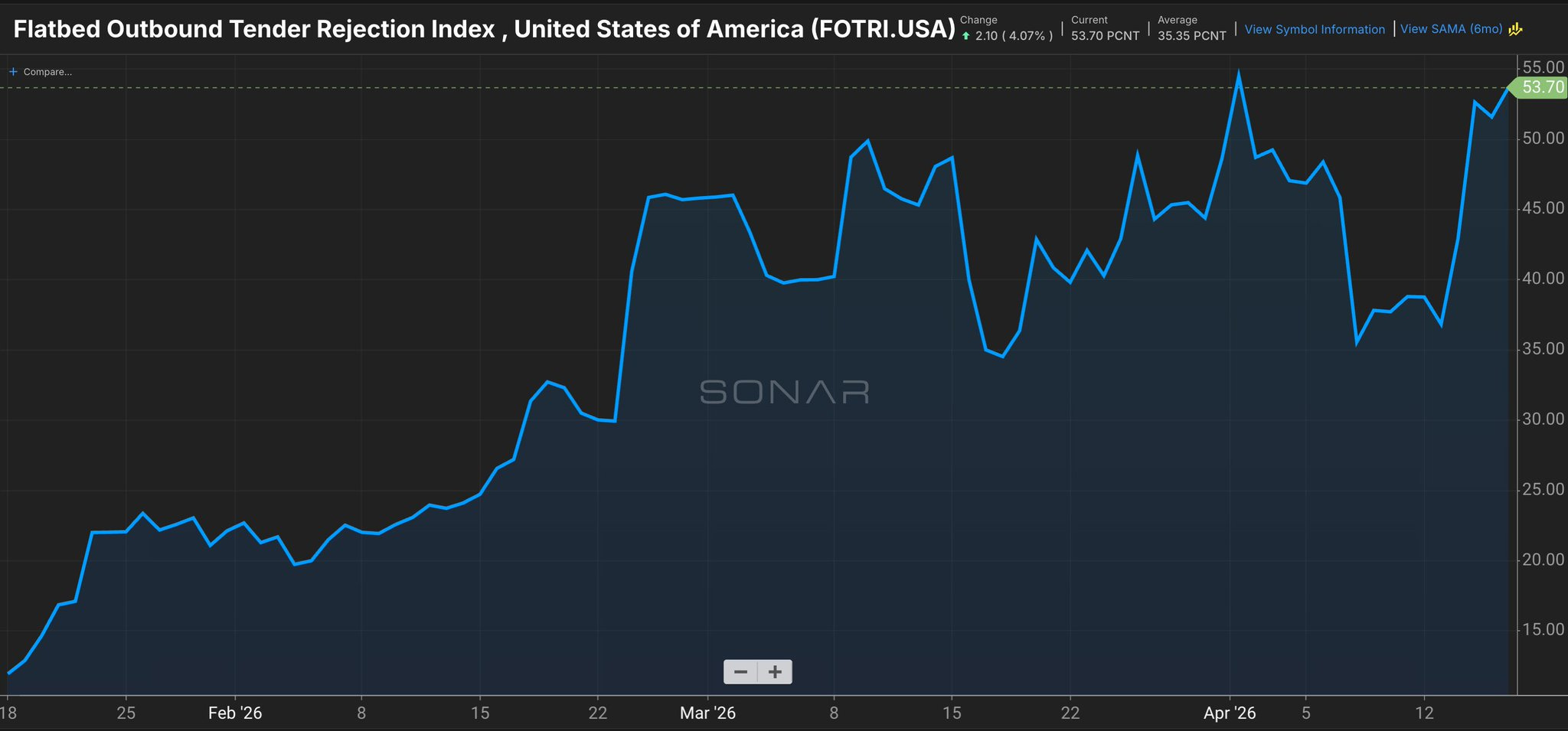

He reposted a tweet from Craig Fuller showing flatbed tender rejections above ~54%, alongside a note about industrial demand ramping through data centers, power plants, transmission lines, and pipelines.

My mind went straight back to Woltz on the Insteel call. Same exact story, just coming from the other side of the freight transaction.

If you don’t spend much time thinking about freight, quick context on what “flatbed” means. Flatbeds are the open-deck trailers with no walls or roof. They haul the big, heavy, awkward stuff. Wind blades, steel coils, transformers, oil and gas equipment, construction gear, pre-fab modules. If it’s a pain to shove in a box, it usually goes on a flatbed.

With that in mind, the domestic industrial buildout is clearly strong and it’s not hard to squint and see a mini industrial boom.

Data center capex is running hot. The grid needs enormous transmission and substation work just to catch up. Oil and gas equipment is moving to offset whatever barrels we aren’t importing. The Big Beautiful Bill pushed companies toward American sources for infrastructure construction, and whatever your politics, that policy is working at the margin.

American factories are firing up.

And all of it — the transformers, the turbines, the pipe, the steel — has to move on flatbeds. If the buildout is multi-year, so is the tightness.

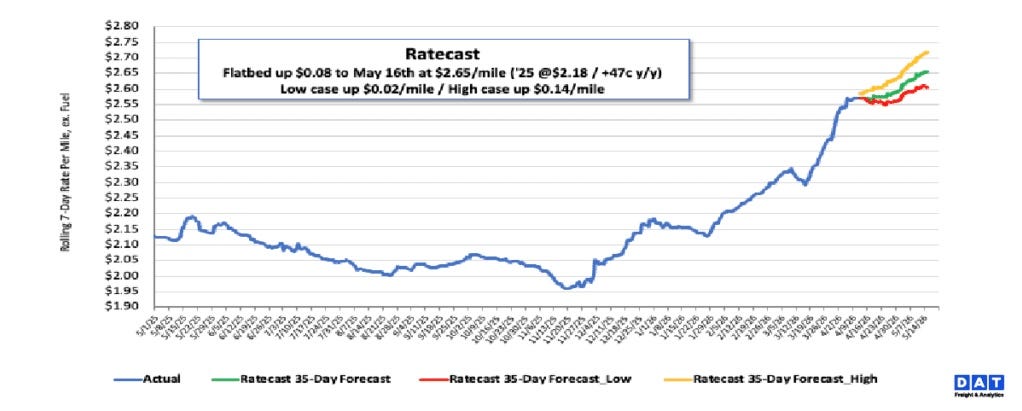

It’s not just the rejection data either. Spot rates are ripping too. National flatbed went nowhere for most of 2025, and then late last year it started climbing and just hasn’t stopped. DAT has it at $2.65/mile by mid-May, up 47 cents from the same time last year. Call it ~22% YoY.

All of which got me sitting down and thinking about how to actually play it.

So how do you play it?

The annoying answer is there aren’t many clean ways in. Flatbed is a sliver of the trucking world, and Daseke, the name that used to be the obvious pure play, got taken private by TFI back in 2024. What’s left is a short list of names with varying degrees of exposure.

These are the four most obvious public-market ways to get exposure, at least in my view:

Universal Logistics (ULH)

Closest thing to a flatbed pure play on US exchanges. I’ve seen estimates that around 35% of revenue is flatbed, though the company doesn’t break it out cleanly.

Layer in wind-energy project cargo, heavy-haul, and a big owner-operator network, and you have a real industrial transportation franchise dressed up as a boring trucker. An asset-light model flows more of the rate upside to the company than a fleet of leased trucks that still have to be paid for whether they’re moving or not.

It’s trading around ~1x book vs ~2.5x (ish) historical range, and it’s a controlled company, with Chairman Matthew Moroun owning roughly 73% of the shares. His cost basis is around $25 against a stock price in the mid-$20s. That’s strong alignment, with some take-private tail risk.

Landstar (LSTR)

Asset-light model like ULH, which I think I’d prefer in a tightening cycle. Landstar runs on an owner-operator network (they call them BCOs) with real flatbed and heavy-haul exposure, not just dry van. Not a pure play, but a quality franchise that benefits directly when capacity tightens.

Also less single-name risk than ULH. It’s larger, more liquid, and doesn’t have a controlling shareholder. The trade-off is you pay for that quality in the multiple.

Heartland Express (HTLD)

Mostly dry van truckload rather than flatbed, but tight capacity is tight capacity and the whole sector tends to move together when rates turn. Historically a very well-run operator, until they took on real debt with the Smith Transport and CFI acquisitions in 2022.

The last couple years have been messier than the old HTLD crowd would’ve wanted. They’ve paid the debt down from ~$494M to ~$160M and management is targeting debt-free by 2027, but operating results are still ugly. It’s trading at what looks like cyclical trough numbers, and if the turn is real, pretty asymmetric.

Werner Enterprises (WERN)

One of the more out-of-favor names in the group, and a higher-torque way to express a freight-cycle turn. It’s truckload plus logistics, and results have been ugly through the downturn. CEO Derek Leathers recently called current rejection rates “COVID-like” in public remarks, which tells you where they think the cycle is.

If rates really rip, WERN should have upside. If they don’t, it can keep grinding. But I do think it’s a legitimate way to play the cycle if you’ve got conviction.

I definitely don’t think a broad transportation/trucking ETF gets you what you want here.

Too much dry van exposure that isn’t levered to this specific industrial tailwind, plus the big rails with their own issues. It’s a narrow trade and I think you have to pick names. For now, ULH looks like the cleanest pure-ish play.

While I keep doing my own work on ULH, Unemployed Value Degen already published Part I of a small-cap trucks series on the exact same name. Go read it.

He walks through the flatbed exposure, the valuation (ULH trading around ~1x book vs a ~2.5x historical range), the accounting quirks, the Moroun ownership piece, and his base and bull case targets. He also just dropped Part II on Forward Air.

If you aren’t already subscribed to his stack, fix that.

What I’m actually watching

At this point, I’m not really trying to figure out if something is happening in freight. I think that part is pretty clear. The real question is whether this is just a sharp squeeze that fades or the front end of a real turn.

The setup definitely looks a little too obvious to ignore. You’ve got three years of pain in trucking, fewer trucks in the system, tariff certainty, and now demand picking up into a backdrop where a lot of industrial stuff still needs to move.

What makes it interesting, and honestly a little annoying, is that there aren’t many clean public-market ways to express it. ULH is still the one I keep coming back to. Landstar makes sense too, and the others would probably work if trucking broadly turns, but ULH still feels like the cleanest way to play the idea.

A few things nagging at me

I could also be very wrong here… I’m still getting up the curve on trucking, and it’s easy to overread a couple loud data points. I mean I think it’s very unlikely but, it’s entirely possible this could just be an Iran-driven spike — diesel settles, capacity loosens, and the whole thing cools off.

But I also think there’s a real chance people are leaning too hard on the old playbook here. If this is being driven by a genuine domestic industrial buildout, and truck supply has already been beaten up for years, this may not be some quick little squeeze that disappears next month. It could be a better and more durable setup than the market is giving it credit for.

That doesn’t mean I’m smashing the buy button tomorrow morning.

But directionally, this has gone from something that caught my attention to something I feel like I should probably be acting on. The only real question now is what the best vehicle is.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Might be interesting to listen to the recent interview with Craig Fuller on Thoughtful Money regarding the freight industry. He was very bearish in November, now the opposite, super bullish.