The SaaSacre

The market is shooting first and asking questions later.

I don’t know if you’ve noticed, but software stocks are kind of getting massacred right now. AI is going to kill all of them, or so the thinking goes.

A SaaSacre, if you will. I stole that from someone on Twitter but it’s too perfect.

The carnage has been broad and ugly. Some of the biggest names in software are down 35-75% from their all-time highs:

Salesforce (CRM): -37%

ServiceNow (NOW): -37%

Workday (WDAY): -40%

Adobe (ADBE): -55%

Atlassian (TEAM): -74%

The Trade Desk (TTD): -75%

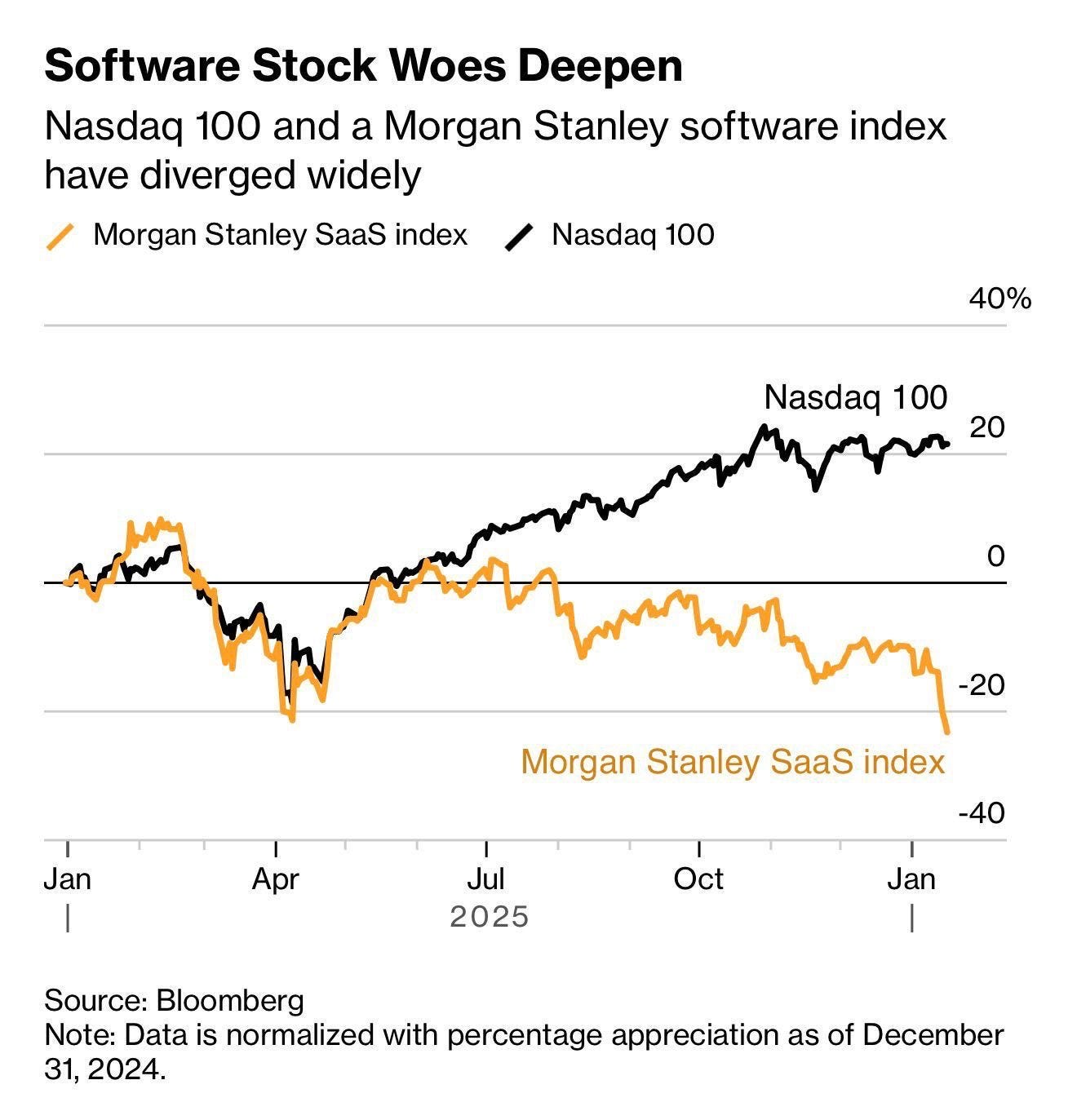

Most of that damage happened in the last twelve months. Meanwhile, the Nasdaq 100 is up about ~20% over the same period.

The Morgan Stanley SaaS basket is now trading at 18x forward earnings. That’s the cheapest on record. The historical average? Over 55x.

So what’s going on?

Basically the market has decided AI is going to murder software. Every time OpenAI or Anthropic announces something new, these stocks dump.

The latest trigger was Anthropic launching Claude Cowork earlier this month. Some Google engineer went viral saying it recreated a year of her team’s work in an hour. I have no idea if that’s true or wildly exaggerated but it doesn’t really matter. Investors saw it and panicked.

Honestly, the bear case makes a lot of sense. I mostly agree with it.

Most SaaS companies charge per seat. If AI makes one person do the work of three people, companies need fewer seats. Fewer seats = less revenue. And if AI eventually replaces the software entirely? Then you're just… cooked.

I mean, it’s not difficult to see why investors are nervous.

I’ll admit, I’ve never really understood software as an investment. These stocks always traded at insane multiples and I could never figure out the moats. Every SaaS company tells the same story. Recurring revenue, high margins, sticky customers, massive TAM. But like… what actually makes one CRM different from another? What stops someone from just building the same thing?

I never had a good answer so I just stayed away.

The funny part is AI is now kind of proving my skepticism was somewhat valid. A lot of these businesses might be way more vulnerable than their valuations implied. When everyone was high on growth and multiples didn’t matter, nobody asked the hard questions. Now they are. And a lot of people don’t love the answers.

So where does that leave me?

On one hand, valuations are genuinely starting to look attractive now. These companies are trading at forward P/Es in the high teens or low 20s. They’re still growing. Still printing cash. That seems… cheap?

On the other hand, I still can’t get comfortable.

Adobe doesn’t do it for me. I can totally see a world where generative AI makes Photoshop and Illustrator way less essential. When anyone can create professional images with a prompt, what exactly are you paying for? I don’t know.

Salesforce doesn’t do it for me either. Growth has slowed to high single digits. They keep talking about Agentforce but it hasn’t shown up in the numbers yet. And Microsoft is right there waiting to eat their lunch.

ServiceNow, Workday, HubSpot, Intuit… I look at all of them and I just don’t have conviction. I can’t explain what makes their moats durable when AI can automate half of what they do.

Maybe I’m dead wrong. Maybe this is a generational buying opportunity. But I genuinely don’t know which names survive and which ones don’t. And if I don’t know, I shouldn’t pretend like I do.

That said.

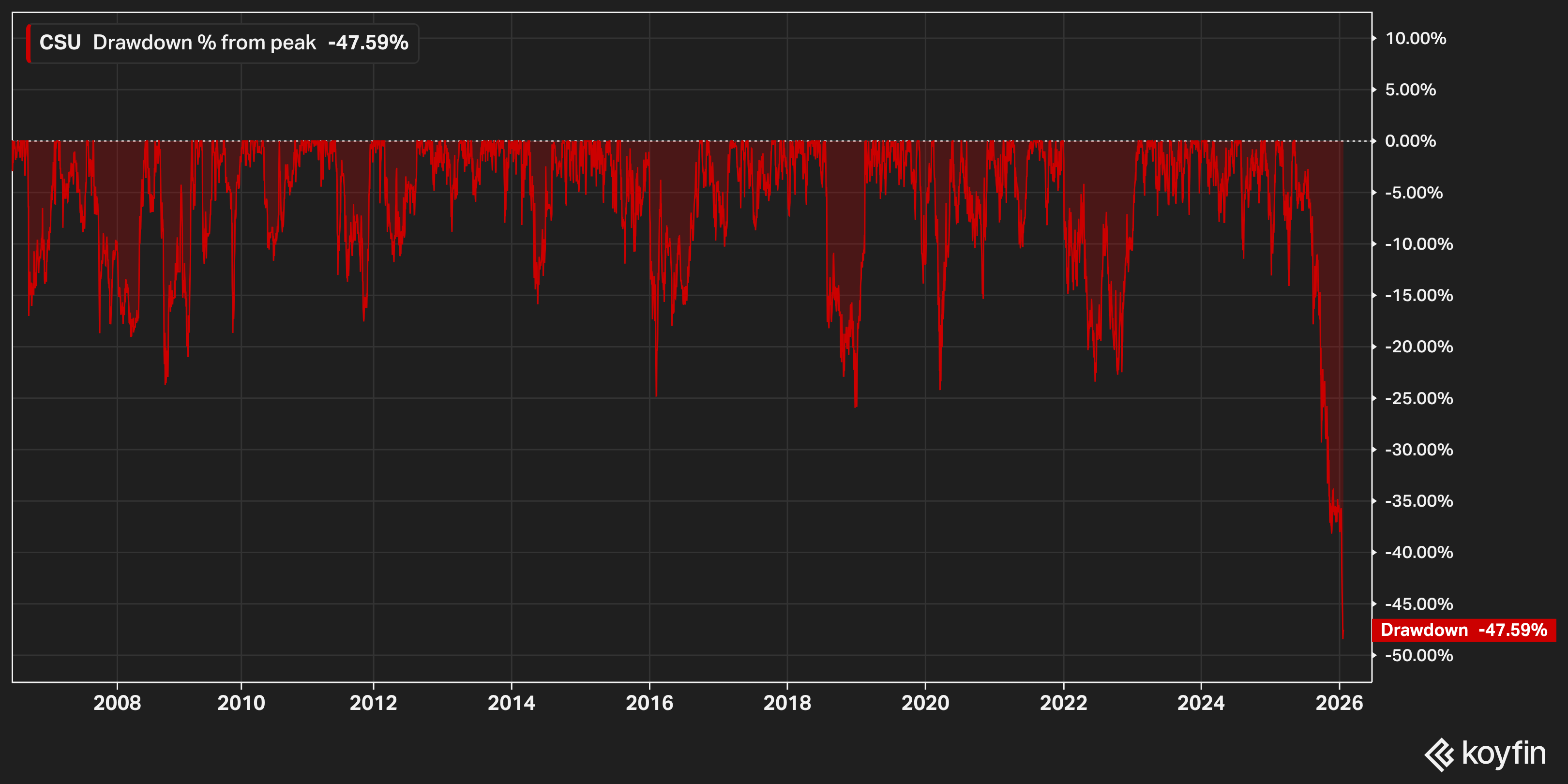

There is one name that actually interests me: Constellation Software.

Constellation is this weird Canadian company that just buys vertical market software businesses. We’re talking tiny, boring, unglamorous stuff. Marina management software. Transit scheduling systems. Library software. Notary compliance tools. Software for running a cemetery. Literally nobody cares about these businesses except the people who use them.

They’ve made over 1,000 acquisitions since 1995 and they never sell. The founder Mark Leonard is basically the Warren Buffett of software except even more secretive. Since their IPO in 2006, the stock has compounded at over 30% annually.

The stock is down about ~45% from its highs. Even fintwit's favorite compounder got swept up in the SaaSacre.

But I’ll explain why it appeals to me when Adobe and Salesforce don’t…

Constellation doesn’t depend on any single product. They own hundreds of small businesses across dozens of verticals. If AI disrupts one, they have 999 others. If an entire vertical disappears, they’ve already diversified away from it.

And the type of software they own is just fundamentally different. Enterprise CRM and marketing automation? Yeah, Microsoft and AI can probably come for that. But the scheduling software for a small-town transit authority? The compliance system for some niche manufacturing process? AI isn’t touching that anytime soon. It’s too specialized. Too customized. Too deeply embedded in workflows nobody outside that industry even understands.

These are mission-critical systems of record. Customers don’t rip them out because it’s not worth the headache. The revenue per customer is small but the retention is insane.

And now, for the first time in a long time, the valuation actually makes sense.

Constellation currently trades at ~18x earnings and ~16x FCF. The historical averages are closer to ~30x. It’s the cheapest it’s been in nearly a decade.

I'm not saying I'm buying tomorrow. Software is admittedly outside my wheelhouse and I'd want to do more work before pulling the trigger.

But if I was going to put money into this space, that’s where I’d go. Not Adobe. Not Salesforce. Not ServiceNow.

I’d rather own the guy who quietly buys hundreds of boring mission-critical businesses at reasonable prices than bet on any single product surviving the AI apocalypse.

The bigger picture here is that I think the market is probably overreacting. Shooting first, asking questions later.

Only 6% of companies had AI agents actually in production as of mid-2025 according to Bank of America. The disruption everyone is pricing in hasn’t really happened yet. Channel checks say customers aren’t canceling, they’re just being cautious. The fundamentals haven’t collapsed.

But I also think the market might be onto something. Some of these businesses probably are more vulnerable than they looked two years ago. The seat-based model has real problems if AI makes everyone more productive, the rebundling risk is real and the competition is certainly real.

So I’m mostly just watching right now. Trying to figure out who has actual moats and who was just riding a wave.

Constellation is the one name where I feel like I understand what makes it different. Everything else? I’m honestly not sure.

Sometimes the smartest thing you can do is just admit you don’t know.

Disclosure: I don’t own any of the stocks mentioned. That could change.

As a business owner operator, I do think NOW offers an irreplaceable service. And they have shifted their pricing to seats + AI assists from agents and are deploying integrated agents into their systems.

Also re Adobe - I am a hobby photographer. Someone could pay me to switch off Lightroom and it would be a hard choice.

I’ve tried to edit photos with AI and it just doesn’t work - as a creator I need full control and translating internal visuals/thoughts into prompts cannot convey that.

That doesn’t mean the product that can won’t come in the future - it may. But Adobe is integrating all of the best models into their suite while allowing full control to the creator.

I dont think there’s any short term catalyst here for them but I imagine they will execute through the sentiment. They won’t ever return to the premium multiples they once commanded but that’s ok.

Most of the others I’m in full agreement with.

Great write up. CSU is definitely the most interesting of the bunch.