The Illusion of a Healthy Consumer

Every now and then I put my macro cap on and try to make sense of the world outside the handful of businesses I actually understand. I always feel a little clueless when I do it.

I am a bottom-up stock picker trying to squint at the big picture. But if you stare at markets long enough, you start trying to connect the dots anyway.

The Black Friday “record spending” headline was one of those times. It popped up everywhere, and it was hard not to at least try to make sense of it.

U.S. shoppers spent a record $11.8 billion online on Black Friday, up a little over 9% from last year, according to Adobe. Salesforce puts total U.S. Black Friday online spending at around $18 billion, up about 3% year over year.

Over the weekend my entire X feed was wrapped up in this. And true to form, the platform delivered three completely different reactions.

Camp One looked at the record and declared the consumer invincible. Strong spending, no recession, bears in shambles, etc. You know the type.

Camp Two (myself included) squinted at the number and smelled something off underneath. Record spend, sure. But driven by what, exactly?

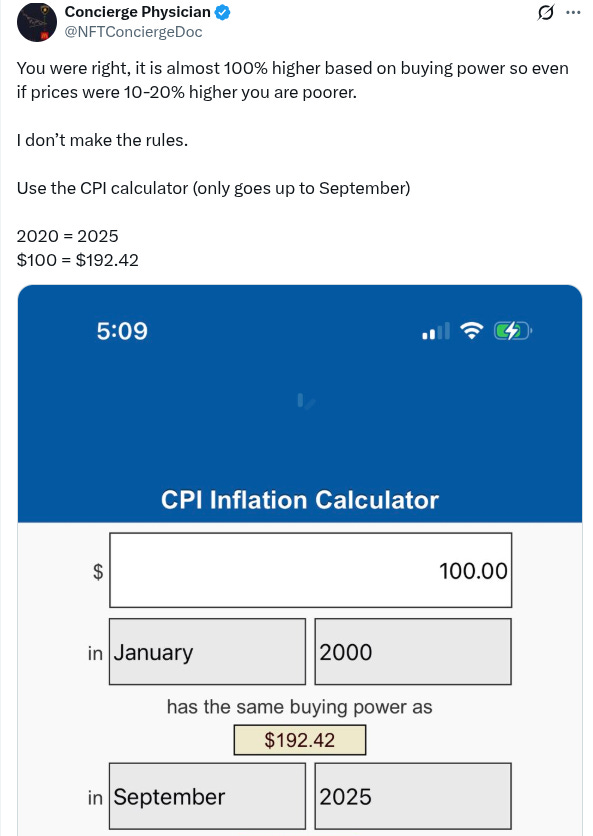

And then there was Camp Three. This is the camp that reminds you X is one of the great petri dishes for confidently wrong people. My personal favorite was a guy insisting that $100 five years ago is now basically $150, backed by a screenshot of a CPI calculator. Checkmate, inflation deniers.

Except he plugged in the wrong year. Used January 2000 instead of 2020. The man proved, with receipts, that he could not operate a free website. And walked away thinking he’d made a point.

Same headline number. Two legitimate camps. And one guy doing… whatever that was. It was a good reminder of how elastic these macro narratives can get depending on where you stand—and how much faith you should put in CPI calculator screenshots from strangers on the internet.

So on the surface, this looks like classic “consumer is fine, stop worrying” material. But when you dig into the details, the picture gets more interesting. And by interesting, I mean worrisome.

According to Salesforce, the average selling price rose about 7%, while online order volumes fell 1% and units per transaction dropped 2%.

In plain English, people spent more dollars but bought fewer things.

Then there’s the financing. Adobe notes that “buy now, pay later” usage was up high single digits year over year on Black Friday alone, driving roughly three quarters of a billion dollars in spending—about 6% of all digital sales that day. Over the full holiday period, they expect more than $20 billion will be spent through BNPL, up around 11% versus last year. CBS and others are also reminding everyone that credit card debt and delinquencies on short-term loans have been creeping higher.

And Salesforce’s own read is that luxury apparel and accessories led the way.

So you end up with an odd mix: record spend, fewer items, more installment payments, softer physical traffic, and strength skewed toward the top of the market.

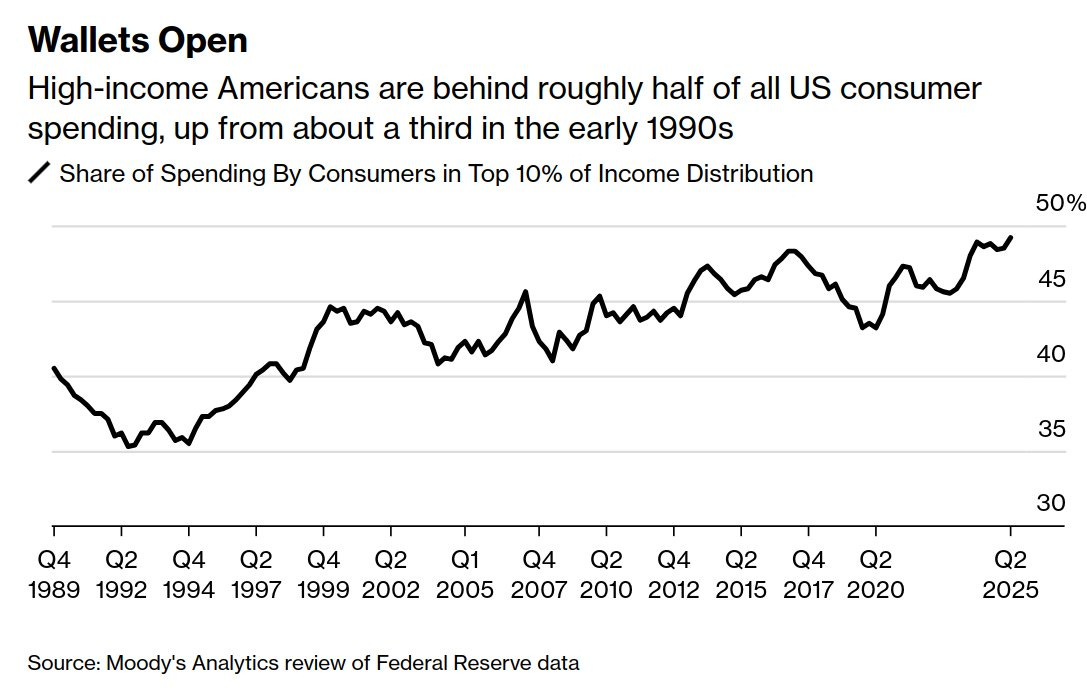

That does not look like a broadly booming, carefree middle-class consumer to me. It looks more like a split one. This is where the whole K-shaped idea comes in.

At the top of the K, life still looks pretty good. If you are in the top 10% or tied into the AI and cloud profit machine, you have assets that went up, equity compensation, and plenty of ability to keep spending. Those households show up very clearly in the Black Friday numbers. They are also a big reason you can hit a “record” even when a lot of people are uncomfortable.

At the lower leg of the K, it is a different story. Wages have not fully kept up with the cumulative jump in prices. Housing, food, and services are still expensive in level terms. Rising BNPL usage and higher delinquencies do not prove the bottom is falling out, but they are consistent with a world where a growing slice of people are stretching to keep up.

Those two realities get averaged into one clean headline. “Record spending” is technically true, but it does not tell you how that spending is distributed or how strained parts of the distribution feel.

So where do I land in that debate?

With all the usual disclaimers. I am not a macro economist. I do not have a magic model. And if we replay this in a couple of weeks/months there is a good chance I will look wrong on some, if not every part of it. Everything I say here should be taken with a grain of salt.

That said, I lean toward the view that this Black Friday record is not as good as it looks. It feels like a number being held up by the top of the K and nominal price increases, while the bottom half of the distribution quietly tightens its belt.

You can see the same tug-of-war in the Fed conversation. Unemployment is near a four-year high. Consumer confidence is around a seven-month low. The broader backdrop is “tighter budgets,” in Reuters’ words. But at the same time, the top 10% are spending aggressively. That strength supports the headline data, even if a big chunk of households is living a very different reality.

If that read is roughly right, I think the path of least resistance for the Fed is to keep easing carefully. A small 25bp cut in December wouldn’t surprise me, followed by a pause while they wait for more proof that the weaker side of the K is under real pressure, not just grumbling.

That’s not a bold prediction. It’s just the path that lines up with an economy where the averages look okay, the tails are stretched, and the data is noisy. Also, it obviously doesn’t help that some official economic numbers have been delayed, revised, and in some cases completely wiped from history… which means the Fed is sometimes flying with partial instruments.

Could I be wrong? Absolutely. Predicting macro is a fool’s game, and I try not to build my portfolio around these kinds of calls.

But if you force me to have an opinion, this is where I am today:

Black Friday’s record is a great headline and a messy signal. It tells you people are still spending. It does not tell you how much of that is the top 10% and how much is the rest of the country stretching with credit and BNPL. It doesn’t resolve the debate over “strong consumer” versus “fragile consumer.” It just sits on top of a K-shaped reality that hasn’t gone away.

So I read the record as neutral at best, and quietly bearish underneath. Not a crisis. Not a crash. Just a reminder that nominal records can be set in economies that are more stressed than the headline suggests.

And then I go back to the part of the game where I have at least some edge, which is trying to understand individual businesses, not the entire macro machine.

That’s always been the lesson for me. Headlines make for good content. But compounders make for good portfolios. And the two don’t always overlap.