Coupang (CPNG): Built for Long-Term Returns

Coupang is one of those businesses where the general perception of the stock and the actual machine underneath are not in sync.

Most people see a Korean e-commerce stock with a premium valuation and a small market going up against giants. They glance at it and call it expensive.

Under the surface, the business looks nothing like that.

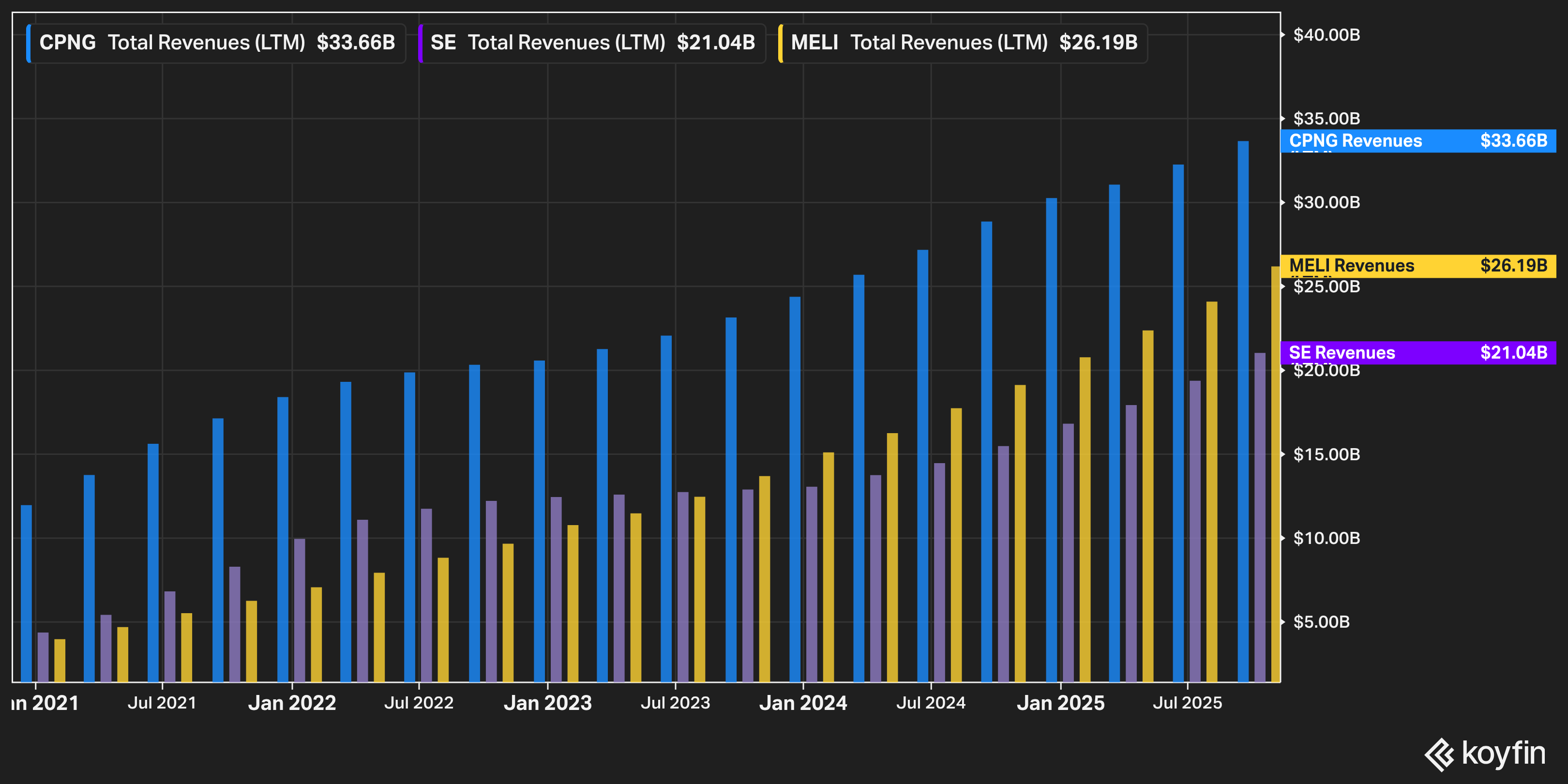

In the last 12 months, Coupang generated roughly $33 billion in revenue, growing about ~24%. For context, Sea Limited (SE) came in around $21 billion. MercadoLibre did about $26 billion. Both operate across sprawling regions with populations well above 600 million.

Coupang does more revenue than either of them while operating inside a country of 52 million people.

That fact alone should make any investor pause. You don’t normally see the smallest market producing the largest revenue base unless something structurally different is going on. The question is not why Coupang screens as expensive. The better question is what sort of engine produces that kind of revenue density, and what it might look like if management keeps under-earning on purpose for another decade.

I think the answer is that Coupang has quietly built one of the deepest local moats in global e-commerce, and the numbers look optically expensive precisely because the company is still teaching that moat how to make money.

I will walk through why I see it that way.

I use Koyfin every day to study long-term winners, compare financials, and track valuations. It’s the tool I used to pull most of the charts and numbers in this piece. If you spend real time analyzing companies, it’s worth trying.

Coughlin Capital has a partnership with Koyfin, so readers get 20% OFF any plan using this link.

Penetration Over Population

To understand Coupang, you have to start with the physical reality of South Korea.

This is a highly urban, highly connected country. Roughly 70% of Koreans live within ten minutes of a Coupang logistics center. The company claims that 99% plus of orders are delivered within 24 hours. They are not a website with some outsourced third-party last-mile layer bolted on. They are a logistics company that happens to wear an e-commerce front end.

Rocket Delivery is the core. It is the promise that if you tap “order” before you go to bed, whatever you ordered will probably be waiting at your door when you wake up. Rocket Fresh extends that to groceries. Coupang Eats pulls restaurants into the same network. Coupang Play sits in the background as a streaming perk that makes the subscription feel stickier. Coupang Pay is the payment glue.

Layered on top of all that is Rocket WOW, their version of Prime. The program has roughly 14 to 15 million members, covering around 60 to 65% of Korean households. For many Korean families, Coupang is the default infrastructure for buying things.

If you zoom out and look at it on a simple per-capita basis, the gap becomes almost absurd. Coupang generated $33.66 billion of revenue over the past twelve months. Spread across South Korea’s 52 million people, that’s roughly $650 per person per year flowing through one platform.

Sea Limited did $21.04 billion across a region of about 680 million people, which comes out closer to $30 per person.

MercadoLibre did $26.19 billion across roughly 650 million people in Latin America, or about $40 per person.

At this point it is worth adding one clarification so the comparison is not misunderstood. Historically, Coupang was almost entirely a first party retailer (1P).

Earlier in its life, estimates put Rocket Delivery items at around 90% of total GMV, which effectively meant the company was buying inventory, storing it in its own fulfillment centers, and recognizing the full ticket price as revenue when it sold. Over the past few years management has deliberately pushed the marketplace side of the business. Third party (3P) merchants have grown much faster, and in 2025, estimates have 3P sellers accounting for a narrow majority of GMV, with 1P a bit under half.

That mix shift matters for how the numbers look on the income statement. A company that still runs a lot of 1P retail will naturally report more revenue for the same underlying GMV than one that is mostly marketplace. Sea and MercadoLibre are structurally more marketplace heavy, so their reported revenue captures only the take rate, not the full value of goods moving across the platform.

But it does not erase the point. Even once you adjust for a higher 1P contribution, Coupang’s underlying GMV per household is still far above what you see elsewhere. Korea’s density, broadband penetration, and consumer habits let Coupang push deeper into daily life than peers can in less concentrated markets. The result is a business that looks outsized not because the market is large, but because the penetration is.

That level of entanglement is where the moat really begins.

Moat as Lived Reality

In most markets, e-commerce has splintered into a messy set of trade-offs. Some platforms are cheap but slow. Some are fast but unreliable. Some are great in metro areas and useless outside cities. Most rely heavily on third-party logistics partners. The customer learns very quickly that delivery promises are aspirational.

Coupang took a different path. From the early days, Bom Kim’s (CEO/Founder of CPNG) obsession was about controlling the entire experience. He built out a proprietary fulfillment network, hired his own couriers, and spent aggressively on automation. There are stories from early investors and board members about his intense focus on customer retention and reliability, which in practice looked more like an operational religion than a slogan.

That obsession shows up in mundane details… Drivers have keys or codes so they can leave packages safely. Refrigerated “Rocket Fresh” deliveries are handled inside a cold chain that actually keeps food cold, not lukewarm. The app is relentlessly tuned for ease, from one-tap reordering to tight integration with local search and reviews.

All of this rolls up into a business built on reinforcing loops. More volume per route means the cost of each delivery goes down. Lower costs make it easier to offer free or cheap shipping, which pulls more volume onto the platform. More volume per warehouse means you can justify higher automation spend, which lowers unit costs further and improves accuracy. Better service drives more customers into WOW, which raises recurring revenue and gives you more predictability as an operator.

At scale, this turns into something that feels simple from the outside and incredibly hard to copy from the inside.

A rival cannot just decide to do same-day delivery in a dense country and catch up in a year. They have to build warehouses, hire drivers, build sortation systems, tune routes, and do it all while bleeding cash and competing with an incumbent that already has the density.

When people say Coupang is the closest thing they have seen to Amazon’s DNA outside the United States, this is what they mean. It is a particular way of building infrastructure ahead of profits, and using price and convenience to compress the time it takes for behavior to change.

Under-Earning by Design

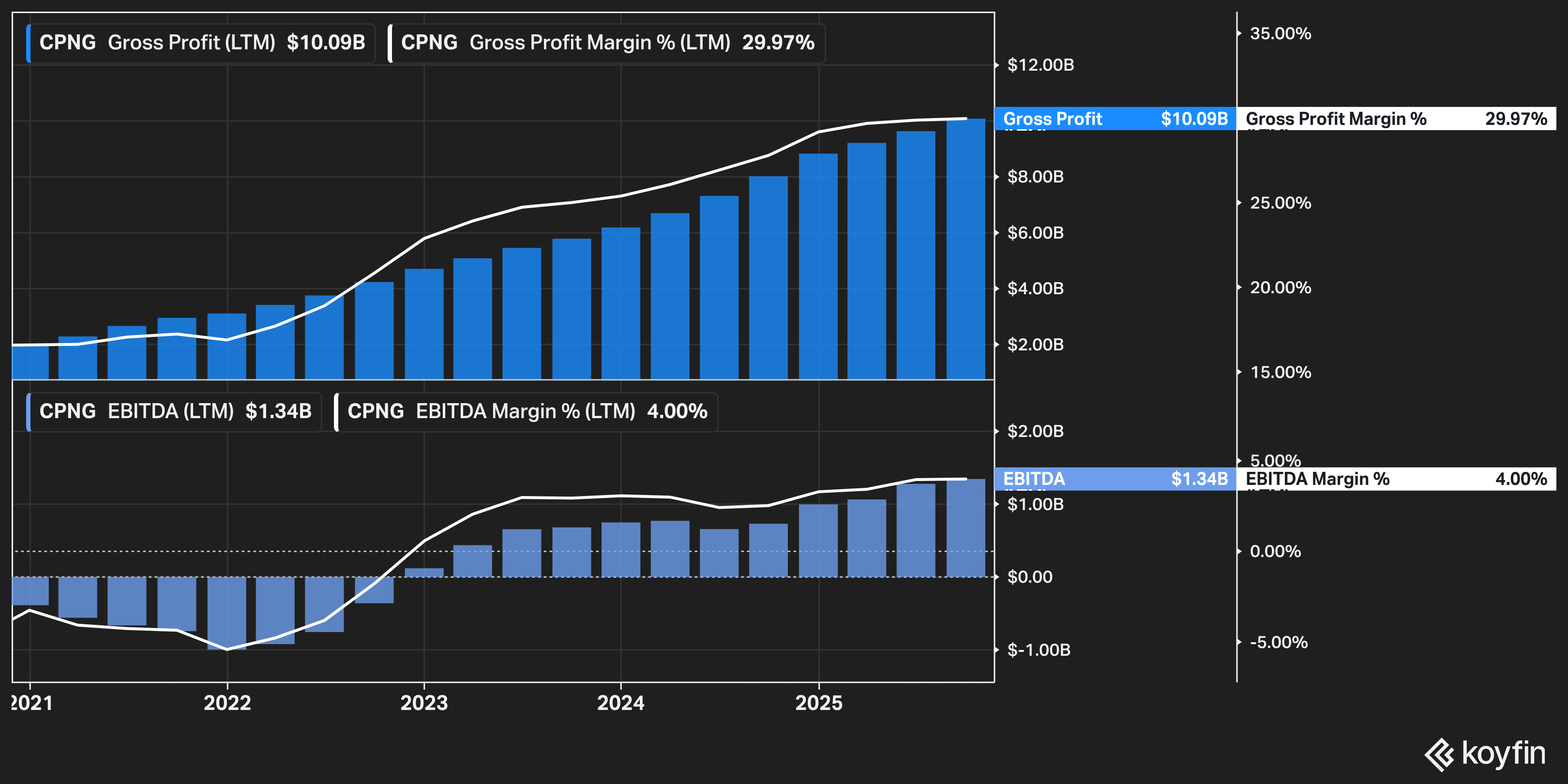

If you only look at the income statement, Coupang can look puzzling. $33 billion of revenue, but relatively modest bottom-line profits.

In Q3 2025, Coupang did about $9.3 billion of revenue, up ~18% year on year, with a gross margin just under ~30% and an adjusted EBITDA margin of roughly ~4.5%. For a business at this scale, that does not scream “bargain” if you are staring at a screener that only cares about this year’s EPS.

On the surface, that does not look like an obviously cheap stock. The temptation is to say margins are thin so the valuation must already be stretched.

I think that frame misses the point. If you break the business into pieces, you can see where the profits already exist and where they are deliberately being suppressed.

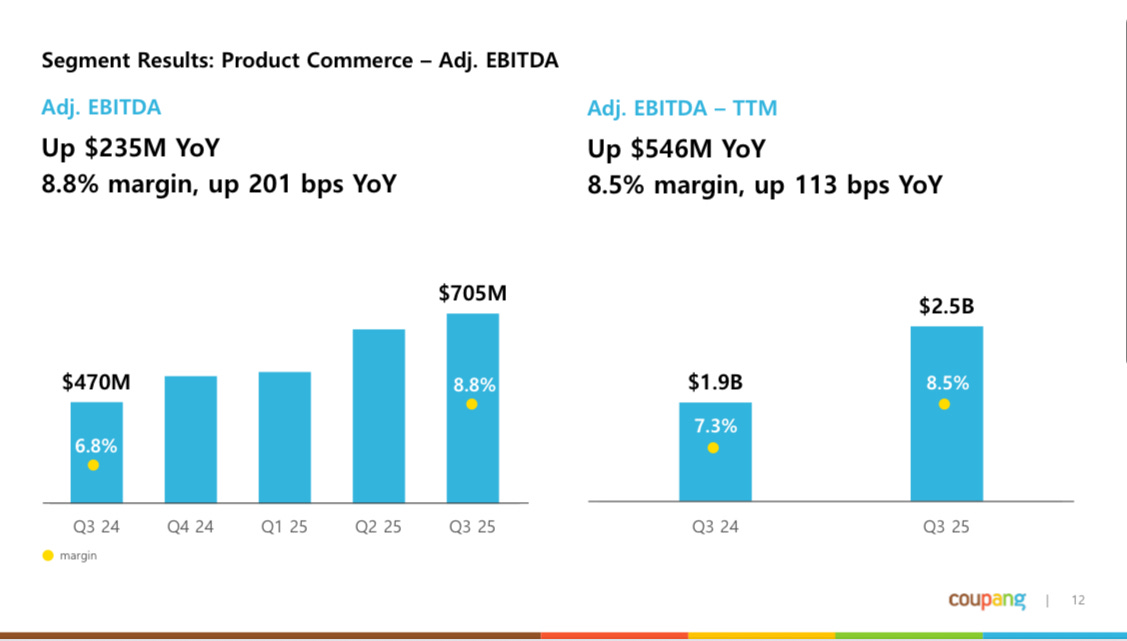

The core Product Commerce segment, which is essentially the domestic e-commerce and Rocket operations, is already earning very reasonable returns. In 2024 that segment generated $539 million of adjusted EBITDA with a margin of ~7.8%.

In the more recent 2025 quarterly results, Product Commerce margins have continued to grind higher into the high single digits. For a business that is still growing revenue in the mid-to-high teens and investing heavily in automation, those are attractive economics.

The drag sits inside what Coupang calls its developing offerings, which include Taiwan, Coupang Eats, Coupang Play, Fintech, and Farfetch.

On a full-year 2024 basis this bucket generated about $3.6 billion of net revenue, more than tripling year on year, and excluding Farfetch the growth was still roughly ~140%. By Q3 2025 it had grown to roughly $1.3 billion of net revenue in a single quarter, up ~32% year on year, with trailing twelve month revenue around $4 billion.

It is also losing money by design.

In 2024 developing offerings posted about $631 million of adjusted EBITDA losses, and management now expects 2025 losses to come in near the high end of a $900 to $950 million range as they lean into momentum in Taiwan and other early-stage bets.

Management is explicit about what they are doing. On the Q4 2024 call they guided to continued increases in tech and infrastructure spend to build a stronger foundation for future scalability, while also noting that OG&A as a percentage of revenue should decline over time.

They know they can dial profitability higher in the core. They are choosing not to, because they see a long runway in front of them, even inside Korea itself. As Bom Kim put it on the Q3 2025 call,

“Korea remains a remarkably durable growth opportunity with a largely untapped runway ahead.”

In other words, today’s drag is the price of turning these developing categories into tomorrow’s cash engines inside a home market that management still views as far from mature.

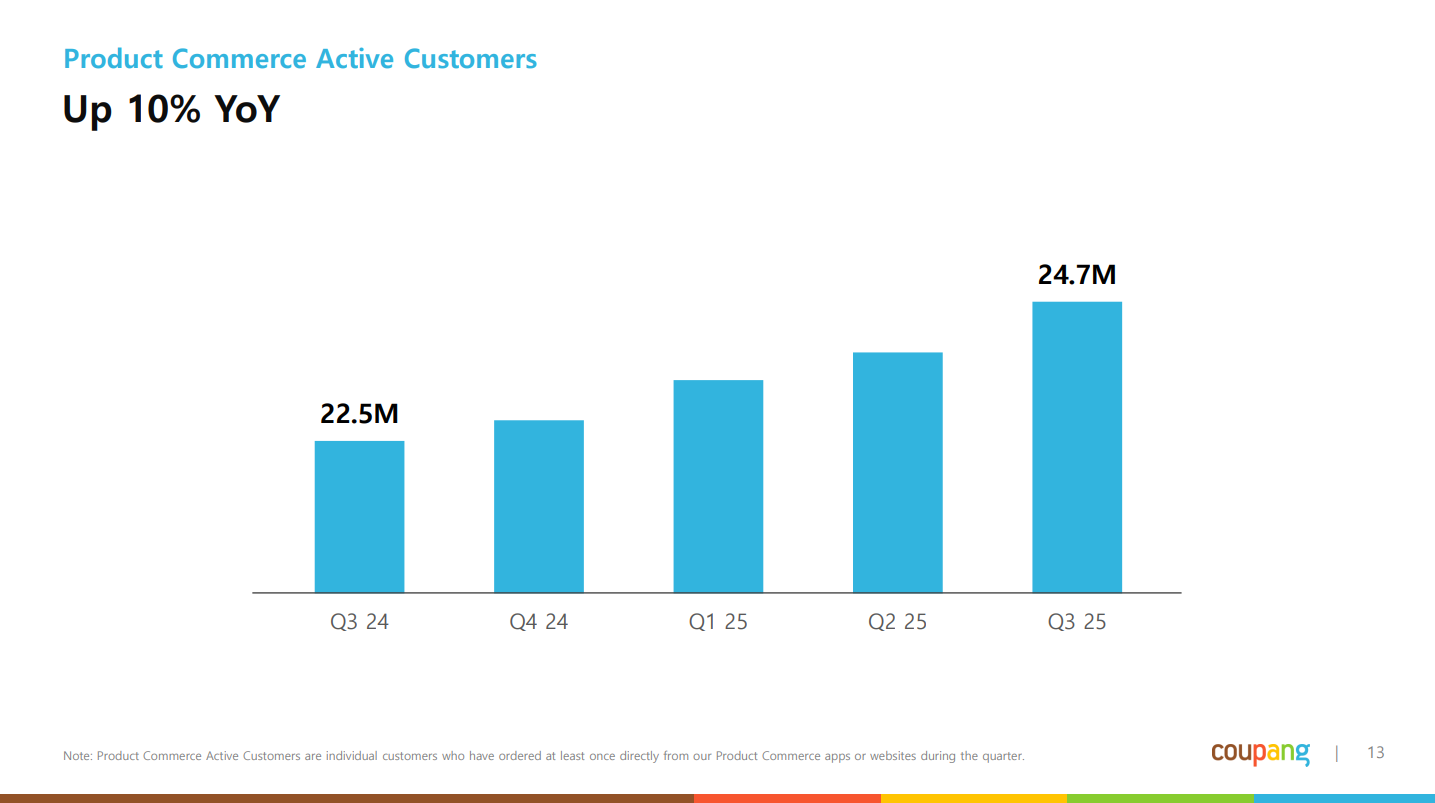

It is hard to doubt that conviction when you look at the underlying demand. Product Commerce active customers have climbed from about 22.5 million in Q3 2024 to 24.7 million in Q3 2025, roughly ~10% growth off an already massive base.

That steady rise in active buyers is what gives management confidence to keep leaning into Taiwan, Eats, Play, and Fintech even though those categories are still loss-making… It reflects a level of broad, habitual engagement that only develops when a service becomes infrastructure rather than a shopping site.

This is exactly the kind of under-earning that I like in a compounding story. It is similar in spirit, though not even close to identical in economics, to what I liked about Dropbox once it embraced being a mature cash machine and used that cash to shrink the share count instead of chasing vanity projects.

In Coupang’s case the choice is not “return cash versus nothing.” It is pressing the advantage now so that ten years from today, the cash machine is far bigger than the market expects.

In all of these cases, the accounting makes the business look less attractive than it really is if you only glance at current margins. That is what under-earning on purpose looks like.

The Paradox of Scale in a Tiny Market

So why exactly does Coupang generate more revenue than Sea and MercadoLibre, despite operating in a fraction of the population base?

Some of this is simply definitional. Sea and MercadoLibre mix e-commerce, fintech, and other services. Coupang also mixes things, but their mix is more tightly tied to physical commerce and logistics, and more of the economics are on their own P&L.

An asset-light marketplace that relies on third-party logistics and merchants will naturally show a different revenue and margin profile than a company that owns the trucks, the warehouses, and the drivers.

But the bigger answer is behavioral and structural.

Korea is extremely online. Broadband penetration is high. Mobile penetration is high. The population is dense. That allows Coupang to leverage its network harder than a comparable business spread across dozens of countries with weaker infrastructure.

The company has successfully turned WOW into a default utility. Two thirds of households paying a recurring subscription to one retailer is a different level of entanglement than what you see in most other regions. Once families have sunk into that ecosystem, each incremental category expansion, whether groceries or beauty or electronics, has a ready-made base of habitual buyers.

And the company has used price and convenience in a way that fits the Nick Sleep idea of sharing scale. When they improve efficiency, they pass much of it to customers in faster delivery and lower effective prices. That increases loyalty, which increases scale, which in turn lowers per-unit costs further. Over long stretches, the compounding from that flywheel can look surprisingly large.

Sea and MercadoLibre are both excellent businesses with their own defensible moats. But when you step back and ask which company has driven the deepest behavioral change in its home market, Coupang’s revenue density is a clear signal.

Reinvestment Logic and the Amazon Echo

If this were just a story about a dominant Korean retailer, the discussion would stop here. Big domestic moat, nice cash flows, maybe dividends, maybe steady earnings expansion.

Coupang is trying to do more than that. The under-earning strategy only makes sense if the reinvestment opportunities are real.

There are three reinvestment paths that matter most in my view.

1.) The first is deepening the Korean moat.

That means continuing to automate logistics. It means more AI in routing, forecasting, and inventory management. It means pulling more categories into Rocket, and making WOW such a no-brainer that churn stays negligible even if someone else offers free shipping for a while. Gross margins have been steadily expanding as the network matures. That gives them room to invest now and allow more of that efficiency to flow through to operating income later.

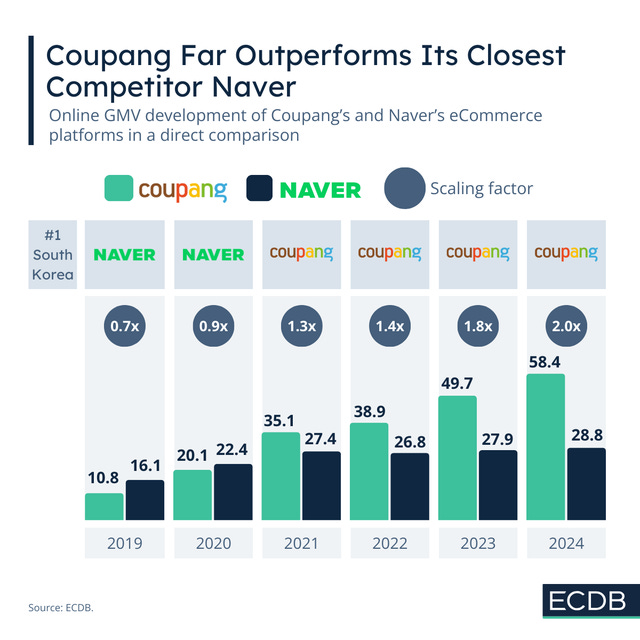

It helps to pause here and remember who they are actually competing against inside Korea. The company most people outside the country know is Coupang. The company most Koreans know is Naver. It is the default search engine, a massive portal, and for a long time its marketplace was the gravitational center of Korean e commerce.

Coupang didn’t grow up in a vacuum. It grew up ripping share away from entrenched marketplace players in Korea, in much the same way Amazon slowly pulled spending away from eBay and other early online incumbents in the US.

The chart below gives you a sense of how that rivalry has evolved. Naver is still an important player, but the gap in commerce GMV has widened sharply. Coupang has gone from trailing Naver to roughly doubling its online volume and it has done that while absorbing the heavy operational work, from warehouses to last mile, onto its own books. Naver’s marketplace still matters, but the flow of incremental consumer spend is tilting toward the model with the denser network and the faster service.

On the Q3 2025 call, management made clear that the Korean market is nowhere near saturated. As Bom Kim put it,

“Even in categories where we’ve made significant progress, we remain at the very beginning of what the customer experience can become. Our focus is on raising the bar every quarter, because the opportunity in Korea is still far larger than what we’ve captured so far.”

That mindset, seeing Korea not as a mature or tapped out market but as an expanding frontier, is the real reason they continue to reinvest so heavily at home even as the core business throws off more cash.

2.) The second is selective international expansion.

Taiwan is the obvious case. It shares some useful traits with Korea, including density and relatively high incomes. If Coupang can port even a fraction of the Korean playbook there, the long-run payoff is meaningful.

“Our Taiwan offering is growing faster and stronger than even the most optimistic forecast we set at the beginning of the year. After ending last year in Q4 with a quarter-over-quarter revenue growth of 23%, this quarter revenues surged 54% quarter-over-quarter, more than double the pace of revenue growth from just 2 quarters ago. Year-over-year revenue growth was triple digits in Q2, and we expect that to be even higher in Q3.

What’s most encouraging is that this growth is primarily fueled by repeat customers. While new customer additions did contribute to growth and a quarter-over-quarter increase of nearly 40% in active customers, the majority of the revenue growth and acceleration we saw this quarter stem from the continued strengthening of spend and retention across our existing customer cohorts. Our conviction in the long-term potential of Taiwan is only growing as we’re seeing a trajectory similar to what we saw in the early years of scaling our retail offering in Korea.”

The risk is that they spend heavily in markets where the structural advantages are weaker and discover that the domestic model does not travel as cleanly as hoped."

3.) The third is what I would call luxury and ecosystem optionality, where Farfetch is the most visible piece.

Coupang effectively rescued Farfetch from near-bankruptcy with a $500 million funding injection and is now trying to apply its operational discipline to a historically messy luxury marketplace. It is not core to the Korean moat. It is a separate bet that the same logistics, data instincts, and service orientation can turn an underperforming asset into something worthwhile.

This is where the Amazon echo is hard to ignore. Amazon spent years plowing money into AWS, Prime Video, and other adjacencies while retail margins looked thin. That was not an accident. It was a conscious decision to let the P&L under-earn in order to create much larger future cash engines.

I am not saying Coupang will replicate that outcome. The odds of any company recreating the AWS story are low.

I am saying that the management mindset feels familiar. The choice to accept mid single digit consolidated margins today, when core domestic commerce could probably support higher numbers, says they believe the opportunity set is still rich enough that hoarding earnings would be short-sighted.

Valuation in Context

I will not run a full DCF here. That is not how I like to think on paper.

Instead, I try to keep a simple mental picture in mind. You have a core Korean commerce business that can probably grow revenue in the low to mid teens for a while and push segment EBITDA margins into the low double digits as scale and automation keep doing their work. Around that core you have a set of developing offerings that currently pull consolidated margins down, but that can shift the whole P&L higher if even a couple of them grow into real profit pools over the next five to ten years.

If the group ends up somewhere in the $50 to $75 billion revenue range over the next five or so years, with consolidated operating margins in the high single digits or low teens, the earnings power looks very different from what shows up in today’s income statement. That is the basic shape of the bet.

The interesting part is how little you have to pay for that possibility when you line Coupang up against the obvious peers. A lot of the “Coupang is expensive” argument comes from looking at near term earnings or EBITDA multiples in isolation.

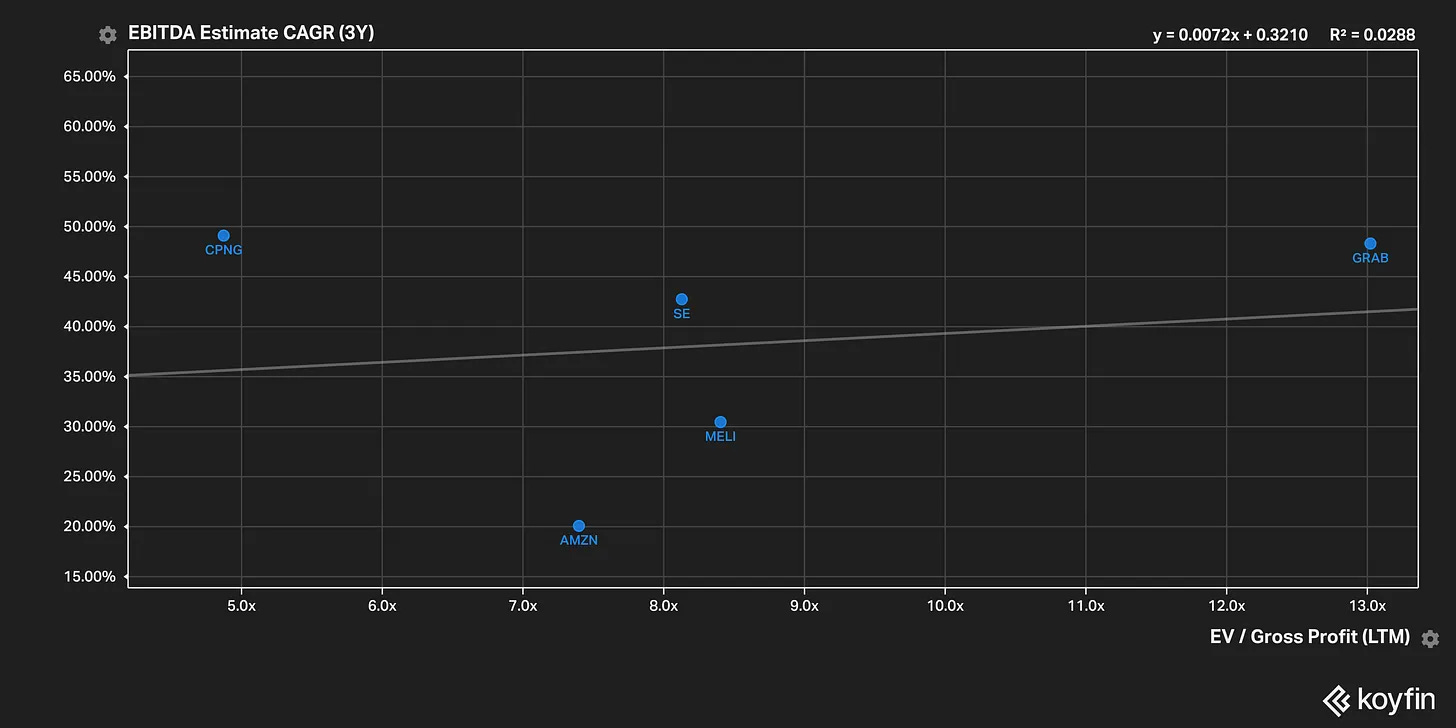

If you instead anchor on enterprise value to gross profit, which is a cleaner way to compare businesses that are still under-earning by design, Coupang actually sits at the bottom of the peer group. On a trailing basis it trades at a lower EV to gross profit than Sea, MercadoLibre, Amazon, or Grab, despite having already built a denser revenue base in a much smaller market.

The Koyfin scatterplots in this section try to make that point visually.

The first chart plots EV to gross profit on the x-axis and expected three year EBITDA growth on the y-axis. Most of the peer group lines up roughly where you would expect. The names that trade at richer multiples are the ones where consensus is baking in healthy but not explosive EBITDA growth. Coupang is the outlier. It sits at the low end of the valuation range on EV to gross profit, yet consensus expects its EBITDA to compound meaningfully faster than any of the large caps on the same chart.

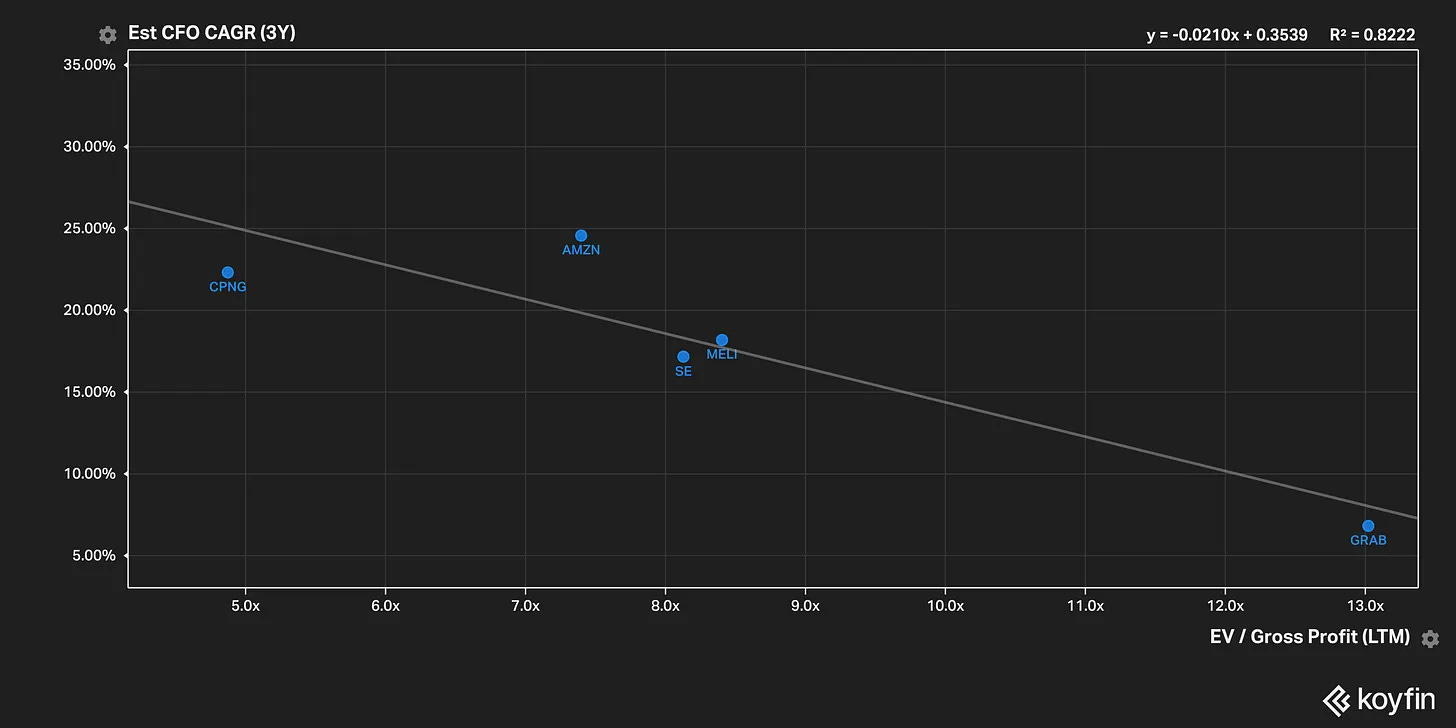

The second scatterplot runs the same exercise using estimated three year operating cash flow growth instead of EBITDA. The pattern is similar. Coupang again shows up as the cheapest name on an EV to gross profit basis while also posting the strongest expected growth in operating cash flow over the next few years. In other words, within this small universe of high quality, scaled commerce platforms, Coupang is the one name that combines a low structural valuation yardstick with the highest forward growth estimates.

To me that is what under-earning on purpose is supposed to look like. The market recognizes that Coupang is not a distressed asset, so you will not find it at a single digit headline P/E or EBIT mulitple. At the same time, it has not fully connected the dots between the current accounting, the segment mix, and the cash flow trajectory. If the core Korean engine keeps grinding margins higher while the developing businesses move from losses to breakeven and then profits, the multiple on today’s gross profit will quietly compress itself over time.

The flip side is that this is not a mature, sleepy cash generator trading at a single digit free cash flow multiple. Alibaba was in that bucket in 2024, when sentiment and macro fear pushed a real asset into value-stock territory. Dropbox still lives in that world today, where you can clip a healthy free cash flow yield from a stable base and let buybacks quietly do most of the work.

Coupang is not that kind of investment. It is still in buildout mode. The cash that could be sitting on the income statement is being recycled into logistics, automation, and the developing businesses that weigh on current margins. You have to be comfortable underwriting execution risk in Korea and reinvestment risk across the broader portfolio, because the whole point here is to own a business that is deliberately holding back earnings today in order to produce a very different earnings profile a few years from now.

That is what paying an owner’s multiple really means. You are buying the right to the future cash machine, not the optics of current profitability.

For me, the thesis is simple. I like businesses where the observable flywheel is powerful, the reinvestment decisions are rational, and the accounting makes the business look worse than it really is. That is what I think is happening at Coupang.

Owner’s Lens for the Next Decade

If I zoom out and imagine what Coupang looks like in ten years if this works, a few things stand out.

I see a Korean household that has grown up with Coupang as the default infrastructure for daily life. Kids in that household barely remember a time when you did not tap your phone and get groceries in the morning and electronics in the afternoon. That habit is extremely hard to dislodge.

I see a logistics network that is even more automated than it is today, with robots, AI-driven routing, and an efficiency level that makes it painful for any new entrant to match service without destroying their own P&L.

I see adjacencies, maybe not all of them, maturing into profit contributors rather than loss makers. Taiwan is one candidate. Some mix of digital content, food delivery, and fintech may carve out durable niches.

I see a business that is still comfortable under-earning in certain places to keep the flywheel spinning, but with far greater absolute earnings than today’s accounting suggests.

Most importantly, I see a company that has built something structurally hard to copy. You can write checks to fund an app. You cannot write a check to compress a decade of logistics learning and trust-building into a year.

That does not mean Coupang is risk free or inevitable. What it does mean is that when the smallest market is generating the largest revenue among its peer set, and when the mechanics behind that fact are well understood, the debate becomes less about what the stock earns next year and more about whether the moat and reinvestment philosophy deserve time.

For a long-term, business-owner style investor, that is the real question. And for Coupang, I find myself leaning toward yes.

Disclaimer: Nothing here is investment advice. Please do your own research and make decisions that fit your own situation.