Fear + Volatility = Opportunity

Zooming out on the China thesis and China AI

If you’re reading this and you own Chinese tech names, you probably feel like an idiot right now. I own China tech names and I sometimes feel like an idiot too…

That’s what drawdowns do. They make you question everything. You start second-guessing yourself, and you start wondering if the guy on X/Twitter calling you a bagholder might actually have a point.

But I’ve been through enough of these to know that stock prices don’t tell you much about a business over short periods of time. They tell you about sentiment. And right now the sentiment and the fundamentals are living on different planets.

The broader thesis on China/China Tech hasn’t changed. I actually think it’s the strongest it’s ever been. Which I realize sounds like exactly what a bagholder would say…

But instead of getting emotional about it I’m going to do my best to zoom out and focus on what actually matters in terms of returns.

The tape looks awful. The underlying buildout doesn’t. That disconnect is the whole reason I’m still here.

Fear + Volatility = Opportunity

It’s been a rough stretch. And not just for China names, but especially for China names.

Iran and the Strait of Hormuz have global risk appetite in the gutter. VAT tax rumors on internet companies sent everyone scrambling for the exits back in February. The Supreme Court struck down Trump’s IEEPA tariffs and threw the whole trade framework into question.

And mainland investors have been yanking billions out of Hong Kong-listed tech because they’re tired of watching these companies spend aggressively on AI without seeing it in the earnings yet.

Oh, and Alibaba’s Qwen AI team had some leadership departures. Three senior guys this year. Cue the hot takes about Alibaba abandoning open source and the whole AI strategy falling apart.

You stack all of that on top of each other and yeah, I get why people are running for the exits.

If you’re a sentiment-driven trader, this is a nightmare. Go sell. I’m not mad at you.

But the long-term tailwinds haven’t changed. There are 1.4 billion people moving online, and a government actively pushing domestic consumption while going all-in on AI. Nothing has actually gotten worse.

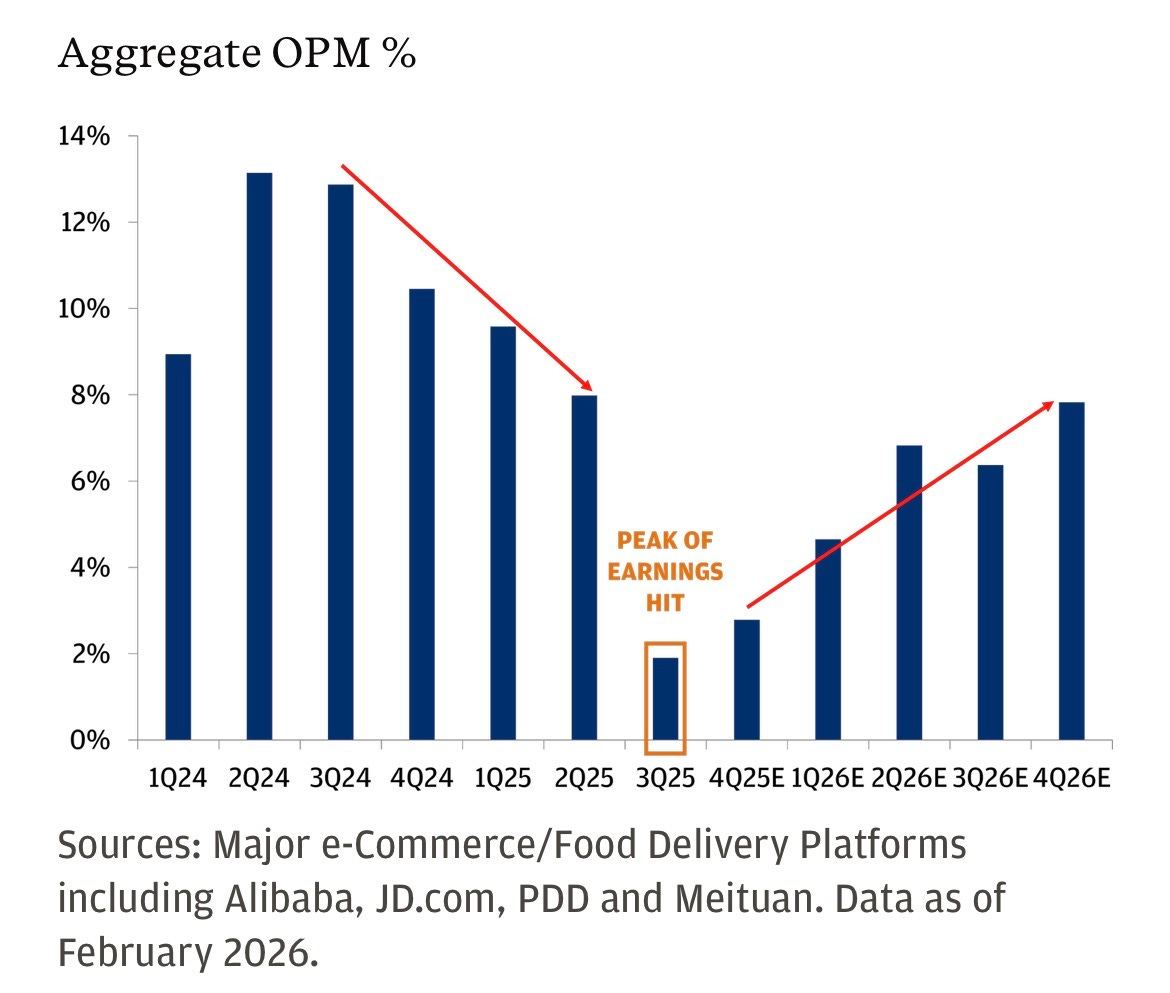

A big reason HSTECH in particular has been under so much pressure is the margin compression from the e-commerce price war. And that’s fair. It’s expensive and the near-term margins are getting destroyed.

But I think people are seriously underestimating what a company like Alibaba will actually earn in a normalized environment once the subsidy wars wind down. And regulators are already stepping in to cool things off, which basically locks in the gains for the companies that already won share.

More importantly, the story is shifting. Alibaba is becoming a cloud and AI-first company. That’s where the investment is going and that’s where the growth is. But they also have something none of the pure-play cloud or AI companies have, which is a massive existing user base, a mountain of commerce data, and an ecosystem that’s probably better positioned for agentic AI and AI-powered shopping than anyone else in the world.

When AI agents start actually buying things for people, who do you think has the infrastructure for that?

Keep reading with a 7-day free trial

Subscribe to Coughlin Cap to keep reading this post and get 7 days of free access to the full post archives.