How to Identify Long-Term Compounders

Understanding the qualities that support real, durable compounding.

I use Koyfin every day to study long-term winners, compare financials, and track valuations. The platform makes it easy to pull clean data without feeling like you are fighting the interface.

Coughlin Capital has a partnership with Koyfin, so readers can get 20% OFF any plan (Use this link to claim it). If you spend real time analyzing companies, it is worth trying.

A Simple Guide to Spotting Long-Term Winners

Most investors spend their time trying to figure out what happens next quarter. I’d rather find businesses I can ignore for ten years and still feel good about owning.

That sounds lazy, but it’s actually harder than trading the news cycle. Finding companies that can compound value over decades requires looking past the noise and understanding what creates durable, accumulating advantages. After studying dozens of long-term winners and sitting through plenty of losers, I’ve noticed the same patterns keep appearing.

Not every great compounder has all of these traits, but the ones worth holding through multiple cycles usually have at least three working strongly in their favor. These aren’t revolutionary insights, they’re obvious once you see them.

The hard part is having the patience to wait for them to compound.

1. The Business Creates More Value Than It Captures

Nick Sleep articulated this idea better than anyone. The best long-duration businesses consistently create surplus for their customers, which then circles back in the form of loyalty, scale, and pricing power that does not depend on marketing budgets or trend cycles.

Costco is the purest example. For decades, the company could have extracted far more margin from its membership model and never did. Prices stayed low. Consumers felt the bargain. That trust hardened into behavior, and behavior is what protects a business when the economy swings around.

The same dynamic drove Amazon’s early years. Bezos consistently chose to pass on cost savings to customers rather than expand margins, creating such overwhelming value that customers changed their shopping behavior permanently. The consumer surplus was so large that when Amazon finally did start raising prices and introducing fees, customers barely noticed. They were still getting a bargain relative to the value received.

Contrast this with businesses that try to capture all the value they create. Cable companies extracted maximum value until streaming destroyed them. Taxi medallion holders charged monopoly rents until ridesharing made them obsolete. When you leave no consumer surplus, you’re essentially posting a “Please Disrupt Me” sign.

The businesses that compound for decades understand this math intuitively. They could charge more, but don’t. That gap between value created and value captured isn’t inefficiency—it’s the foundation of the compounding.

2. Scale Economics That Get Shared, Not Hoarded

Most businesses talk about scale advantages. Few actually share them. The difference between those two approaches shows up clearly over ten-year periods.

When a business gets bigger and keeps all the benefits, it might boost margins for a while. But it also creates an umbrella for competitors and resentment from customers. When a business systematically shares scale benefits, it creates a virtuous cycle that’s nearly impossible to stop.

The sharing approach is what built Walmart into a multi-decade compounder. Every efficiency gain from scale got passed to customers through lower prices, which drove more traffic, which increased scale, which lowered costs further.

Sam Walton understood that maintaining modest margins while growing the pie was better than maximizing margins on a fixed-size pie. The long-term result of that mindset is one of the most impressive compounding stories in public markets.

Nebraska Furniture Mart, one of Berkshire’s longest-held subsidiaries, runs the same playbook. Mrs. B’s philosophy was simple: sell cheap and tell the truth. By sharing scale benefits with customers through rock-bottom prices, she built such volume that competitors couldn’t match her costs even at higher margins. The business has quietly compounded value for Berkshire for four decades.

The inverse approach (hoarding scale benefits) might boost margins temporarily but plants the seeds of disruption. When incumbent retailers kept all their scale advantages as profits rather than lower prices, they created the umbrella that let Amazon grow. When traditional auto dealers captured scale through higher margins rather than better prices, they opened the door for Tesla’s direct model and Carvana’s digital approach.

Scale economics shared is a choice that looks like leaving money on the table in year one but proves brilliant by year ten. The businesses that make this choice tend to compound the longest.

3. Capital Allocation as a Core Competency

Over a decade, how a company deploys its cash matters more than almost any other factor. The best long-term compounders treat capital allocation not as a side activity but as central to the business.

Danaher is a great example of this. Their operating system is well known, but the quiet discipline behind their acquisitions is what produced the multi-decade compounding story. They stayed inside their circle of competence, avoided heroic bets, and recycled cash with remarkable consistency.

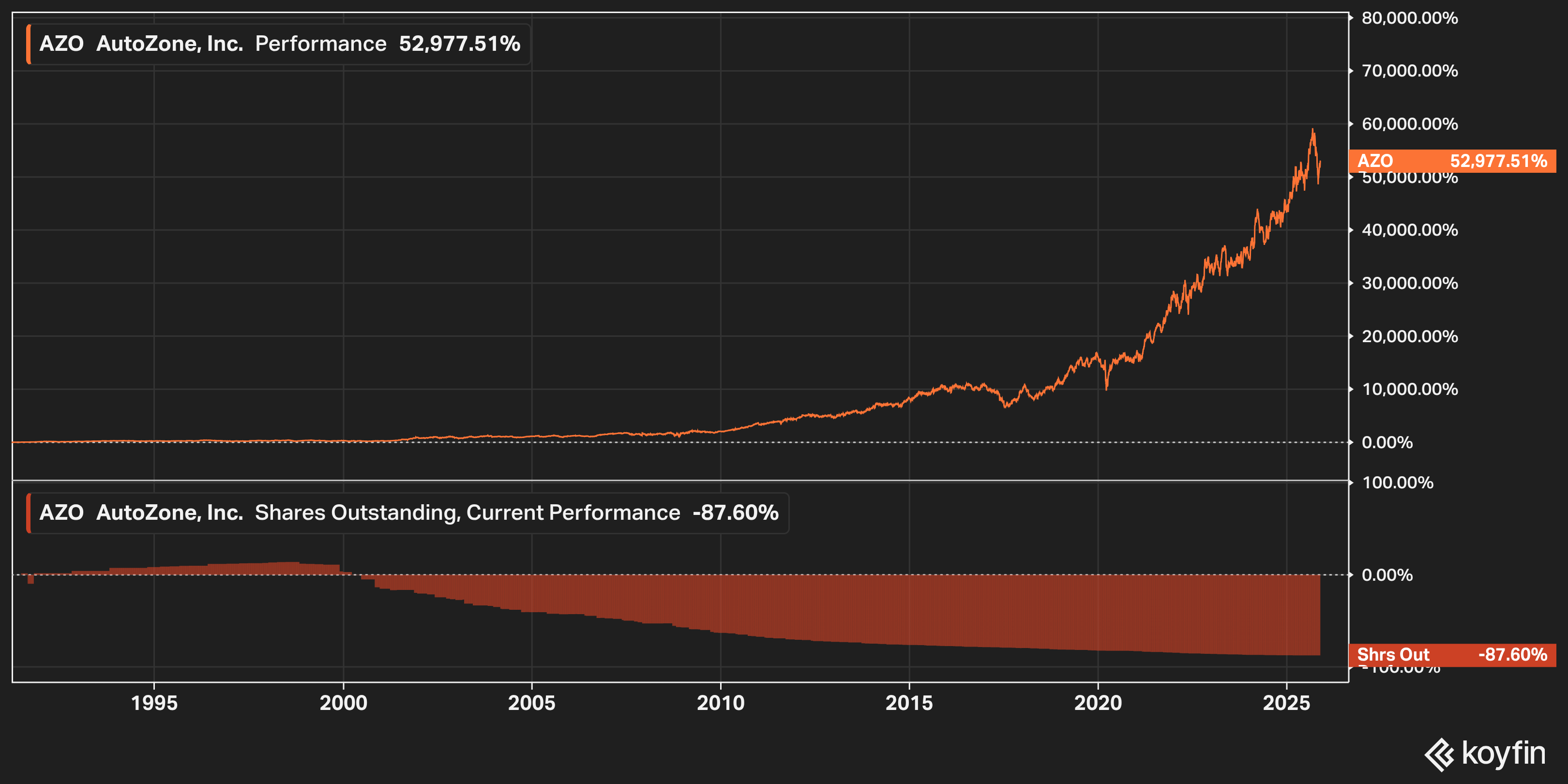

AutoZone proved that you do not need a glamorous strategy to create enormous value. A simple business model paired with steady buybacks and rational store growth produced one of the best long-term returns in American retail.

Constellation Software built its entire identity around capital allocation. By acquiring sticky, mission-critical vertical software businesses and reinvesting the cash flows, they created a flywheel that has worked across multiple cycles and geographies.

The companies that fail this test are usually easy to spot. They chase growth through expensive acquisitions, they buy back stock at peak valuations to offset dilution, or they sit on cash while opportunities pass by. Over a quarter or two, this might not matter. Over a decade, it’s the difference between compounding and stagnation.

4. Unit Economics That Endure When Conditions Change

Many businesses look great during expansion, but long-term compounders tend to have unit economics that stay resilient when the world pressures them.

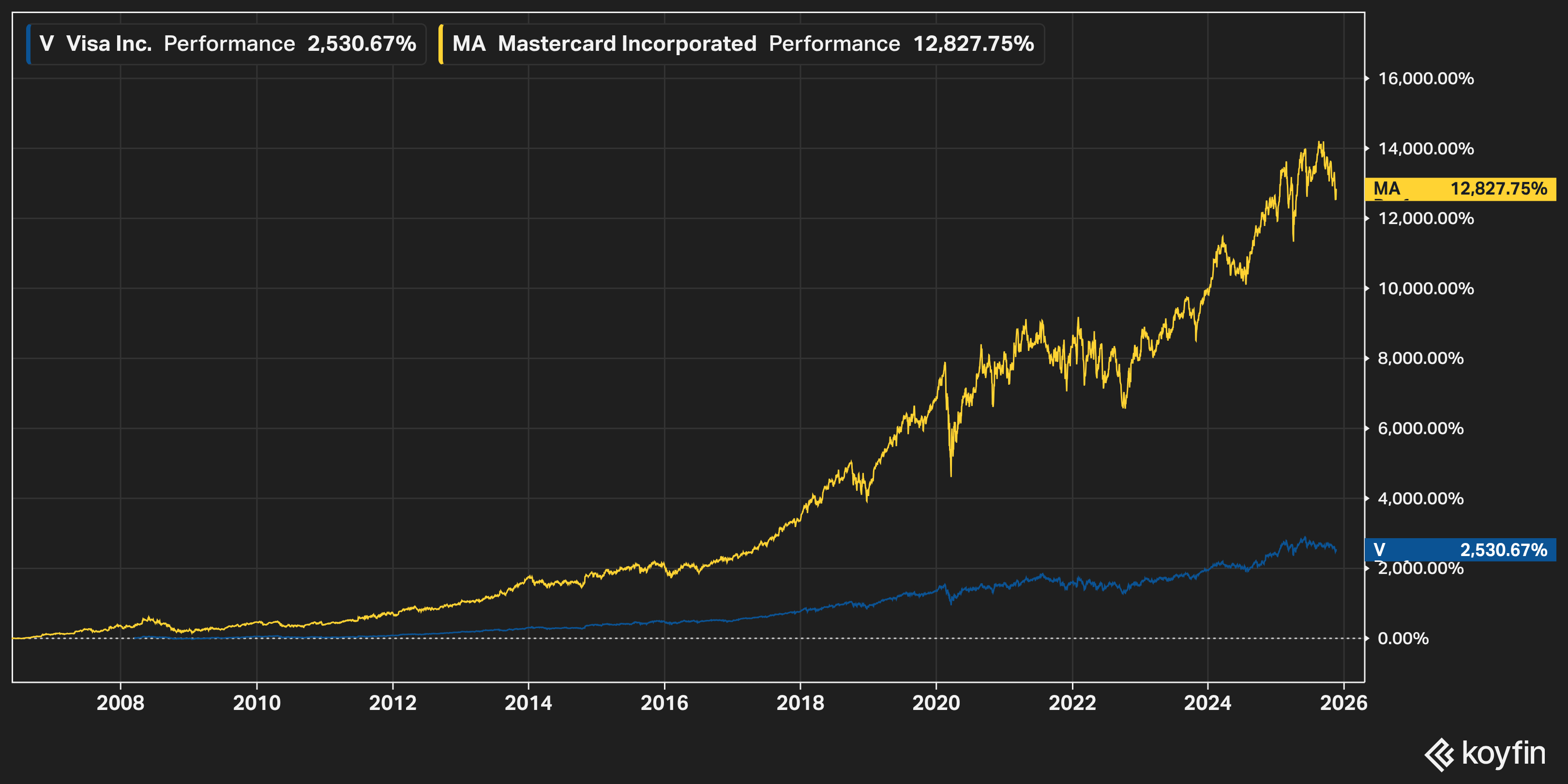

Visa and Mastercard have perhaps the most resilient unit economics ever created. Near-zero marginal cost to process an additional transaction, network effects that strengthen with scale, and a toll-booth position that’s regulatory-protected but not regulated.

Those economics survived the dot-com crash, the financial crisis, COVID, and countless fintech “disruptors.” The unit economics are so strong that even terrible capital allocation couldn’t kill the compounding.

ASML and TSMC show a different flavor of durability. Their economics are tied to extreme complexity and irreplaceability. Even in difficult cycles, the market structure protects returns.

The opposite examples usually reveal themselves through fragile assumptions. The meal kit companies, the moviepass model, most food delivery services—they all had unit economics that looked acceptable at small scale but broke when they tried to grow. If you need to believe in massive scale benefits that haven’t appeared after billions of investment, you’re not looking at sustainable unit economics.

5. A Starting Valuation That Isn’t Priced for Perfection

Even the best business becomes a mediocre investment if you pay too much. The greatest long-term compounders were usually available at reasonable prices at some point, often when they were misunderstood or temporarily out of favor.

Microsoft in 2013 and 2014 is the cleanest example. The stock traded at a modest earnings multiple because the PC narrative dominated the conversation. The underlying economics were still powerful, and Azure was quietly building momentum. The multiple created room for compounding.

Home Depot in 2011 looked dull and cyclical. The market assumed the housing crisis had permanently damaged the model. In reality, the unit economics never changed, and the business resumed its steady long-term trajectory.

Today’s equivalents might include certain European consumer brands or Chinese internet giants. Hated sectors where decent businesses trade like they’re going extinct. Not all will compound, but at these valuations, you don’t need heroics. You just need survival and modest improvement.

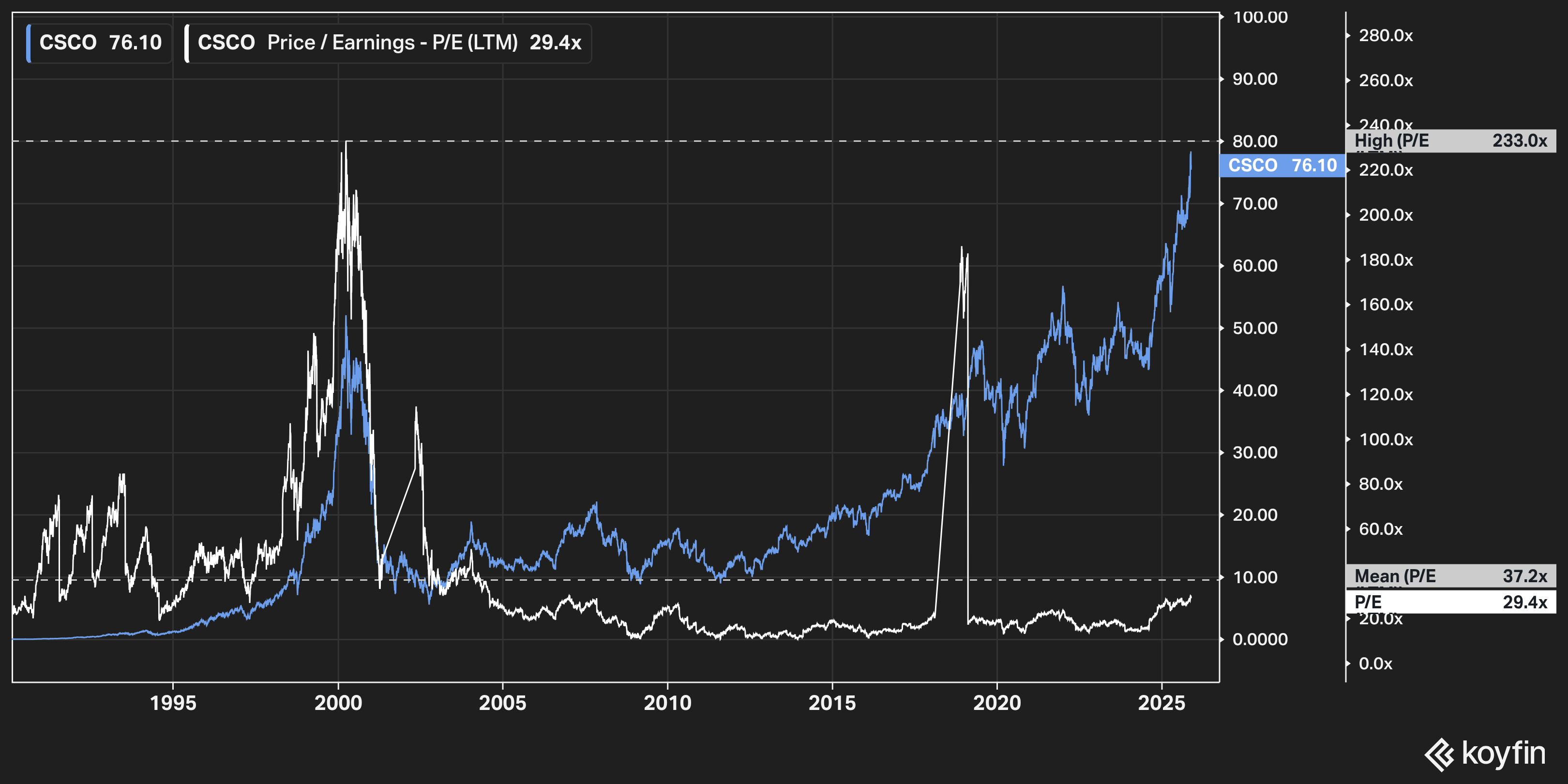

The flip side is obvious but worth stating: paying something like ~50x earnings for even a great business usually leads to disappointment. Cisco in 2000 was a phenomenal company that traded at ~200x earnings.

The company created value for years, but shareholders had to wait a generation to see it reflected in the share price. That is the difference between owning a good business and paying too much for it.

Time Is the Common Thread

These five traits are not boxes to check. They are characteristics that show up repeatedly in the companies that manage to grow value year after year. You will not find every trait in every business, but a handful working together often signals a foundation you can trust through good and bad periods.

What they share is the need for time. Customer surplus becomes behavior only after consistency. Shared scale advantages strengthen in increments that are invisible until they suddenly are not. Capital allocation reveals its skill only across long stretches. Strong unit economics do not prove anything during easy years. Valuation becomes destiny only after the business earns its way forward.

Once you see this dynamic, the rhythm becomes familiar.

These traits reward time. They reward investors who stay focused on the signals that matter.

Customer value evolves slowly.

Scale takes patience.

Capital allocation needs cycles.

Unit economics require stress.

Valuation influences the arc, not the daily movement.

The edge is not foresight. It is patience.

Most investors never give these traits the room they need, which is why the opportunity repeats for those who do.

I fully agree with this view point. The problem is that exceptional businesses are so rare, that you sometimes need to fill the portfolio with mediocre businesses that are valued at stupid prices which are set for a rerating in the medium term (1-2 years). It takes balls of steel to have a portfolio of 3 stocks like Nick Sleep. For now I have 1 stock which I know very well which meets all of these criteria, perhaps a second one, and a bunch of them which meet several points, but I am not 100% sure that they can meet all points. The economies of scale shared is one where it is difficult to know unless you are a customer of their products, and I also tend to gravitate to businesses that are niche and without competition, so what can you compare their value proposition to? Just my thoughts.

Thank you, that's helpful framework for assessing potential compounders. I tried to apply it to SEA Limited, my biggest position by far:

1. Customer value: yes. Shopee is positioned as the cheapest, focuses on high volume of orders with a low average order value.

2. Economies of scale shared: yes. Delivery cost keeps coming down, they pass the savings to the consumer.

3. Capital allocation: probably yes. Examples: raised capital near the top of the 2021 mania, switched focus from growth to profitability when the tide turned against them, stepped back quickly when expansion into new regions didn't work (e.g. Europe).

4. Resilient unit economics: yes for the gaming division, but hard to tell for ecommerce and fintech (early stage, haven't faced a major crisis yet).

5. Valuation: probably reasonable if one believes in the secular growth of South East Asian economies, SEA's moat in ecom and a large runway for the lending business.