Some Thoughts on China

Just a short post today. I wanted to get some thoughts out on China.

We’re only a few days into 2026, so I’m not going to read too much into the early price action. But after watching Chinese tech bleed out through November and December, it’s at least worth noting that the first few sessions of the year have been strong.

Whether that holds or not, I have no idea.

If you're new here, I'm a private investor who writes about the companies I'm researching and the positions I'm building. China has been a big focus.

If that's the kind of thing you're interested in, my Start Here post explains what I'm doing with this newsletter. And if you find it useful, consider subscribing.

What I do know is that the Q4 weakness never changed my view. The selloff looked like tax-loss selling and year-end noise to me. The kind of stuff that shakes out the late money but doesn’t tell you anything about where things are headed.

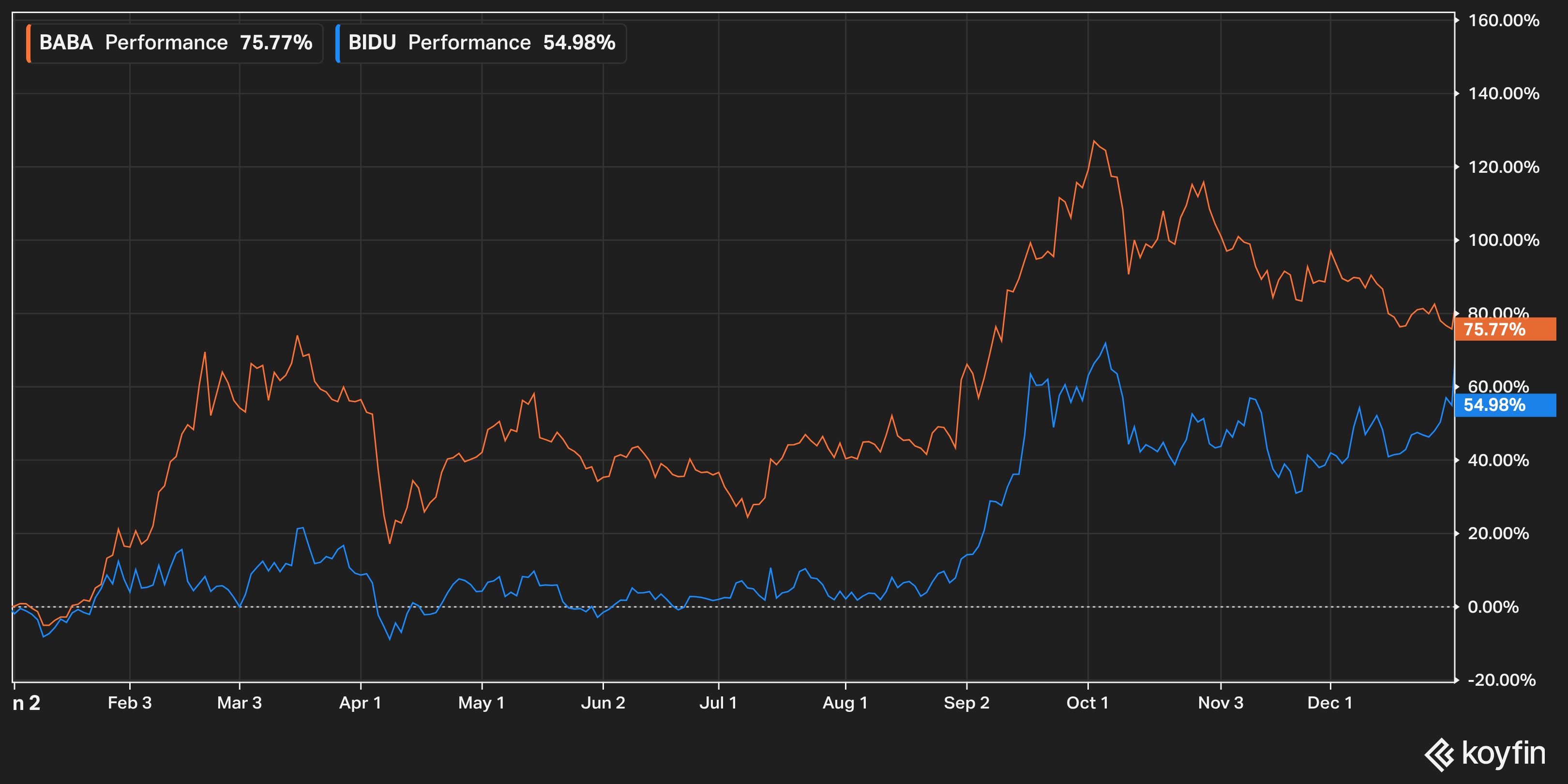

If you’ve been following along, you know China has been a big part of my portfolio. Alibaba is one of my largest positions. I’ve written about it plenty and taken heat for it at times. Baidu has been on my radar almost as long. So while my broader view applies to Chinese equities as a whole, I’m going to focus on these two since they’re the names I know best and where I’ve actually put money to work.

Both Alibaba and Baidu had monster years in 2025. BABA finished up around ~75%. BIDU around ~50%. After years of being left for dead, suddenly everyone realized China was investable again.

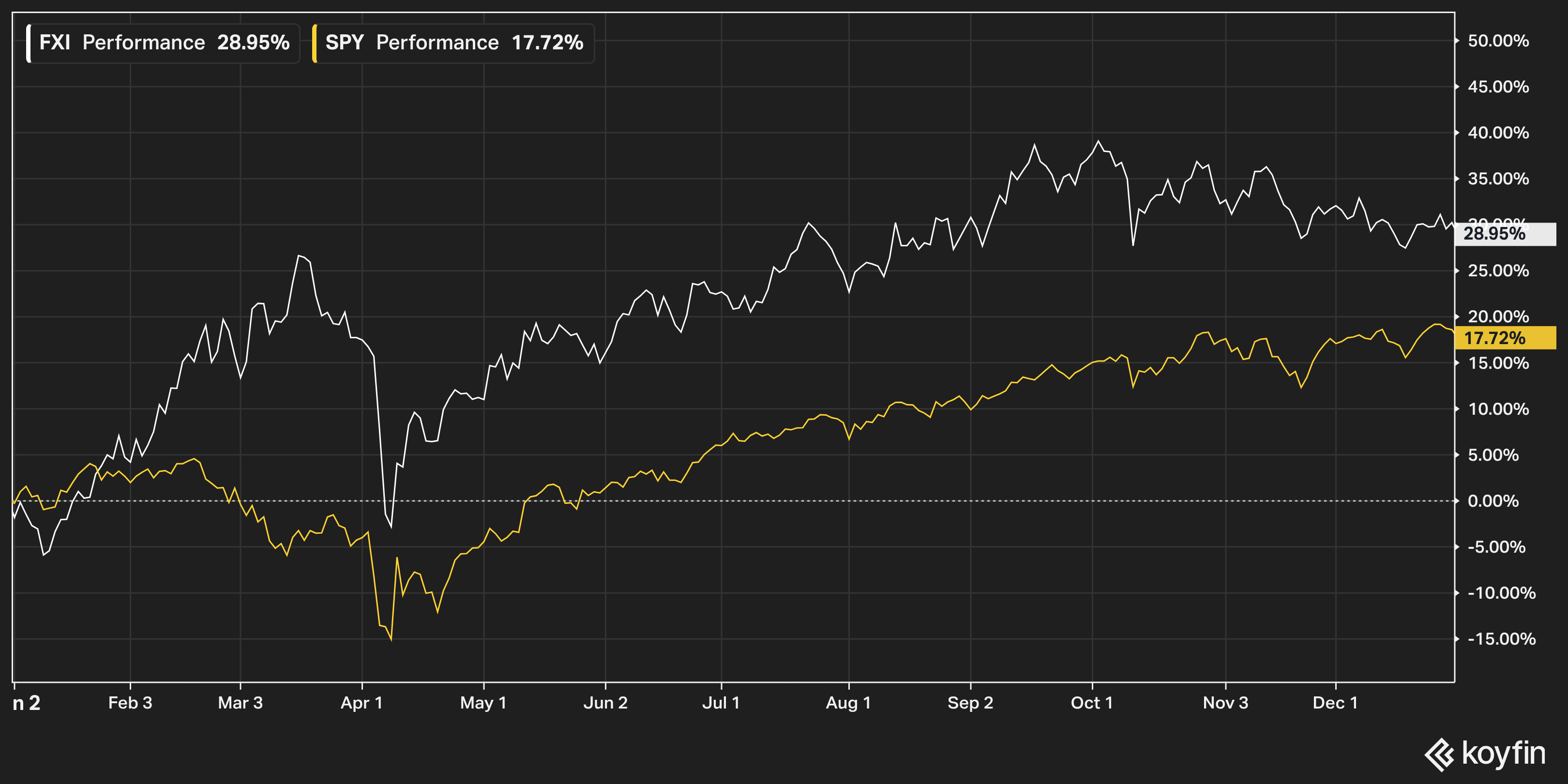

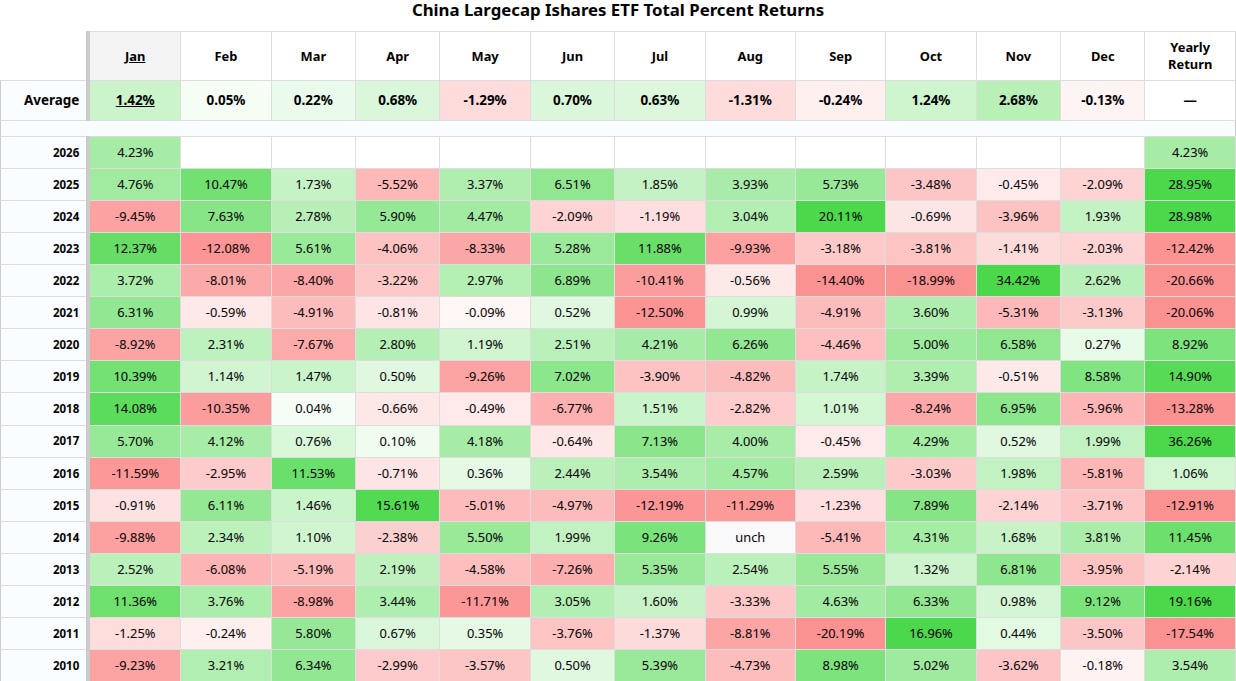

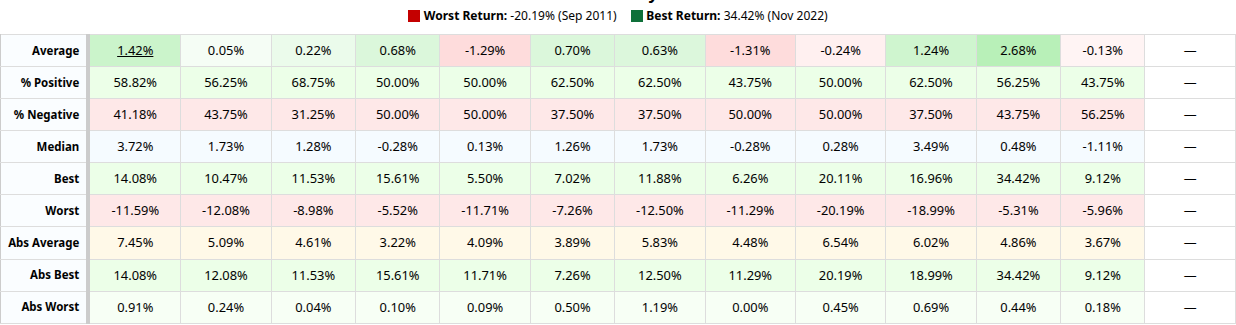

Zoom out a bit and 2025 looks even more notable. FXI (China large-cap ETF) returned around ~29% for the year. SPY did about ~18%. Chinese large caps beat the US market by double digits. The last time that happened was 2009.

Sixteen years. Most investors I know haven't even processed this yet. They saw the China headlines, maybe noticed BABA was up a lot. But the idea that China actually beat the US market last year? I don't think that's sunk in for most people.

But big moves attract late money. And I'd guess a lot of the people who bought in September or October don't even realize China outperformed the US for the year. They just know they're sitting on losses after the Q4 rollover. Those are exactly the people who sell into year-end to harvest tax losses.

So the late money got shaken out. The fundamentals didn’t change. Alibaba’s cloud business is still growing north of 30% with AI revenue compounding at triple digits. They’re still buying back stock. The valuation is still reasonable by almost any measure. The only thing that changed was the price went down for a couple months.

We’ve also seen Baidu get a bit more interesting. The Kunlunxin chip spinoff news dropped on the first trading day of 2026 and the stock jumped over 10%.

Jefferies thinks the unit could be worth $16 to $23 billion and Baidu owns 59% of it. That’s $9 to $13 billion in attributable value against a market cap that’s now around $50 billion. And the core business (outside of search) is performing well. AI cloud revenue is growing north of 20%. Apollo Go doing a quarter million robotaxi rides a week. New partnerships with Uber and Lyft to bring the tech to the UK. It’s not exactly the “dying company” the valuation implies…

I know the pushback. What about geopolitics? What about tariffs? What about all the reasons China has been “uninvestable” for the past few years?

Honestly, I think the US-China relationship is actually the best it’s been in years. The tariff situation has calmed down dramatically from the worst-case scenarios. We went from 145% at the peak to a 10% reciprocal rate after the Trump-Xi meeting in October, extended through late 2026. Yes, there’s still stacking with older duties that keeps effective rates higher on certain goods, but the trajectory is toward de-escalation, not escalation. Both sides want to make deals.

I genuinely believe this dynamic continues to improve. I know that’s not the consensus view. But the market spent years over-discounting China on geopolitical fears, and part of what we’re seeing now is that discount narrowing.

Could I be wrong? Obviously. But I’m not going to pretend I see risks that I don’t actually see. My read is that geopolitics is a tailwind at this point, not a headwind.

One more thing worth mentioning. We’re heading into the Lunar New Year window, January 29th this year. There’s actually decent academic research showing Chinese stocks tend to do well in this period. Investors get optimistic, bonus money gets deployed, the government avoids dropping bad news during the holiday. I’m not going to overweight a seasonal pattern, but it doesn’t hurt to have that tailwind either.

I’ve been saying for a while now that we’re in a bull market for Chinese equities. Not a trade. Not a bounce. A multi-year re-rating of an asset class that got way too cheap for way too long. The Q4 pullback didn’t change that view. If anything it reinforced it.

And I’ve said it before and I’ll say it again… If you’re an investor sitting with zero exposure to China right now, I think that’s a mistake. Not because I have some magic insight or because I’m pounding the table for you to go all-in. But because the risk-reward has shifted and the market hasn’t fully caught up yet.

You’ve got the second largest economy in the world, home to some of the best tech companies on the planet, trading at a fraction of what comparable US businesses cost. The narrative is finally turning. The money is starting to flow back. And most portfolios I see are still sitting at zero.

I’m not saying you need to size it like I have. But having nothing? In this environment? That feels like a bet in itself, and I’m not sure it’s the right one.

I think we’re still early. And I’m positioned accordingly.

Disclaimer: I am not a registered investment advisor. This newsletter is for informational purposes only. I hold positions in companies I write about, and those positions may change without notice. Do your own research.

Fully agree. I think Chinese equities are in consolidation/accumulation phase, and might have another strong leg up if the macro picture remains favorable.

Do you have any thoughts on Miniso?