Snapchat (SNAP): A Case Study in Value Destruction

A response to everyone calling this a buy

I’m not sure why, but at least once a year, my timeline fills up with optimism around Snapchat.

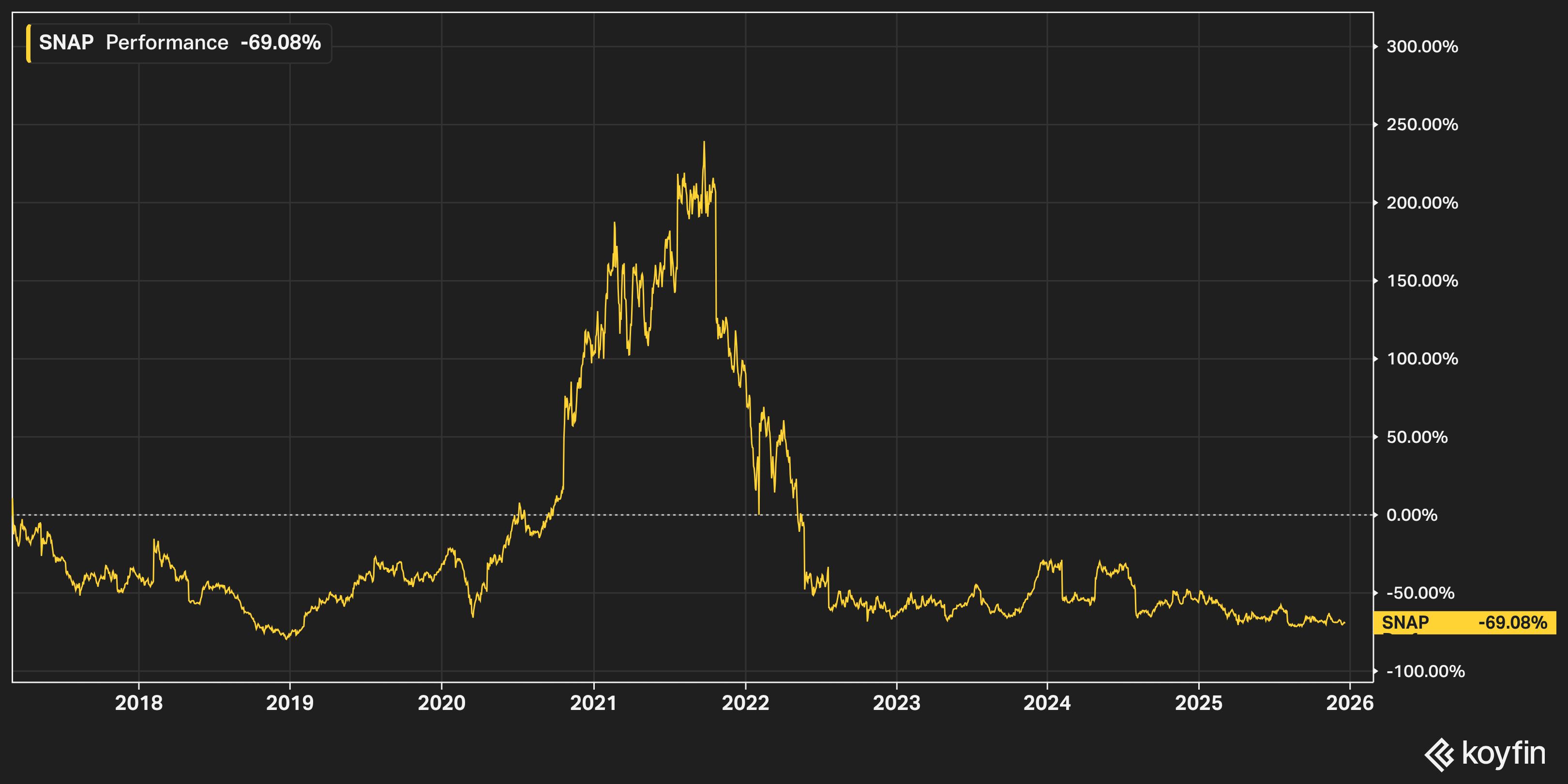

Over the past couple weeks, I’ve watched it build again—same pitches, same “this time is different” energy, same excitement for a stock down 90% from its highs and 70% below its IPO price…

I’ve seen this cycle play out for a few years now. Stock pops, someone writes a thread about how the market is finally waking up, people pile in, and then it quietly bleeds back down while everyone pretends they sold at the top.

Like a guy who keeps going back to his ex, convinced she’s changed. Rinse and repeat.

Look, I get why it looks attractive on the surface. Social media is a fantastic business when done right. Meta prints money. TikTok is eating the world. Snapchat has around 450 million daily users and your kids probably use it more than they talk to you. Surely there’s value somewhere in there…

Unfortunately, there isn’t. Or at least, there isn’t any for you.

The People Running This Thing

As with most shitcos, the problems start with the people running it…

Evan Spiegel, the CEO, received a stock award worth roughly $637 million tied to completing the IPO in 2017. Not for hitting targets. Not for profitability. Not for building something sustainable. Just for getting the company public.

He already owned around 24% of the company. The board handed him another chunk as a thank you for going public. I genuinely laughed when I first read this.

Most founders are already aligned with shareholders because they own a massive stake. Spiegel was apparently not aligned enough, so they gave him more. As a reward. For the privilege of letting you buy shares.

And those shares you can buy? No voting rights.

Snap went public with a three-class share structure where the Class A shares sold to the public carry zero votes. Spiegel and co-founder Bobby Murphy hold all the Class C shares, giving them control over the vast majority of voting power despite owning a smaller fraction of the economic interest.

You’re along for the ride whether you like it or not. You’re buying a movie ticket to a film they’re directing, producing, and starring in. Your opinion on the plot doesn’t matter.

This was all done intentionally… When the company went public, it was the first major U.S. IPO in decades to offer shares with absolutely no voting rights. The message was clear from day one: we want your money, not your input.

So what has Spiegel done with that control?

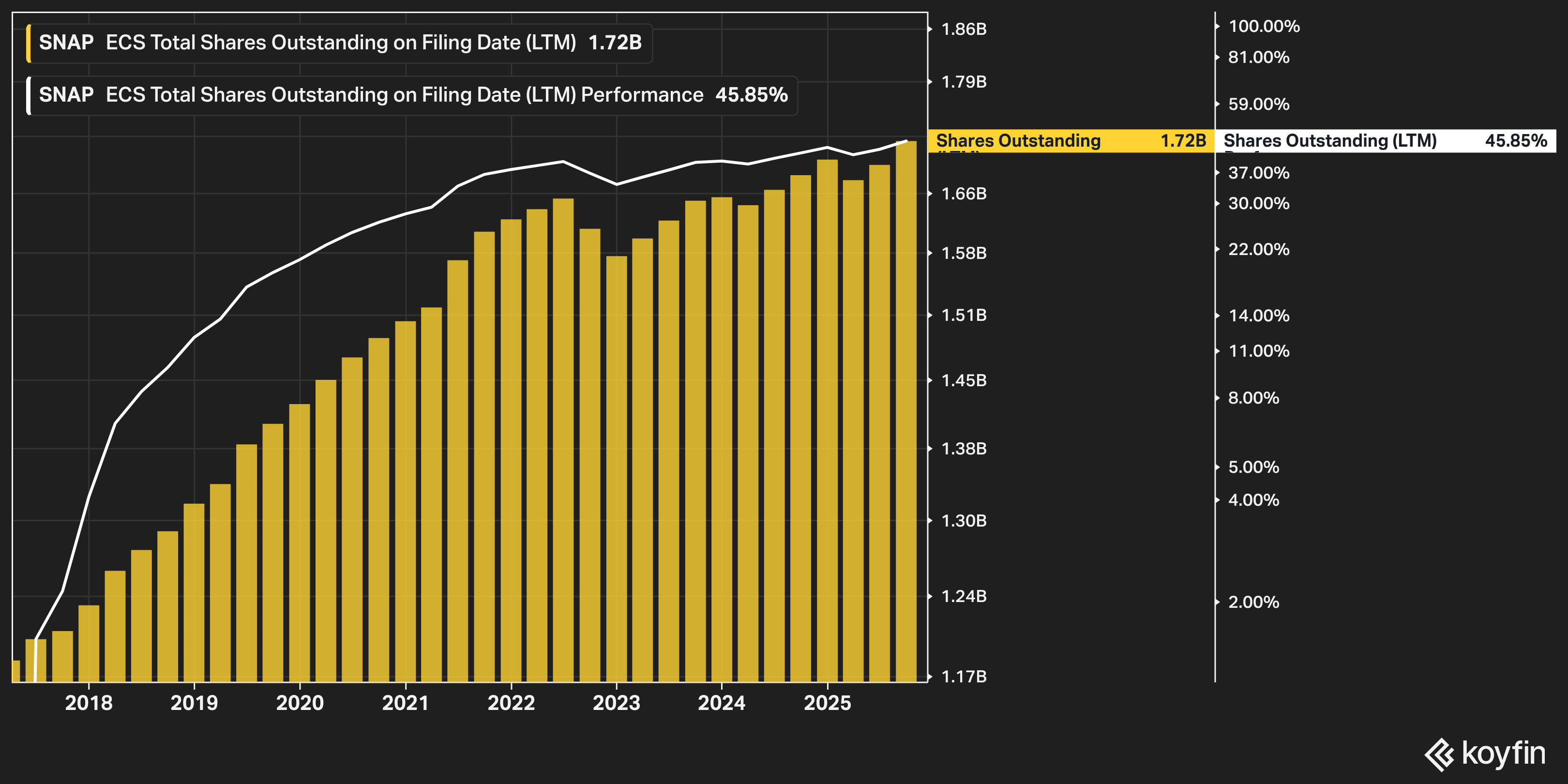

Snap has been public for eight years. In that time, the share count has grown from about 1.16 billion to roughly 1.7 billion. That’s about ~45% dilution. If you bought at the IPO, you now own meaningfully less of the company than you thought you did.

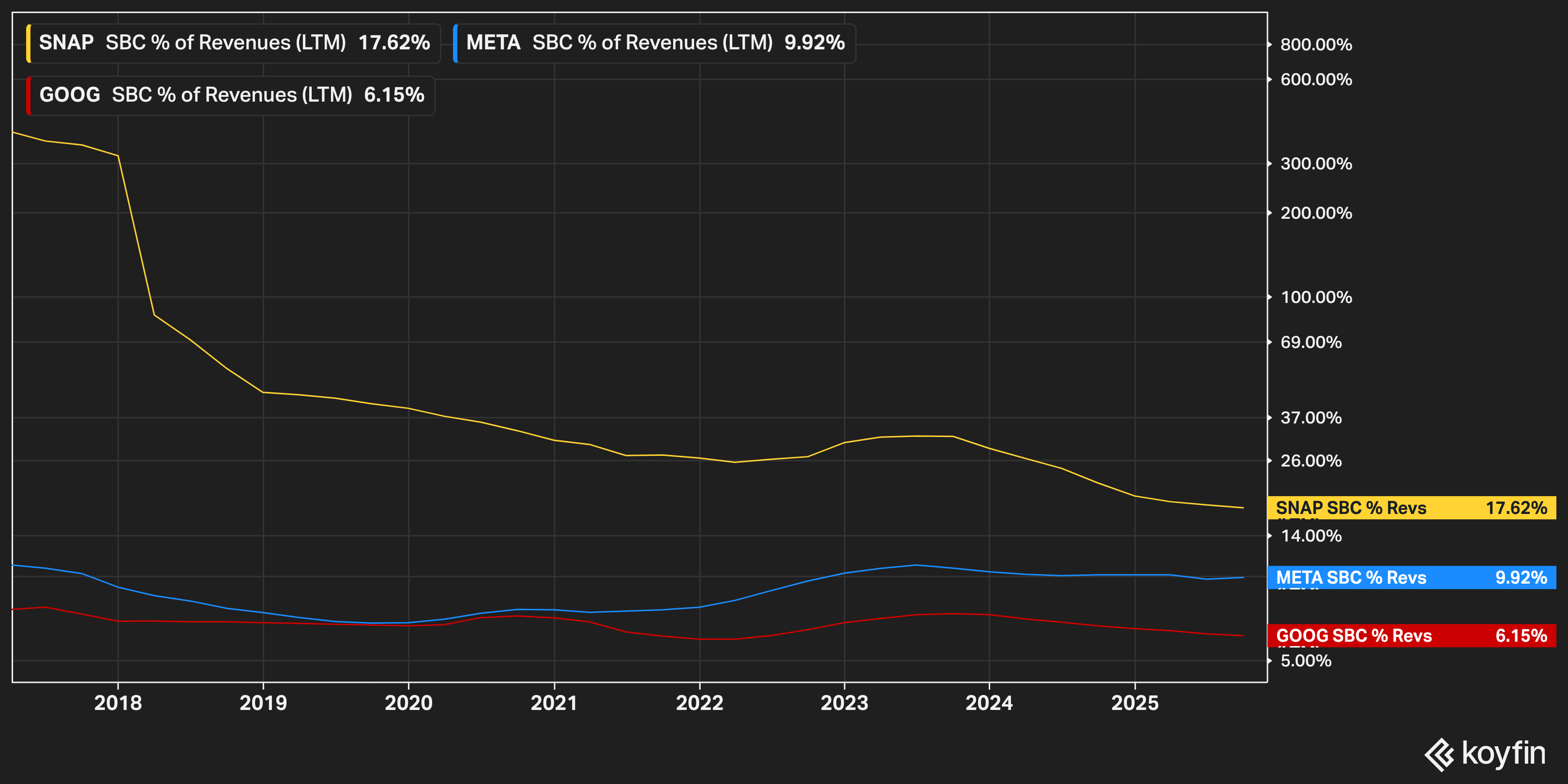

Where did all those shares go? Employees. Management. Stock-based compensation that runs somewhere around ~20% of revenue in recent years. Not operating expenses or EBITDA. Revenue.

They’re handing out a massive portion of the top line to employees every year in the form of equity. For context, Meta’s SBC runs in the single digits as a percentage of revenue. Google is similar. Snap is on a completely different planet.

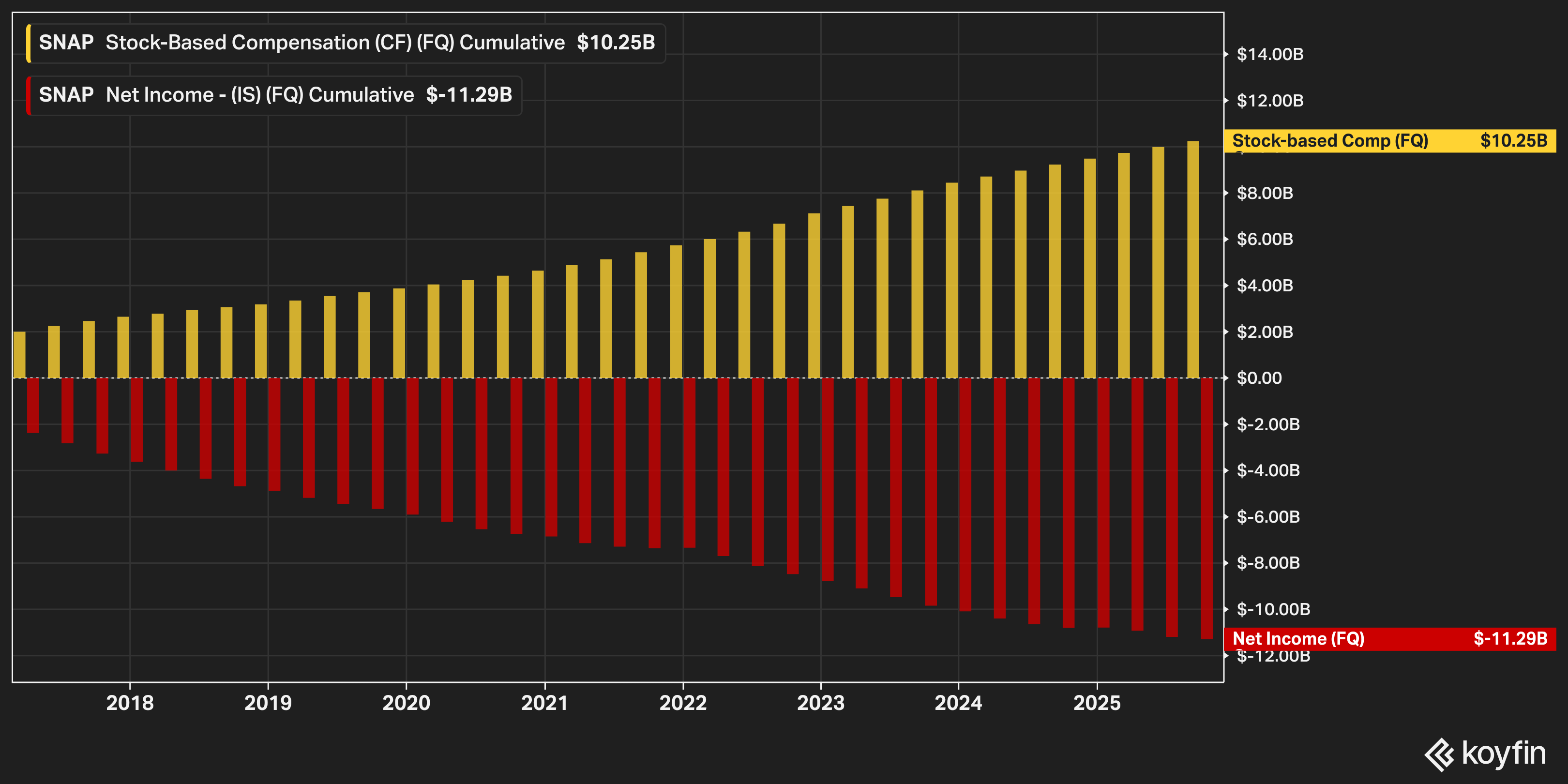

And here’s what really gets me. Snap has lost money every single year since going public.

Cumulative net losses are in the billions. They’ve burned cash in most years. The company did layoffs in 2022 and again in 2024, cutting around 10% of the workforce each time, and they still can’t turn a consistent profit.

But somehow, management keeps getting paid like they built the next Google.

The bulls will tell you that profitability is improving. And technically, that’s true. Snap has been flirting with breakeven on an adjusted basis. But adjusted metrics at Snap exclude stock-based compensation. When you’re giving away 20%+ of revenue in equity every year, excluding that expense makes things look way better than they actually are. GAAP earnings are what matter, and GAAP earnings are still negative.

At some point you have to accept that management is showing you exactly who they are. Eight years of this. Why would year nine be different?

The Business Problem

Even if management were perfect stewards of capital, Snap would still have a structural problem: they’re a distant fourth in a market where scale matters enormously.

Digital advertising is a game of data and targeting. The more users you have, the more data you collect, the better you can target ads, the more advertisers pay. Meta has nearly 4 billion monthly users across its family of apps. Google has search intent data on basically everyone with an internet connection. TikTok has the attention of an entire generation.

Snap has ~475M daily actives. Respectable. But Snap’s ARPU tells you everything about their competitive position. In North America, Snap does about $9 per user per quarter (call it mid-to-high $30s per year if you annualize it). Meta’s user economics are materially higher—even on a global basis Meta is doing roughly $14–15 per user per quarter, and North America is higher than that. These are completely different businesses from a monetization standpoint.

Why the gap? Meta has data from across the internet thanks to their tracking infrastructure. Snap’s data is largely confined to what happens inside the app. Meta has been iterating on advertising products for two decades. Snap is still figuring it out. And when brands allocate digital budgets, Meta and Google get the first call.

Snap is left fighting for whatever is left over.

You also have TikTok, which came out of nowhere and basically ate Snap’s lunch on short-form video. Instagram copied Stories and Reels directly from Snapchat’s playbook. Snap keeps innovating on the product side, credit where it’s due, but they’re fighting for attention against companies with far more resources and far better economics.

Meta can afford to lose money on new bets because the core business prints cash. Snap doesn’t have that luxury. Every dollar they spend trying to keep up is another dollar that comes out of a business that’s still struggling to break even.

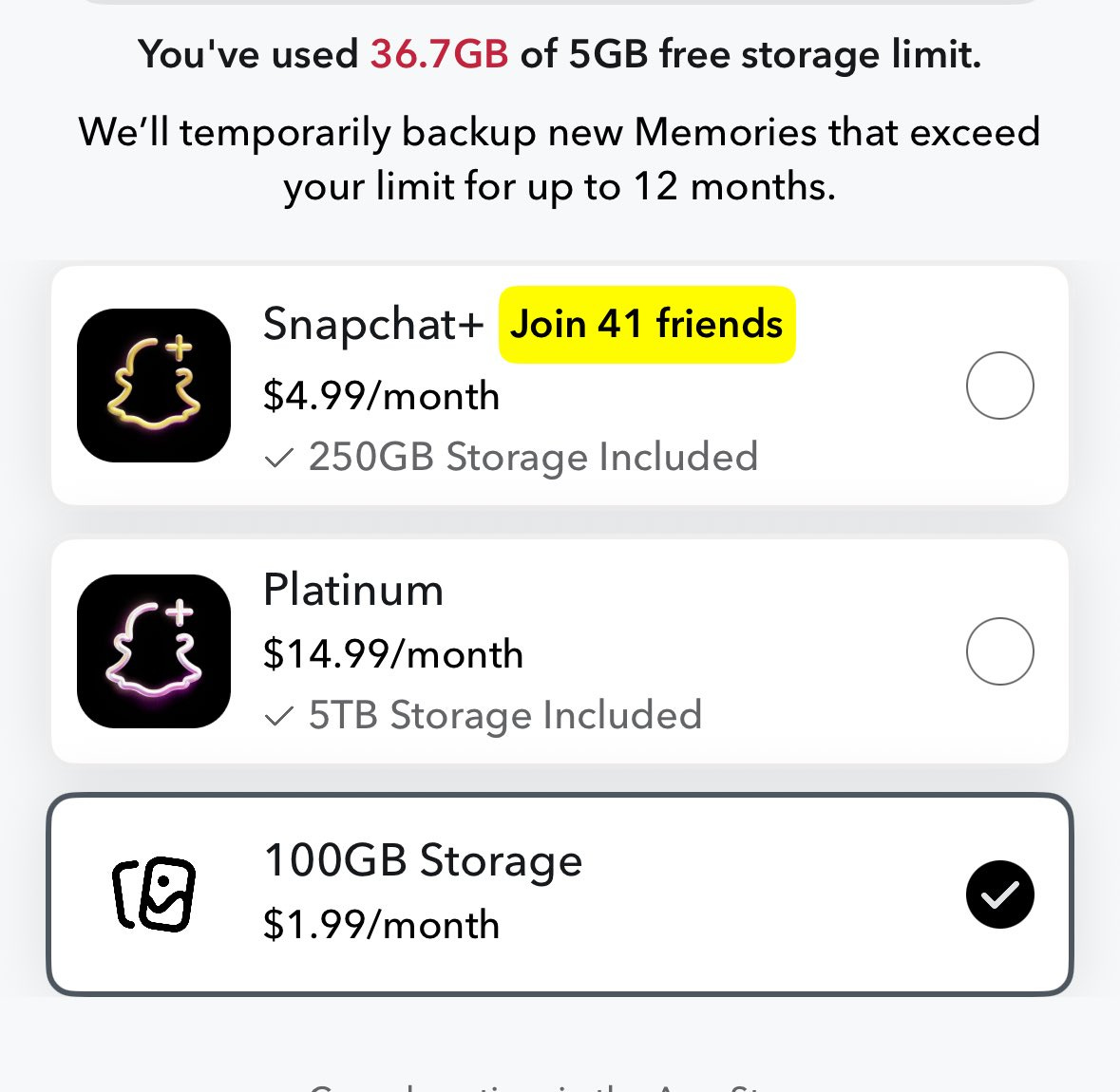

The bulls point to Snapchat+ as a diversification play. Something like 12-14 million subscribers paying around $4 per month is real money, probably in the $500-600 million range annually. And three months ago, they added another lever: Memories Storage Plans. If your photos and videos exceed 5GB, you now pay a monthly fee to keep them backed up. Pricing runs from $1.99/month for 100GB up to $14.99/month for 5TB.

This one actually has some logic to it. It’s a “paying for peace of mind” product—you’re not really buying storage, you’re buying the guarantee that your memories from 2013 won’t disappear. That’s an emotional decision, not a rational one, and emotional decisions convert.

There’s also a 12-month “temporary” backup for memories over the limit, a word chosen deliberately to light a fire under users. And since Snap already stores these files, the incremental cost is basically just billing and support. Almost pure margin.

The math bulls throw around: if 5% of users convert to the cheapest plan, that’s $1.2 billion in high-margin recurring revenue against a roughly $5.8 billion advertising business. Not nothing.

But I’d cap realistic conversion at maybe 5-10%, and even that feels generous. You can literally save your memories straight to your camera roll for free. The whole value proposition is paying Snap to store something you could store yourself in about three taps.

And let’s be honest about what we’re preserving here—the average Snap memory is a drunk selfie with dog ears or a face swap that seemed hilarious at 2am. We’re not talking about family heirlooms.

Even if both subscription products hit their full potential, it doesn’t change the fundamental problem: they’re still an advertising company that can’t monetize users anywhere close to their competition. Snapchat+ and storage fees are nice diversification, but they’re not a new business model. They’re a side hustle.

Product vs. Investment

I’m not saying Snapchat the product is bad, despite me knowing very few people who still use it. It’s clearly doing something right for a certain group of consumers. The disappearing messages, the filters, the Snap Map, the whatever else they do on there that I don’t understand. All fine. The product has survived longer than anyone expected, and that’s worth acknowledging.

But there’s a difference between a good product and a good investment. Lots of companies make great products. That doesn’t mean you should own the stock.

Twitter was a great product. It was a terrible stock for years. GoPro made a product people loved. The stock went from the $90s to a penny stock. Peloton had a cult following. You know how that ended.

Product-market fit and shareholder returns are two completely different things, and Snap is maybe the clearest example of that disconnect in the entire market.

If I’m wrong here, it’s probably because management wakes up one day and decides to run the company for shareholders instead of themselves. That would require a dramatic shift in culture, capital allocation, and basically everything about how they’ve operated since day one. I don’t see evidence it’s coming. But if it does, I’d want to see years of restrained stock comp and actual share count reduction before I believed anything had changed. And by then, the stock would probably be higher anyway, so what’s the rush?

I don’t own Snap. I won’t be buying it. If you want to own social media, buy Meta. Zuckerberg has his flaws, plenty of them, but he actually returns capital to shareholders. He actually generates profits. He actually runs the company like he wants the stock to go up. Meta has been buying back tens of billions in stock while Snap keeps issuing more shares.

Evan Spiegel got paid over $600 million for completing an IPO and has spent the last eight years diluting everyone who bought it.

Red flag factory.

Disclaimer: This is not investment advice. Do your own research. I don’t own SNAP and have no plans to change that.

Since before their IPO it was obvious this was a horrendous stock to hold.

Crazy dilution through SBC (as you point out well), insane underwriting assumptions (I remember they assumed a WACC well below Facebook and Google at the time) and they never figured out how to monetize their product well.

It's felt like for a while the best thing for the shareholders would be to sell to a larger acquirer but Spiegel seems to enjoy being CEO with his type of control.