Shift4 (FOUR): Cheaper Than Ever

I keep waiting for the market to figure this out. It hasn’t.

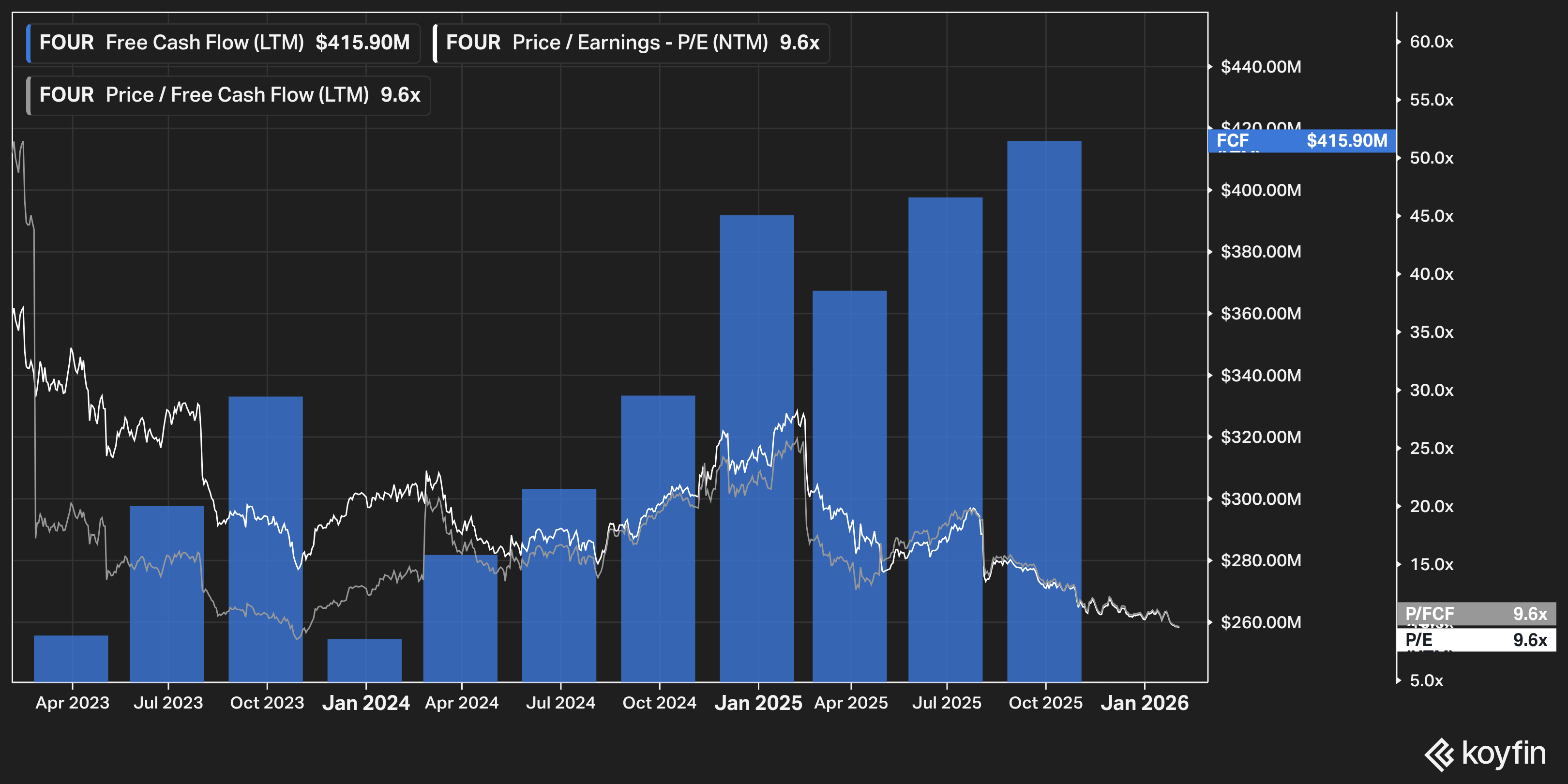

Shift4 hit another 52-week low this week. The stock is down over 50% from its highs, and down meaningfully from where I first wrote about it last September. Every time I look at the numbers, I think I must be missing something. Then I run through the thesis again, and I can’t find it.

At today’s price, you’re buying FOUR at roughly ~9x NTM earnings. If management hits their $1 billion free cash flow target for 2027 (a target they just reaffirmed last quarter), you’re paying under ~5x 2027 FCF. Even if they only hit half of it, you’re still under ~10x 2027 FCF.

For a company growing 20-25% a year with real operating leverage, that valuation makes no sense to me.

The company is also sitting on a $1 billion buyback authorization, which at the current market cap represents roughly ~20% of the entire company.

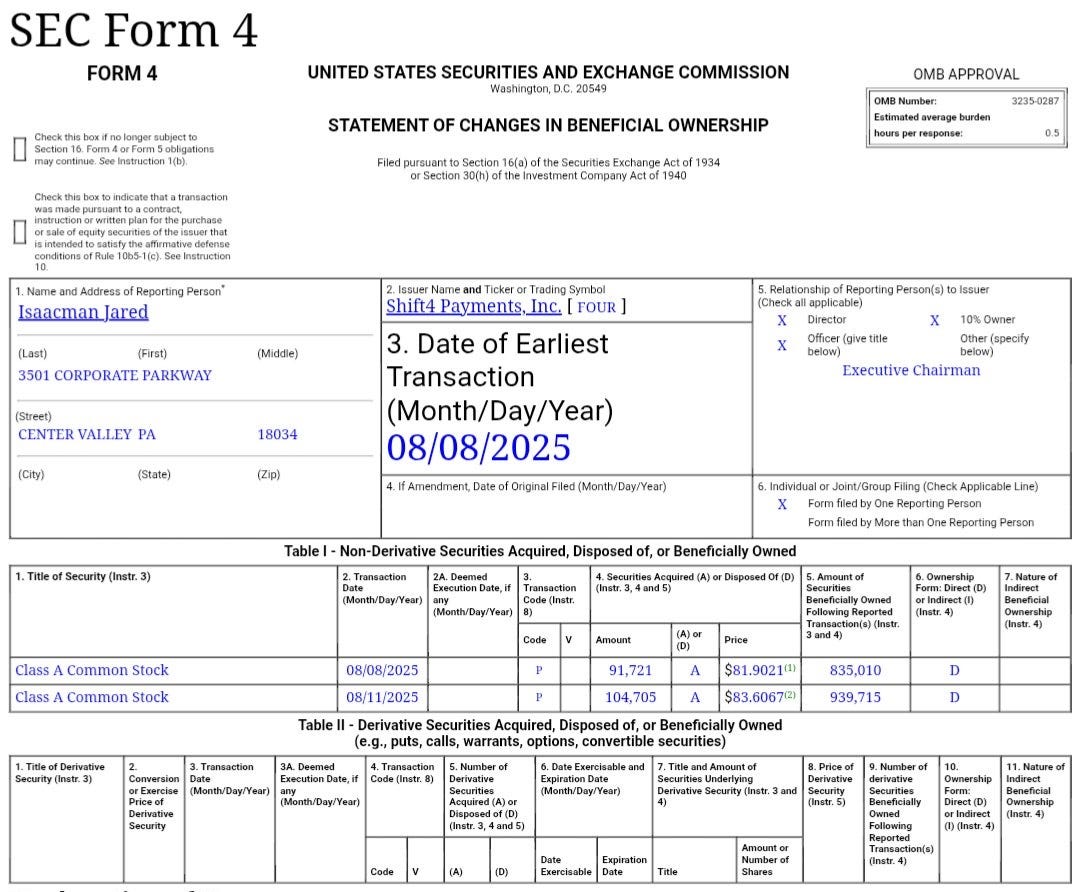

For context on where insiders see value: when the stock sold off after Q2 earnings last summer, Jared Isaacman spent over $16 million buying shares in the open market around $82-84.

He’s the one who founded this company and built it over two decades before handing the CEO role to Taylor Lauber. The stock is now under $60. If he was buying aggressively at $82, I’d imagine he likes it even more here.

And yet the stock keeps falling. At this valuation, there has to be something wrong… right?

That’s what I figured Michael Burry would find when he published an 8,000-word piece on the payments space a few weeks ago. I read the whole thing.

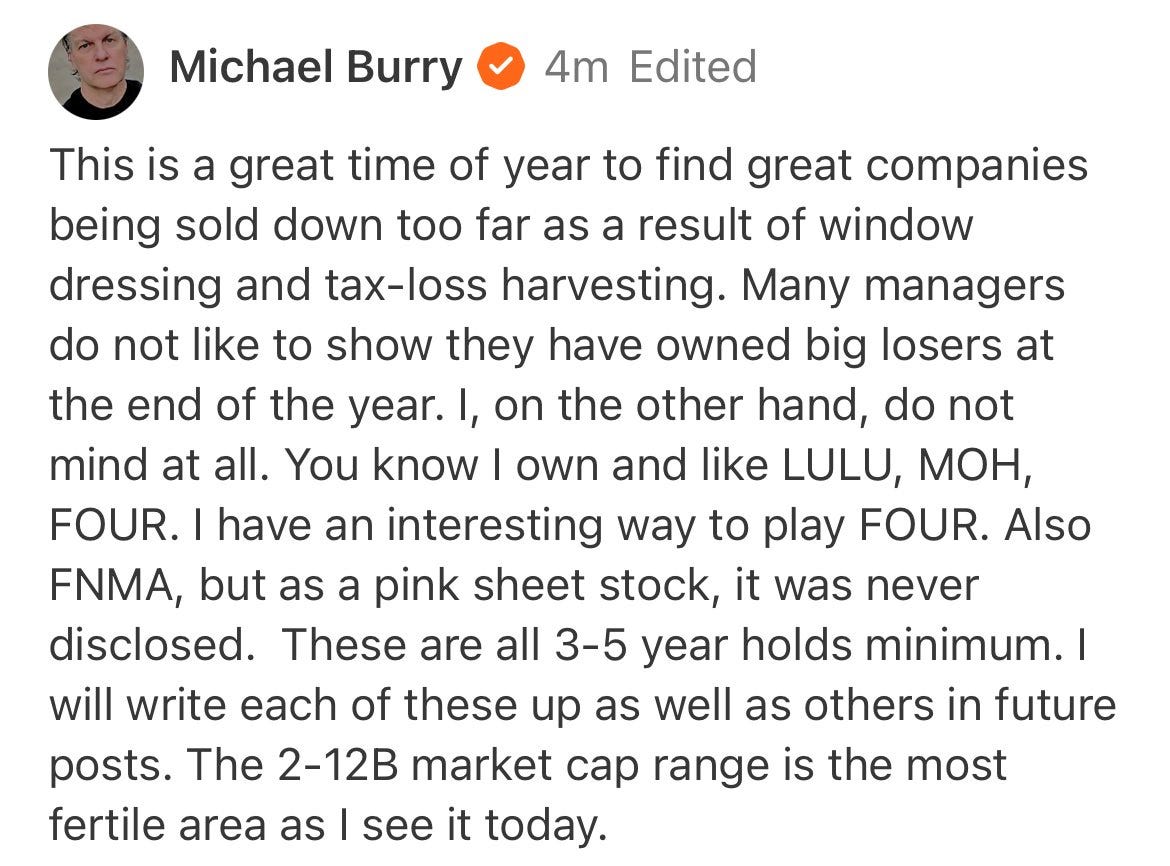

The thing about Burry is he sees things other people don't. Staying put long enough to benefit from what he sees is another matter. In late November, he posted that he owned FOUR and considered it a 3-5 year hold.

Six weeks later:

“I will wait for $30/share, and re-evaluate there. It is also possible that over the next month we get some good news catalysts on the governance front. Perhaps this dovetails with very good headline earnings to take the stock up again. In that case, I will miss it, and that is ok, by my analysis.” — Burry

That’s a lot of conviction lost in six weeks. Still, the piece is worth taking seriously — he went through every bear argument in detail, and his conclusion was more nuanced than the headline implied.