QXO: Consolidating Distribution

A serial acquirer rolling up distribution. Ground-level view.

When I’m not spending time with my daughter or digging into companies and writing here on Substack, I’m a project manager at a small construction company.

The bulk of our business is exterior work, mostly roofing and siding. Earlier this year, we switched distributors. After years of buying from ABC Supply, we moved to Beacon.

The reason was price. Beacon was coming in about ~15-20% cheaper on comparable materials. That’s huge... On a job that runs $20,000 in materials, that’s over $3000 back in our pocket. Over the course of a season, it adds up.

What caught my attention as an investor was that switching distributors isn’t something contractors do casually. Your rep knows your crew’s patterns. Your credit terms are dialed in. You’ve built trust around lead times and order accuracy over years. Switching is a hassle. But when someone undercuts you by a fifth, the hassle starts to seem worth it.

The other thing that caught my attention was how this fit into a pattern I see constantly in my work. The building products industry is fragmented at almost every level.

Distribution, materials, services. There are too many players, too many regional operators doing things the old way, and not enough scale anywhere. It’s inefficient, and inefficiency eventually gets corrected. Someone comes in, consolidates, and takes share. That’s happening now on the distribution side with QXO.

I think it’s starting to happen on the materials side too, which is why I’ve also been watching James Hardie (JHX) closely. More on that later.

Earlier this year, Beacon was acquired by QXO, a new company run by Brad Jacobs. The acquisition makes QXO the largest publicly traded distributor of roofing and building products in North America.

This is my attempt to work through whether QXO makes sense as a long-term investment. I’m biased because I see this industry every day from ground level. I’m also skeptical because founder-led roll-ups can blow up in a lot of ways.

I’ll try to separate what I actually know from what I’m guessing at.

Who is Brad Jacobs?

Brad is a serial consolidator. Over 40 years, he has built and scaled companies in waste management, equipment rentals, and logistics. His pattern is consistent: find a fragmented industry with inefficient operators, use acquisitions to build scale, then apply technology and operational discipline to widen margins.

His track record includes United Waste Systems, which he sold to Waste Management for $2.5 billion in 1997 after rolling up over 200 local waste haulers. Then came United Rentals, now one of the best-performing industrial stocks of the last 15 years with total returns north of 15,000%. And XPO Logistics, which he grew from $177 million in revenue to $14 billion in five years before spinning off pieces to surface value that the market wasn’t seeing.

Not everything went smoothly. United Rentals had a brutal stretch in its early years when Jacobs bet heavily on highway construction spending that didn’t materialize. The stock went sideways for over a decade before it compounded. XPO got bloated and complex before he restructured it. He’s made big mistakes. But he hasn’t had a catastrophic failure, and he’s learned from the ones that hurt.

If you want a deeper look at Jacobs and his history, Kairos Research has a more detailed write-up on him in his recent QXO post. Worth checking out.

What stands out is that Jacobs doesn’t just buy companies. He improves them. He flattens org structures, installs technology, centralizes procurement, and pushes pricing discipline through the system. He has talked about greenfield expansions generating higher returns on capital than acquisitions because the invested capital base is smaller.

That tells you he’s thinking about returns, not just growth.

He owns ~49% of QXO’s common stock through his investment vehicle, worth around $7 billion at current prices. His compensation is structured so that his salary only scales meaningfully if QXO reaches $30 billion or more in revenue. His equity incentives vest over years with strict performance hurdles tied to total shareholder return. This is about as aligned as you can get.

The Industry and Why It’s Ripe for Consolidation

The U.S. building products distribution market is roughly $800 billion. It’s one of the most fragmented industries I’ve seen.

There are an estimated 7,000 to 10,000 distributors in North America alone, most of them regional or local operators that have been doing things the same way for decades. Even the largest players typically hold only single-digit market shares.

There’s no dominant national player. The top distributors have meaningful presence in their regions, but no one has put together the kind of coast-to-coast scale that exists in other distribution categories. That gap is the opportunity.

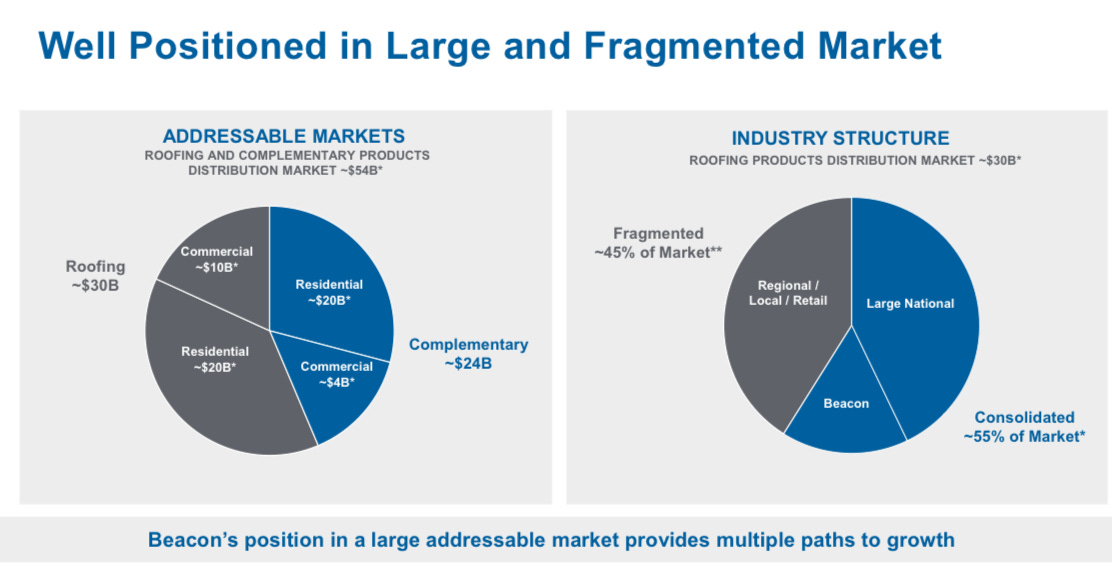

It’s worth noting how Beacon frames its own opportunity. Their investor materials show an addressable market of roughly $54 billion, but that’s just roofing and complementary products like siding and waterproofing. The roofing distribution market alone is about $30 billion according to their numbers, split roughly two-thirds residential and one-third commercial.