$PM, $BTI, $HAYPP: The Pouch Trade

Brand loyalty, explosive growth, and how to invest in the pouch boom.

I typically consume about 6-8 Zyn pouches a day. That probably clouds my judgment, but it also gives me a front-row seat to what’s happening.

A couple years ago, this was some random little tin tucked behind the counter. Now it’s everywhere. You see that faint circle in someone’s jeans and you know immediately. Finance bros, college kids, ex-smokers, the guy next to you on a flight—they’re all ZYN’ing.

What’s wild is how fast it flipped. Cigarettes were supposed to be dying a slow death, vaping was supposed to be the replacement, and then, almost out of nowhere, these pouches showed up and rewired the whole category.

Cigarettes take time, vapes need charging, dip needs a cup. ZYN needs nothing. No lighter, no smell, no charger, no spit. You put a pouch in and move on with your day. That little change is why Philip Morris, which was drifting along as a cigarette dinosaur, suddenly became a growth stock again.

I’ve tried the others. BAT’s Velo, On!, a few smaller brands. I hated all of them. ZYN is the only one I’ve stuck with, which tells me something about brand strength in this category.

The sticking power (at least in my experience) is real.

It’s Coke versus Pepsi, except the tilt toward Coke is heavier. When I run out of ZYN, I don’t say, “whatever, I’ll just grab Velo.” I drive to another store until I find ZYN. That’s habit and loyalty.

The whole ZYN shortage pretty much said everything you need to know. Demand blew past what PM could make, and for a while shelves were just bare. I remember walking into gas stations and the racks were empty—people were literally hunting cans like it was some kind of scavenger hunt. They’ve mostly caught up now, but it showed how sticky this habit already is. The only thing slowing it down was production.

And now you’ve even got RFK Jr. and the administration calling pouches a safer alternative. That’s huge.

“Nicotine itself does not cause cancer; there’s no evidence that it’s carcinogenic. It may, in fact, have some health benefits. It’s clearly addictive, but it may have other health benefits. We have an NIH study that shows it reduces the onset of Alzheimer’s and dementia. It’s infinitely preferable to smoking. I think nicotine pouches are probably the safest way to consume nicotine. Vapes are second. But the thing we really want to get away from is cigarettes.” — RFK Jr

Sure, flavors might get clipped and age rules will keep tightening, but an outright ban? Doesn’t feel like it. Not when politicians are already framing it as harm reduction.

From an investment angle, I keep coming back to one question: how did I miss this?

I’ve been hooked on ZYN for years, and somehow I didn’t own Philip Morris stock. I wrote up BTI this year because Velo was finally showing life in the U.S., and that story is real, but I can’t shake the feeling that PM had the golden goose sitting in plain sight the whole time.

ZYN has single-handedly changed the slope of PMs business. Before it, IQOS was the big reduced-risk bet—capital-intensive, messy in the U.S., complicated rollout. Now PM has U.S. growth, higher margins, and a product that investors actually pay a premium for.

BTI is interesting because the valuation gap is still huge, and Velo is finally scaling. They’ve got share gains, and the rest of their “New Category” is no longer a money pit.

But for me personally, when I think about the category, it still feels like ZYN’s game to lose. Velo might get to 20–25% share in a couple years, but PM already has the brand people ask for by name.

And that’s what got me intrigued by Haypp. As much as I’ve kicked myself for not owning PM while using ZYN every day, Haypp offers a way to play the trend without the rest of the tobacco exposure tied to the big conglomerates.

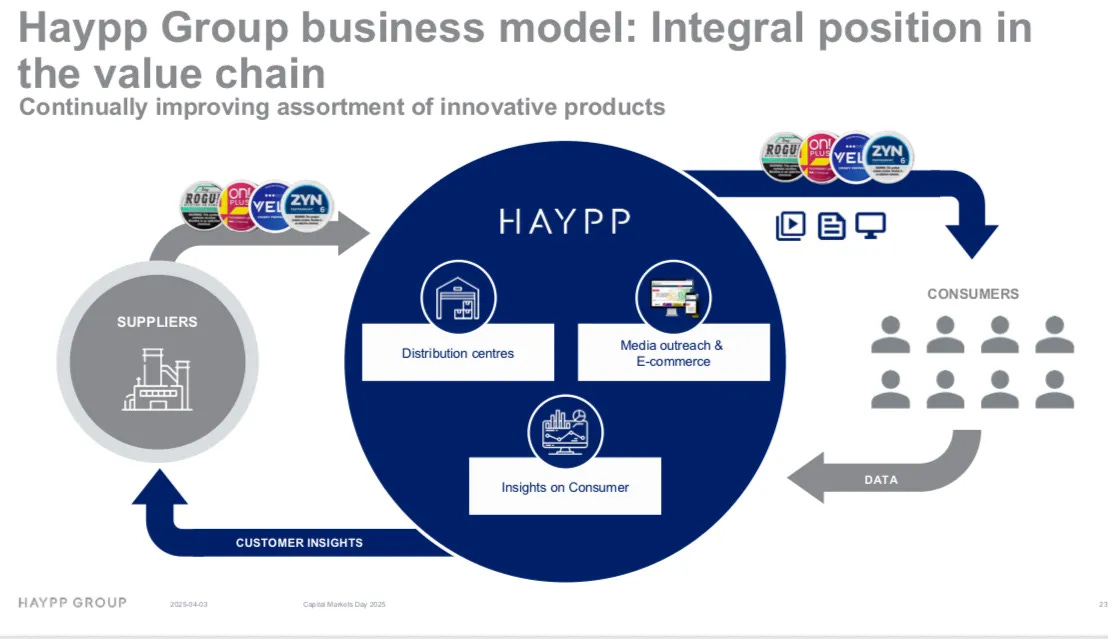

Nobody in the U.S. talks about it, but it’s the only pure-play on the pouch trend. They don’t make their own product; they sell everyone else’s online. ZYN, Velo, On!—all of them. Think of Haypp as the Amazon of nicotine pouches in Europe and the U.S., the digital shelf where the category lives.

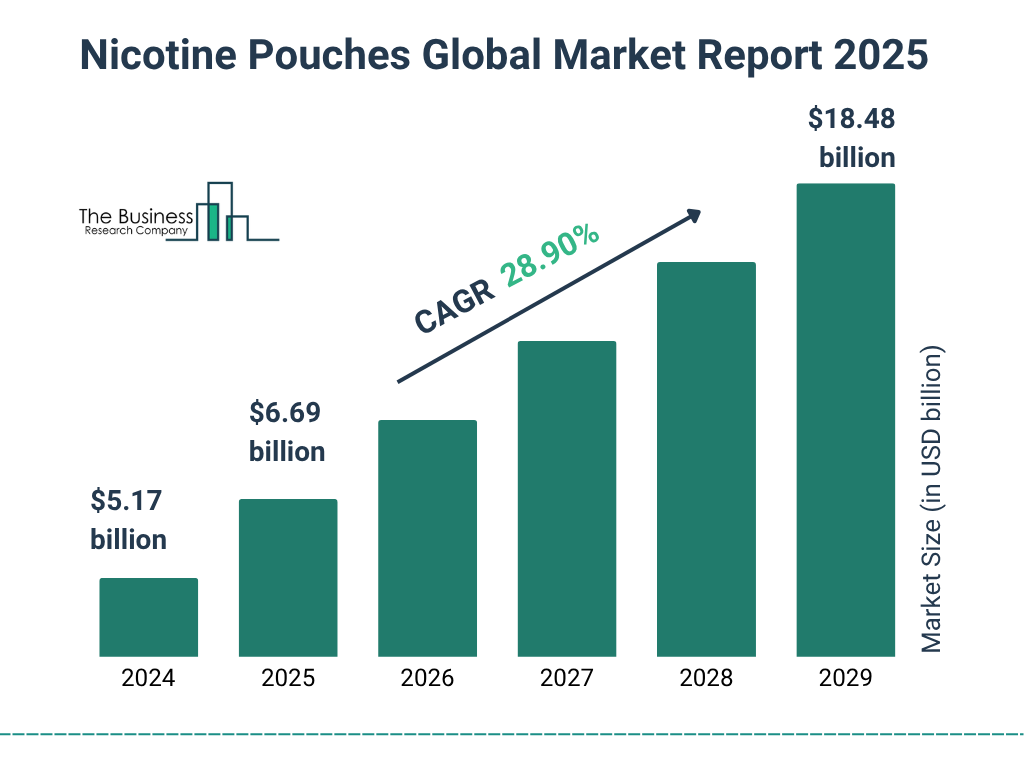

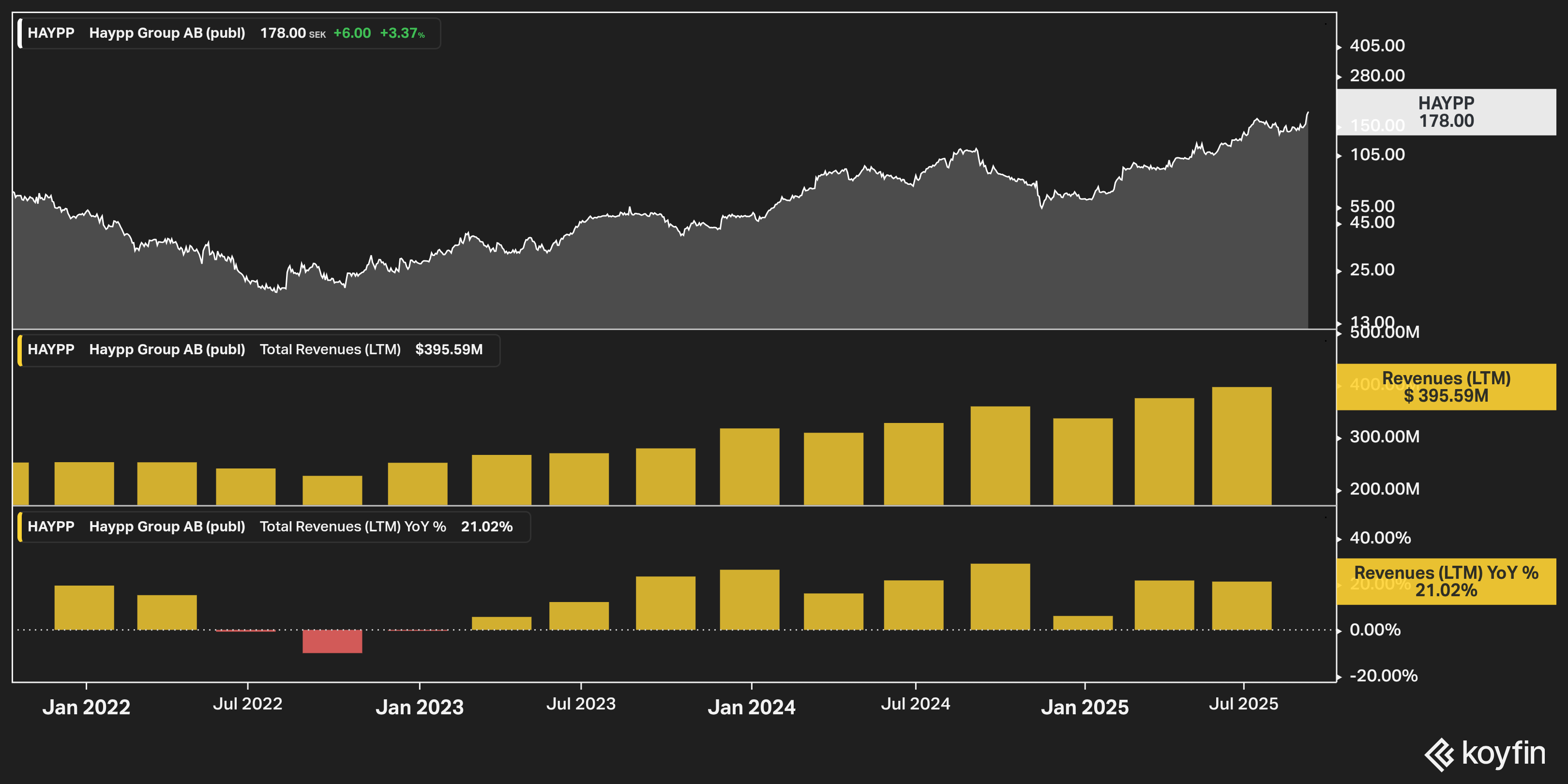

The stock has held up well. On paper it isn’t cheap—roughly 20x EBITDA and low-30s earnings. At first glance, that looks expensive. But the category itself is expected to compound at 20% a year, and management thinks Haypp can at least match that on the top line. If they’re right, the current multiples won’t look so demanding.

So what are investors paying for? At first glance it looks like just another e-commerce site, but the business model is a bit more complex than that. Haypp runs automated warehouses, ships cheap and fast, and offers the widest selection online. On the consumer side, they win because you can get exactly what you want, when you want it. On the supplier side, PM and BAT rely on Haypp not just for volume, but for data.

Every single order creates a data point: which flavor converts, which pouch size sticks, which price point actually moves demand. Multiply that across millions of customers and you’ve got a real-time insight engine into one of the fastest-growing consumer categories in the world.

That’s the real moat. Haypp monetizes that Media & Insights business by feeding information back to the suppliers who need it. That second revenue stream means Haypp can afford to sell pouches cheaper than anyone else and still make money.

It’s a flywheel: more customers → more data → more leverage with suppliers → lower prices → more customers.

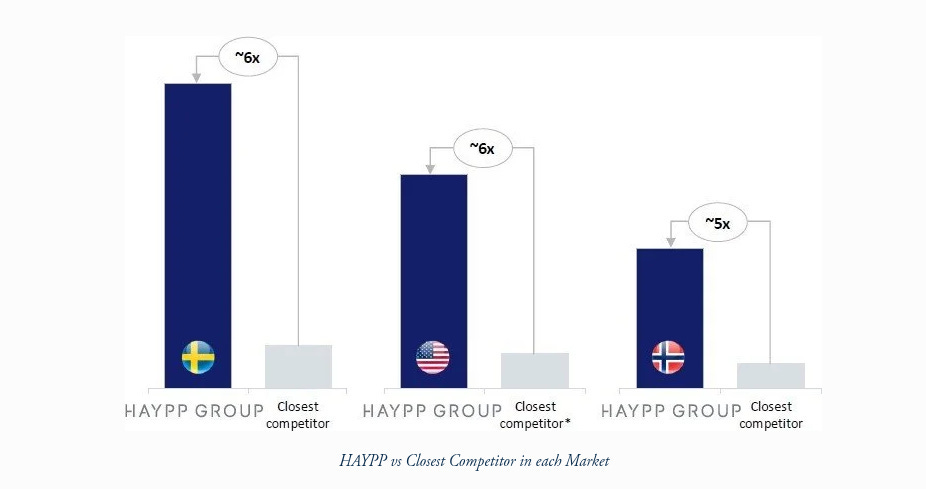

Competition only highlights the edge. Smaller rivals can try to buy share with discounts, but Haypp can keep prices lower indefinitely because it’s running on scale and data.

They’re already five to six times bigger than the next closest player, which means cheaper logistics, stronger compliance, and better unit costs. Regulation ends up working in their favor, because the little guys can’t keep up.

While it isn’t the screaming value BTI was earlier this year, Haypp is a rare setup as the only listed pure-play here. It’s capital-light, built on data, and sitting right in the middle of a category growing 20% a year. If the industry keeps compounding like that, Haypp’s numbers will compound too.

So how do you play it? You’ve got three ways in: PM, which already won with ZYN and has rerated because of it. BTI, which is still cheap and has optionality if Velo keeps catching fire. Or Haypp, the overlooked toll collector in the middle, running a capital-light, data-driven model that could quietly compound for a decade.

For me, the simple truth is ZYN works. It works so well I can’t quit it. I hate the alternatives and I’m definitely not the only one. This is exactly how consumers are behaving across the board. Habits aren’t rational. They’re emotional. ZYN fits into life better than cigarettes and easier than vapes, which is why it sticks.

The industry isn’t going back. Smokers are switching, new users are onboarding, and the growth curve is still steep. Regulation will create volatility—flavor bans, lawsuits, headline panics—but the category itself isn’t going away.

The real question is how you want to play it: the king (PM with ZYN), the challenger (BTI with Velo), or the overlooked platform in the middle (Haypp).

For me, I’m keeping a close eye on all three, but the more I dig into Haypp, the more it grabs my attention. It’s rare to find a pure-play on a consumer trend that’s this sticky, this habit-driven, and still this early in its adoption curve. The business model is capital-light, the data angle gives it a moat, and the scale advantage only gets bigger as the market grows. On the surface the stock doesn’t look obviously cheap, but if the category really does compound at 20% a year, today’s multiples won’t scare me.

That’s why I’m leaning toward Haypp as the way I want to play this. I’ll keep digging into the company, and on a pullback I’d like to start building a position.

This feels like one of those setups where, a few years from now, people will look back and wonder how obvious it was. The habit is here, the consumer has shifted, and I think Haypp has a long runway of growth ahead of it.