Pinduoduo (PDD): Cheap for a Reason

Pinduoduo is the kind of stock that, on paper, should be a layup.

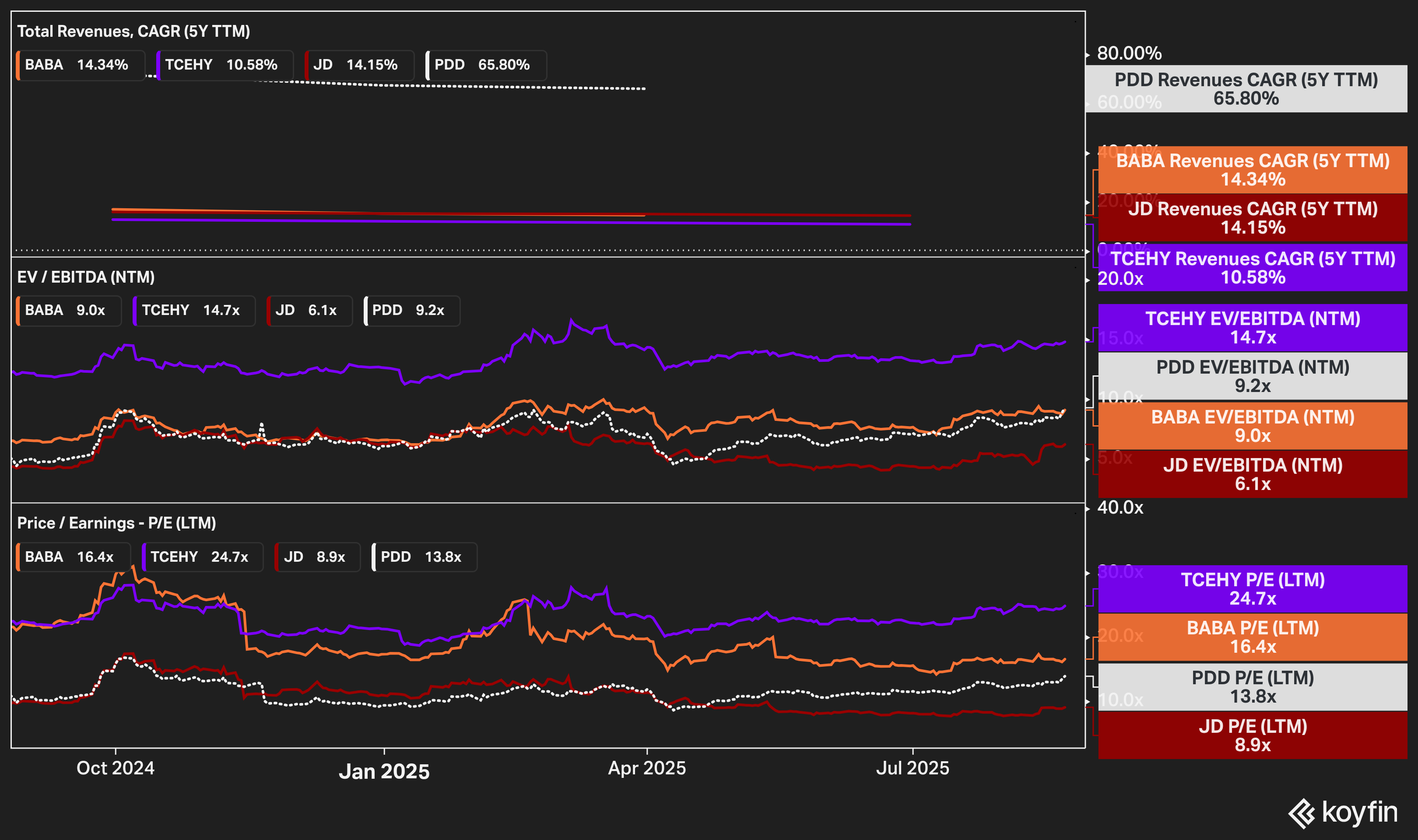

It’s growing faster than Alibaba, JD, and nearly every other Chinese internet platform. Profits are healthier, the balance sheet keeps swelling with cash, and it has managed to turn Temu—once dismissed as a cash-burning stunt—into a legitimate global business with traction in the U.S. and Europe.

All of that should be rewarded. And yet, the stock is cheap. Not just cheap compared to global comps like Amazon or MercadoLibre, but cheap even against other “out-of-favor” Chinese names.

Alibaba and Tencent already trade at cheap multiples, and JD screens even lower. But that’s the strange part. Pinduoduo is growing circles around all of them, yet the market values it like it’s in the same bucket.

Why?

Part of it comes down to narrative. Alibaba and Tencent at least have exposure to cloud and AI, which are the businesses investors want to own right now. China’s cloud market is in its infancy and growing rapidly, and both companies are positioned to capture a meaningful share. Investors (myself included) will pay a little more for that optionality.

PDD doesn’t have it. At its core, it’s still an e-commerce company. And while e-commerce is a good business, it doesn’t have the “next leg of growth” narrative that cloud and AI provide. That explains part of the discount, but not all of it.

The bigger issue is capital allocation.

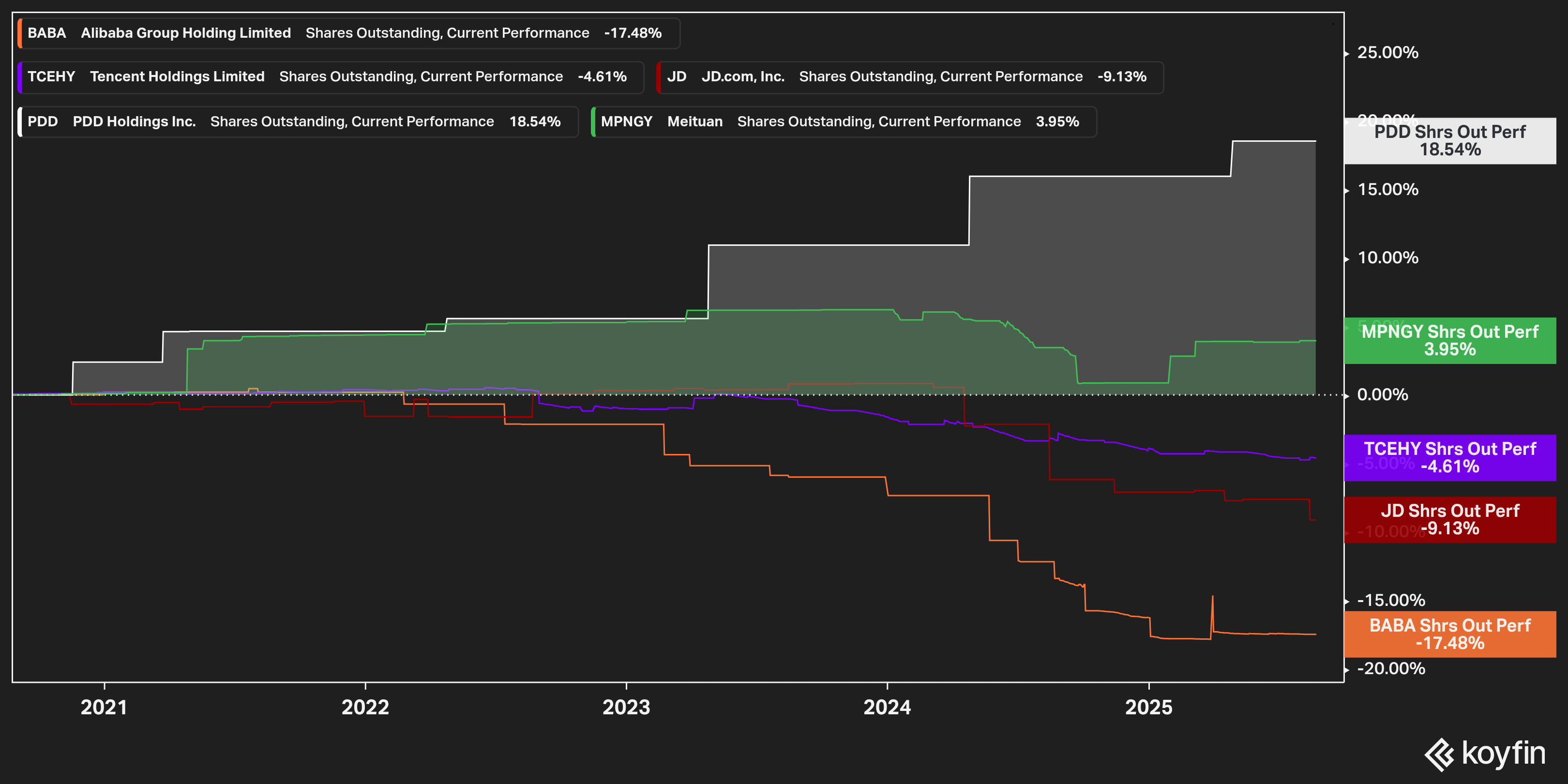

Its peers are all moving the other way. Alibaba is retiring stock at a record pace. Tencent has made it a habit. JD, once conservative, is getting more aggressive. And even Meituan is hinting at capital returns after years of nothing but reinvestment.

If you want to try Koyfin, the tool I use for all my charts and research, you can get 20% OFF with this link.

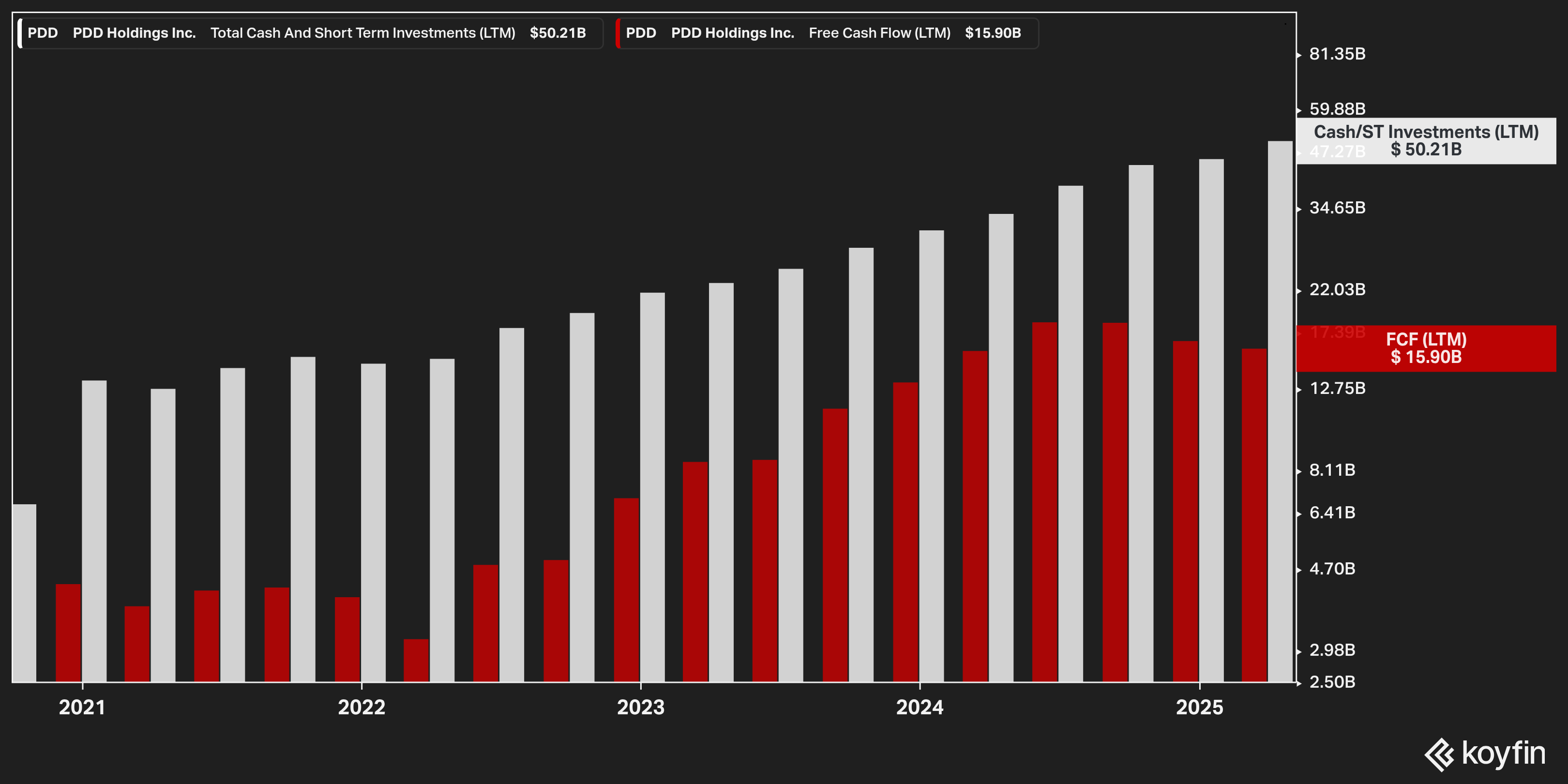

PDD has done nothing. The company sits on a giant pile of cash with no buyback, no dividend, and no indication that management intends to use it for the benefit of shareholders.

And it isn’t just capital allocation. Another problem is communication.

For a company of its size, PDD’s management is unusually quiet. They provide little in the way of guidance, avoid real discussion of strategy, and offer no clarity on how they think about returning cash to shareholders. Compare that with Alibaba or Tencent: you might not love every answer, but there’s at least a steady stream of disclosures and updates.

PDD, by contrast, acts like it doesn’t care whether investors understand the story.

In a market already skeptical of Chinese companies, that silence does real damage. Investors don’t just want numbers on a balance sheet—they want proof and signals that management sees them as partners.

That’s not a neutral choice. In a market where investors are already skeptical of Chinese companies, refusing to return capital and refusing to communicate sends the worst possible signal.

It raises the question: is the cash even real?

That might sound harsh, but credibility is earned. In markets like these, buybacks aren’t just financial engineering. They’re proof of concept. They tell you three things:

Management knows the stock is cheap.

The cash generation is real.

Shareholders aren’t an afterthought.

Without those signals, investors are left staring at big numbers on a balance sheet they can’t touch. Profits and cash flow look great in filings, but if none of it ever comes back to the owners, the market is right to treat them as theoretical.

That’s the paradox at the heart of PDD. On almost every metric—growth, margins, cash flow—it looks stronger than peers. But on the single metric that builds trust with shareholders (capital returns) it has done nothing. And so it trades at a discount to the very companies it’s out-executing operationally.

This is why I don’t own it. I don’t doubt the growth story. I don’t doubt the quality of the core business. But I do doubt whether management sees outside shareholders as true partners. Until that changes, I think the stock will remain stuck.

It’s a case study in why cheap stocks can stay cheap. PDD shows how the market can discount even the best growth and profitability when trust is missing. Scale, margins, and cash generation don’t matter if management won’t give shareholders a reason to believe in the numbers.

Until that changes, I think the stock will remain in the penalty box.

Really great insights, thanks for sharing this!

This is great timing as I actually looked at PDD recently before JD and came away more convinced by JD for exactly the capital allocation point you make. I liked that JD has started to move the needle including through large-scale buybacks. On that though, I’m still not entirely convinced by the JD management and I take it that’s why the others are preferred.

Very interesting. Haven't thought about this cap allocation issue.