Palantir and the Illusion of Growth

Not a short, just a warning

I rely on Koyfin as a core part of my investment research. It’s a powerful platform for tracking markets, analyzing fundamentals, and building custom charts—all in one place.

Try Koyfin now and get 20% off any paid plan.

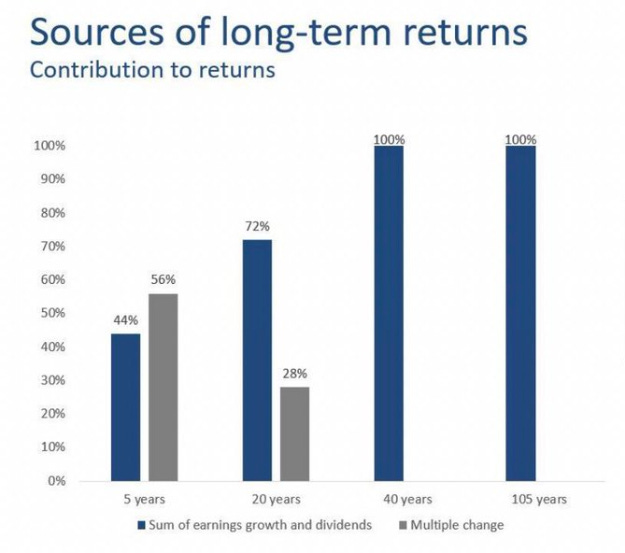

Over time, fundamentals drive stock returns. Earnings growth, free cash flow, dividends—that’s what compounds. In the short run, multiples can stretch, and that can fuel incredible gains. But multiple expansion is borrowed time. Eventually, the business has to catch up.

Over a 5-year stretch, a stock can rally just because the market assigns it a higher multiple. Over 20 or 30 years, that contribution fades to zero. What’s left is what the company actually delivered.

Which brings me to Palantir.

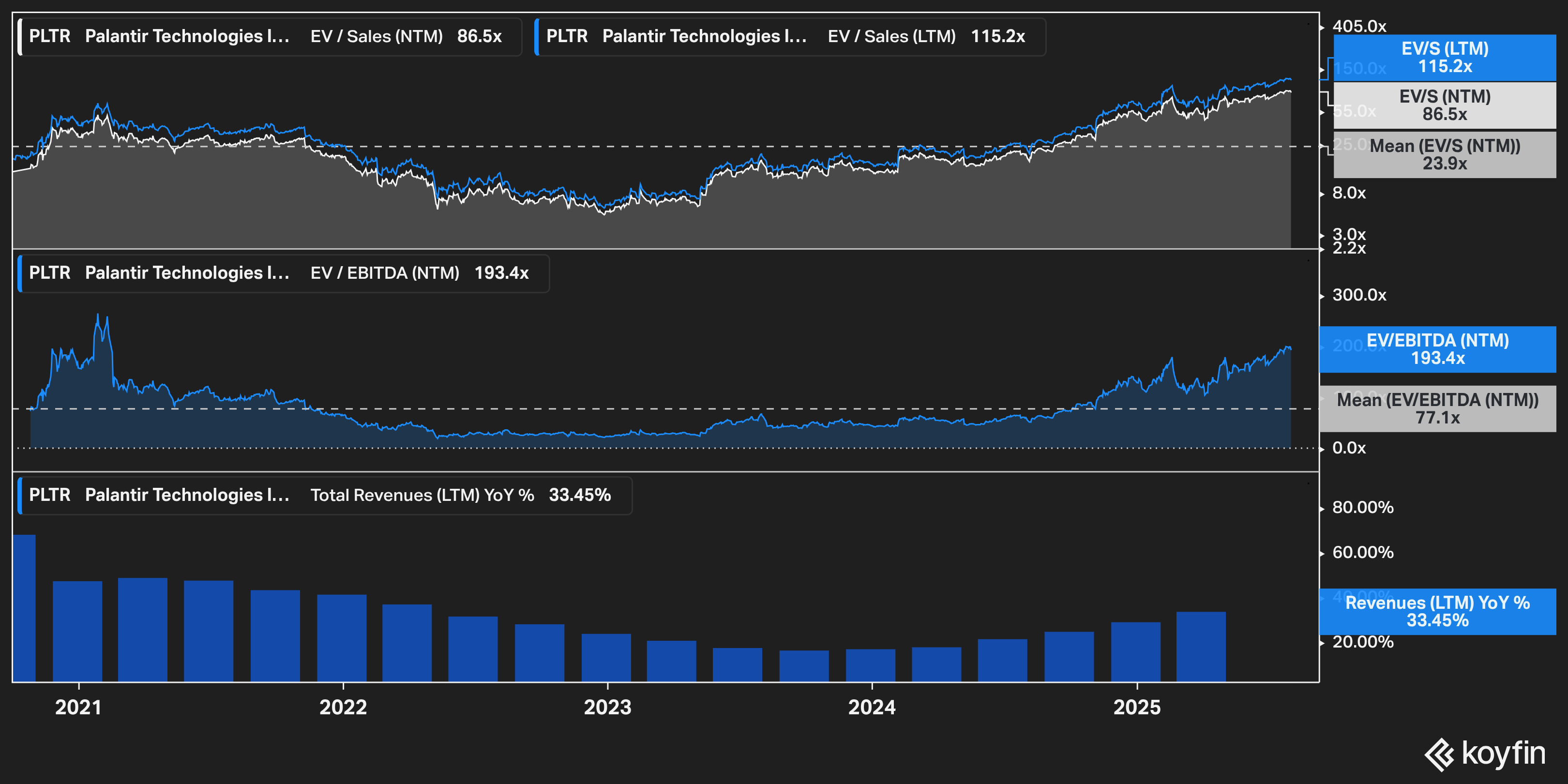

Revenue has grown about 30% annually. That’s strong—but not unheard of. Meanwhile, the stock is up more than 20x since 2023. It didn’t happen because the business scaled 20x. It happened because the multiple did.

In late 2023, Palantir traded at around 10-15x forward sales. Today, it’s pushing 86x. That’s not sustainable. It’s not normal. And it’s not something the fundamentals can justify.

And that’s why, even though I’m not short Palantir—and don’t plan to be—it’s near the top of my list of the most irrationally priced stocks in the market today. Maybe ever.

The business isn’t bad. Actually, it’s getting better.

Commercial traction is improving, government contracts are scaling, and they’ve done a good job pivoting into the AI narrative. But that’s exactly the problem. The market hasn’t just priced in the next few years of growth—it’s priced in a perfect decade.

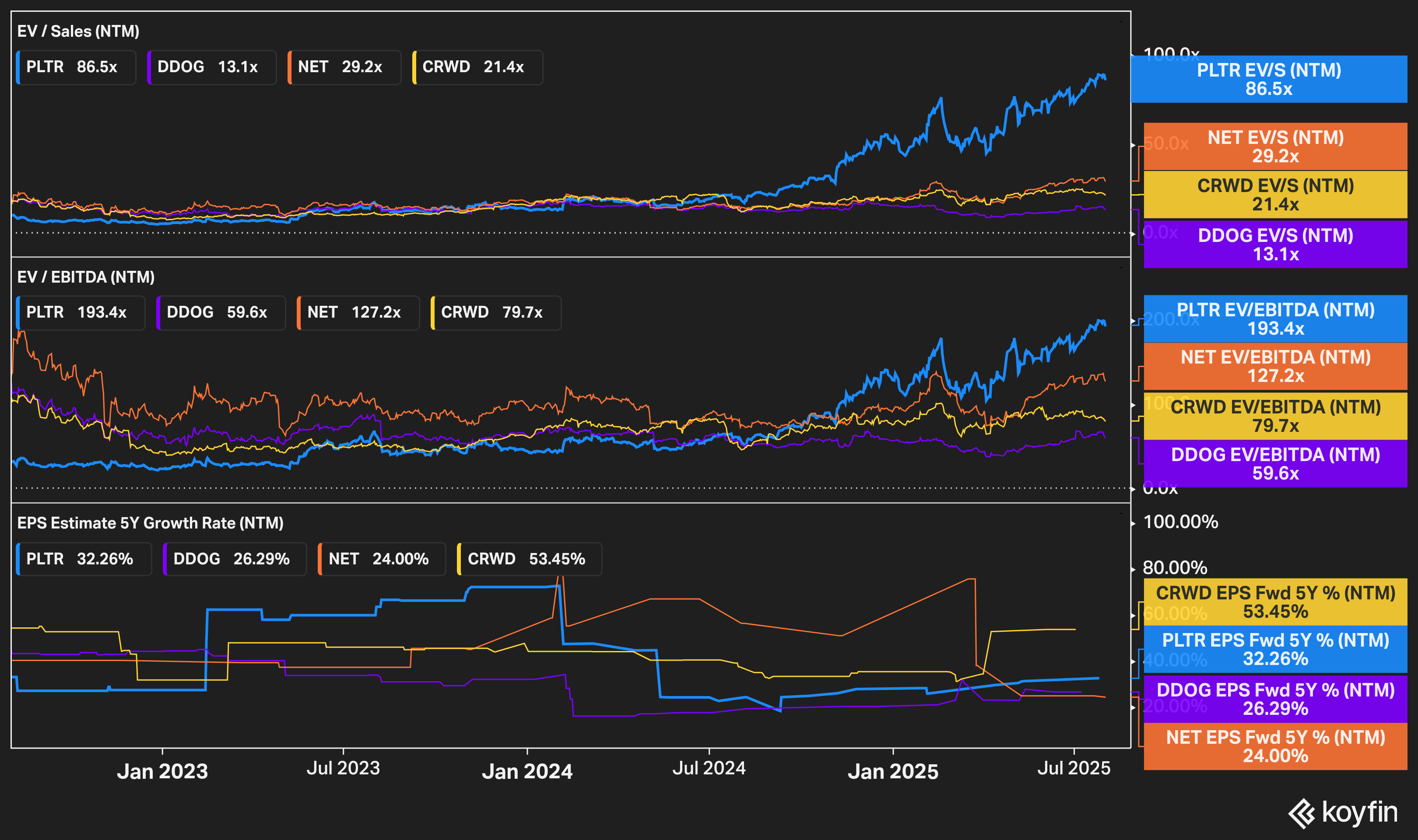

Palantir now trades at 115x trailing sales, 86x forward sales, and 193x forward EBITDA. Not tech bubble numbers. Worse. And it’s not like we’re talking about a $400M-revenue company growing 80%. Palantir is doing ~$3.1B in revenue at a ~31% 5Y CAGR.

At this valuation, you’re paying for Amazon-like scale, Microsoft-like margins, and Nvidia-like terminal growth—all at once. The fundamentals don’t support it. Not even close.

Let me be clear: I think the AI angle has legs. Palantir’s platform is sticky, their work with government agencies is real, and the software has found product-market fit in certain verticals. They’re trying to be the control panel for operational AI. It’s a legitimate business.

But none of that justifies a 100x+ revenue multiple. These numbers don’t make sense. Not in software. Not in AI. Not anywhere.

Let’s say you’re bullish. You think they keep growing revenue at 30% a year through 2029. That gets them to around $11.5 billion in sales. Assume they eventually reach a 30% EBITDA margin—that’s $3.45 billion in EBITDA.

At a $360 billion enterprise value, that’s still 104x 2029 EBITDA

Even on a forward revenue basis, you’re looking at 86x sales. Most high-growth software names trade between 15–20x. The best names—Cloudflare, Datadog, CrowdStrike—rarely go above 30x, even when they’re growing at similar or faster rates than Palantir, and with similar or better margin profiles. And none of them are even close to 50x, let alone 86x.

So even if you re-rated this stock down to 40x forward sales, which is still extreme, you’re looking at 60%+ downside.

Let that sink in: if Palantir re-rated to one of the highest multiples in software—something still rarefied—it would need to fall more than half from here.

And that’s not a short case built on collapse. That’s just gravity.

The problem isn’t the business. It’s the expectations.

Palantir is being valued like it’s already won the next decade of AI. Not just participated—but won. The stock is pricing in perfect execution, massive margin expansion, government scale, international growth, and some magical AI moat that no one else can match.

But let’s be honest about what Palantir actually is.

They build powerful, niche software for large enterprises and government agencies. They help deploy models, organize data, and integrate AI into workflows. It’s valuable software—but it’s not unique, and it’s definitely not infrastructure. They don’t own the chips. They’re not building LLMs. They don’t run a public cloud.

They’re not Nvidia. They’re not Amazon. They’re a verticalized data platform with strong sales relationships and some AI integration.

A great business? Yes. A 100x revenue business? Not even close.

What makes this even more dangerous is the sentiment. Palantir has become the retail AI darling. The stock is up over 20x since 2023. It’s up more than 110% this year alone. It’s in every ETF. Every FinTwit thread. Every momentum screen.

This is a crowded, over-loved stock that’s already had its run. And now it’s priced like nothing can go wrong.

But something always does.

It might be a weak quarter. It might be slower commercial growth. It might be government budget pressure. Or it might just be that the market stops rewarding stories and starts caring about cash flows again.

And when that shift happens, names like this don’t correct 20–30%. They reset. Hard.

We’ve seen this movie before: Zoom, Snowflake, Unity, Teladoc. All good businesses. All sold as the future. And when sentiment cracked, the drawdowns weren’t small. They were brutal.

Palantir doesn’t need to fall apart to drop 70%. It just needs to go from priced-for-perfection to priced-like-a-normal-company.

Again—I’m not short. I don’t hate the business. But at $360 billion, this is not a stock for fundamental investors. It’s a trade. A bet on sentiment staying hot. And when that tide turns, there’s a long way down.

Completely agree. At some point valuation matters.

backed the sentiment with actual data. very concise and well written!