Everyone Hates China. That’s the Opportunity.

Policy is turning, consumption is rebounding, and tech is back in focus. The case for China is stronger than it looks.

Most readers know where I stand on China. I’ve been bullish on the long-term opportunity here for years—through the noise, through the drawdowns, and through the seemingly endless headlines about why “China is uninvestable.”

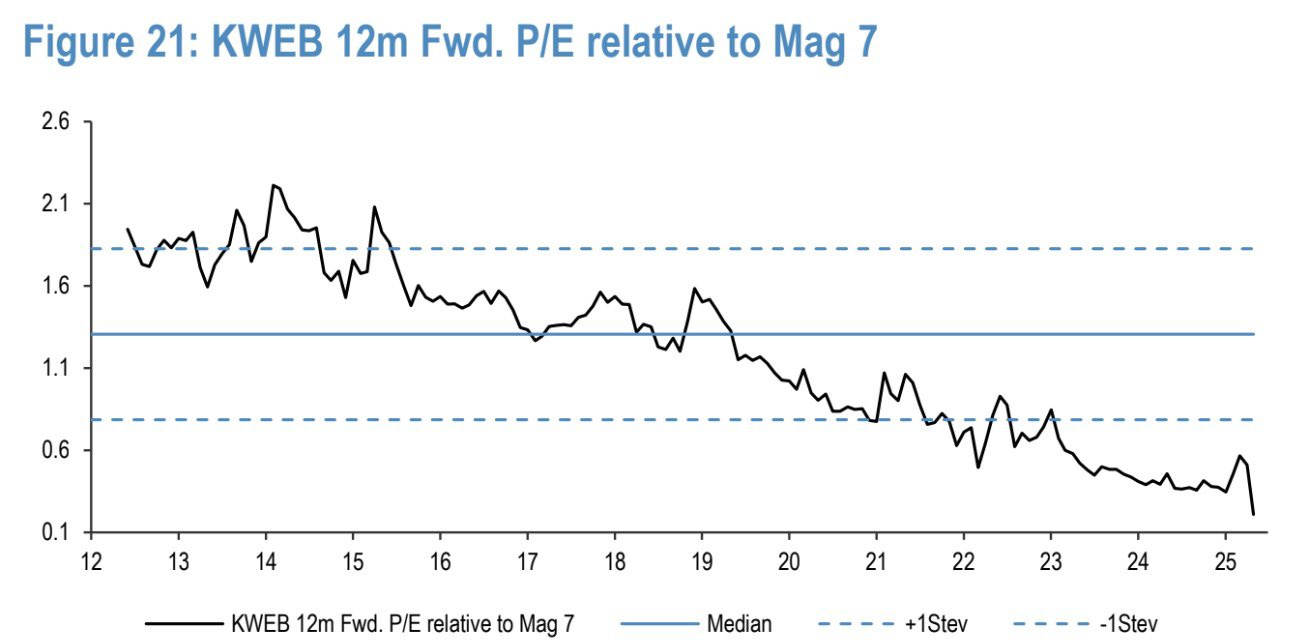

My largest positions include companies like Alibaba and Tencent, which I’ve held through some brutal sentiment cycles.

That conviction hasn’t been easy to maintain. The past couple years have tested even the most patient investors. Policy tightening. Regulatory pivots. Lockdowns. A property collapse. Weak consumer sentiment. There were moments when it felt like the whole market had given up on China ever returning to form.

But part of the reason I’ve stayed long is simple: valuations are dirt cheap.

These are world-class businesses—dominant platforms with massive scale and profitability—trading at single to low double digit earnings multiples and deep discounts to global peers. The dislocation has never made much sense to me. And now, with policy finally turning more supportive and macro signals starting to improve, the case is only getting stronger.

From Sentiment Collapse to Policy Support

Here in mid-2025, the narrative is starting to shift.

Slowly, quietly—and this time, with real policy support behind it—the Chinese consumer is coming back. Travel is rebounding. Retail is recovering. Car sales are climbing. And for the first time in years, the data and the policy message are aligned: Beijing wants consumption to lead, and it’s willing to do what it takes to make that happen.

This wasn’t always the case. Through 2022 and much of 2023, the government’s response to weak domestic demand was half-hearted. Stimulus measures were inconsistent and often aimed at stabilizing supply-side industrial production or propping up struggling real estate developers, rather than stimulating household demand.

Consumers, especially younger ones, remained wary. Unemployment lingered in the double digits. Savings rates soared. The mood was defensive, and spending reflected that.

But 2024 brought a notable pivot. And by mid-2025, that pivot has become policy doctrine.

The latest signal came in June, when Premier Li Qiang addressed the Asian Infrastructure Investment Bank’s annual meeting and declared that “domestic demand is the foundation of China’s economy.” Shortly afterward, a sweeping package of consumption-linked policies was unveiled.

This included ¥500 billion in relending directed at sectors with high-touch consumer activity—elder care, catering, education. At the same time, authorities expanded credit channels for consumption loans and launched a nationwide initiative encouraging trade-ins of home appliances, electronics, and even vehicles.

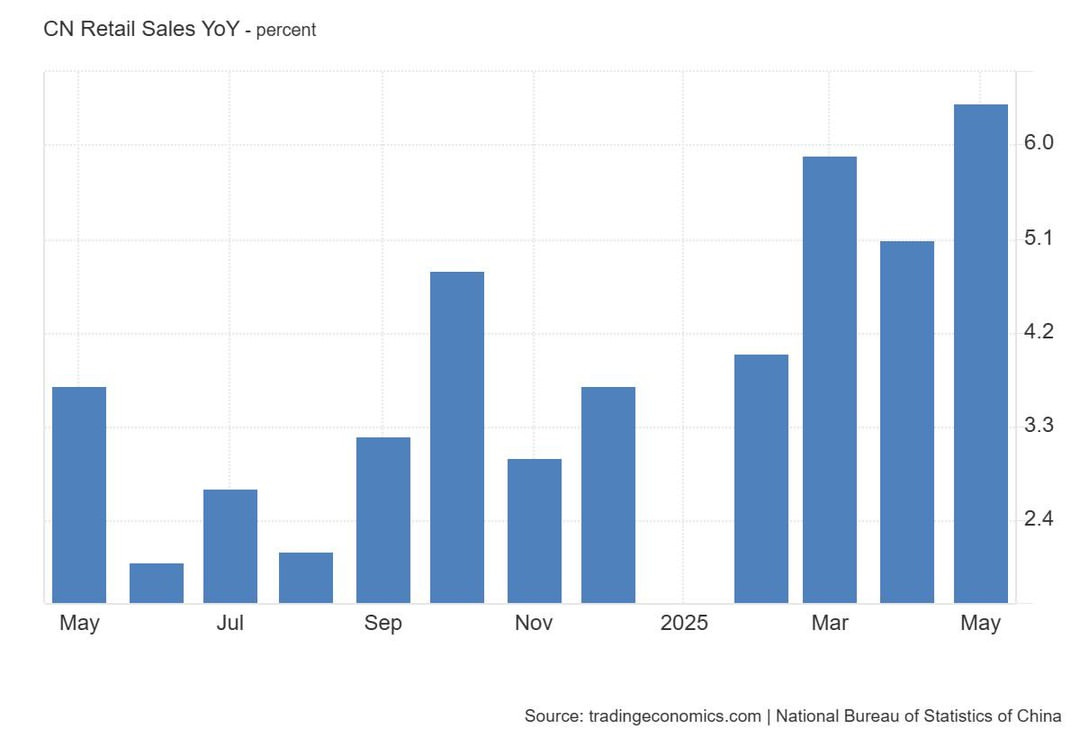

Unlike past announcements that took months to filter through, this time the effect has been swift. You can see it in the data. In May, retail sales rose 6.4% year-over-year, beating expectations and marking the fastest pace since late 2023.

That acceleration wasn’t solely driven by the early kickoff of the annual “618” e-commerce festival. Yes, platforms like Alibaba and JD.com leaned into discounts, but the real surprise came from offline categories: apparel, small appliances, and digital goods sold in lower-tier cities all saw strong increases. These are precisely the segments targeted by provincial trade-in subsidies and digital coupons—proof that the incentives are landing where they’re meant to.

Travel data tells a similar story. During the May Day holiday, 314 million domestic trips were recorded—a 6.5% rise from last year. Hotel bookings surged. Restaurant traffic returned. Overall tourism spending was up 8%, totaling ¥180 billion. Even international travel—long considered a laggard post-COVID—showed signs of life. Over 10 million Chinese citizens traveled abroad during the holiday, a near 29% year-over-year jump. These aren’t the behaviors of a population tightening its belt.

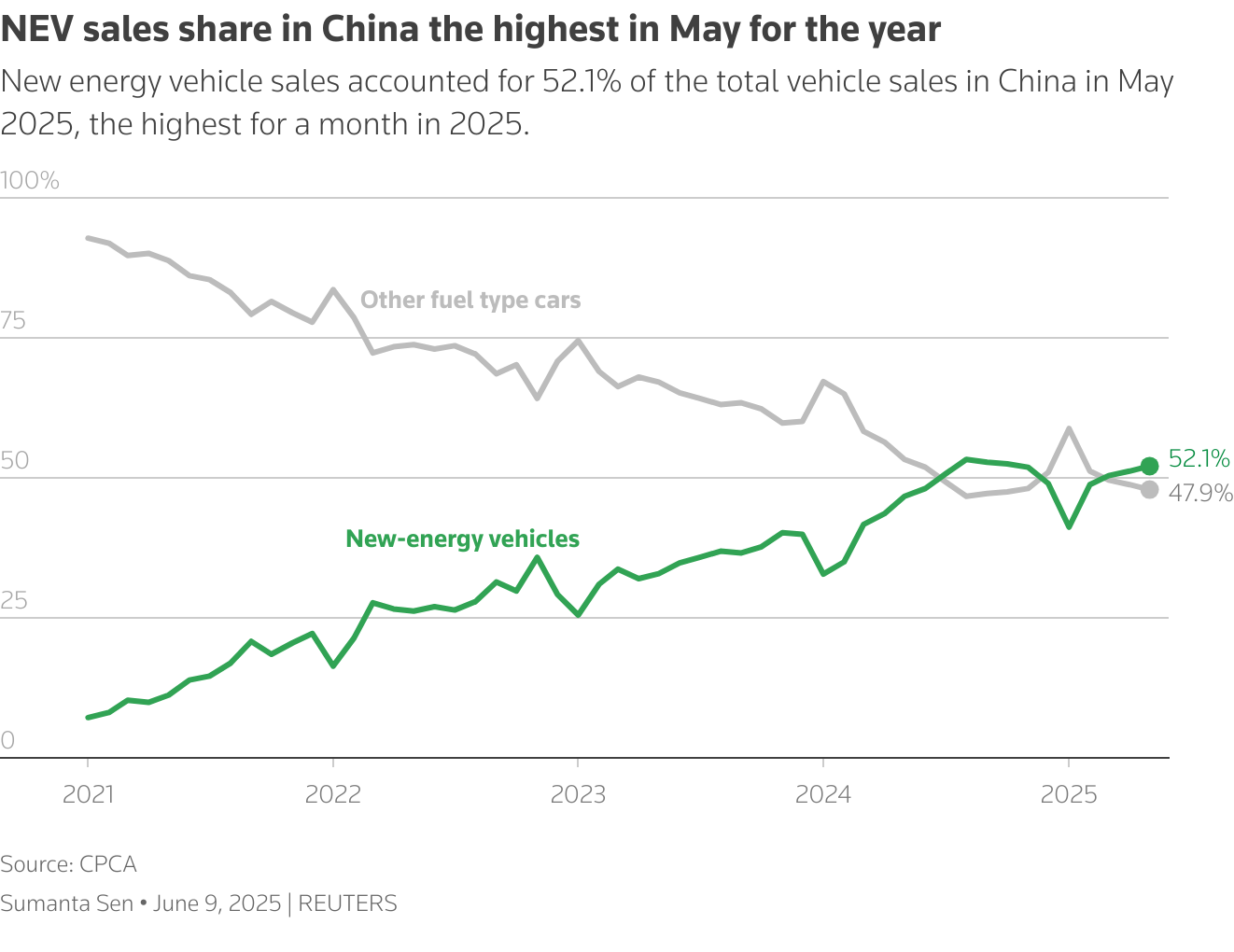

The auto sector—long viewed as a barometer of consumer confidence—is seeing similar momentum. Passenger vehicle sales hit 2.69 million units in May, up 11.2% year-over-year. New Energy Vehicles (NEVs) were the standout, growing 28% and accounting for more than half of total passenger vehicle sales. While government incentives have supported this growth, that’s only part of the story.

What’s happening now is more structural. In second- and third-tier cities, a new cohort of younger, aspirational buyers is emerging. They’re purchasing EVs not just for affordability or environmental reasons—but because these cars represent autonomy, status, and upward mobility. BYD, Li Auto, and XPeng are scaling up deliveries. Even Tesla, after aggressive pricing adjustments, is clawing back market share.

And everyday services? They’re normalizing too. Meituan—China’s all-purpose platform for food delivery, groceries, travel bookings, and more—posted 18% revenue growth in Q1. Profits nearly doubled. Importantly, this wasn’t growth driven by one-off subsidies or flash promotions. It was higher order volume across the board: more meals delivered, more hotel stays booked, more local services used. This kind of recovery is harder to fake. It suggests something more durable is underway.

Not Just Consumption—Technology Is the Second Engine

But what makes this recovery more compelling isn’t just that the consumer is coming back—it’s the fact that it’s happening alongside a broader national push into strategic technology.

If the first engine of China’s economic plan is to restore household demand, the second is to build out a future-proofed digital and AI-driven economy. And in 2025, that ambition is becoming reality.

The central government has made it clear that AI, semiconductors, and foundational tech infrastructure are no longer optional—they’re core to China’s vision of productivity and competitiveness. In recent months, state-linked funds have poured billions into domestic players like Zhipu AI, one of the country’s top LLM developers, and Biren Technology, a leading chip designer poised for IPO. Beijing’s support isn’t just capital—it’s access to data, regulatory clearance, and alignment with national goals. For these companies, that backing translates into runway and relevance.

What’s especially notable is how deeply AI is now embedded in China’s consumer-facing platforms. Alibaba is integrating generative models into search, logistics, and merchant operations. Tencent is deploying AI across content delivery, gaming mechanics, and personalized ad targeting. JD.com is using large models to streamline inventory management and optimize warehouse routing. These aren’t experiments—they’re commercially scaled rollouts.

The result: higher engagement, more efficient cost structures, and—crucially—the return of margin expansion across China’s big tech platforms.

For years, the post-regulatory era forced these companies into capital preservation mode. But with policy pressure easing and new tools finally monetizing, investors may start to see real earnings power return. Alibaba, Tencent, JD, and Baidu are no longer just cheap—they’re beginning to look operationally lean and technologically competitive. And that matters.

A Government Finally Willing to Back Business

That doesn’t mean everything is fixed. Youth unemployment remains high. The property market is still under pressure. Industrial output growth has been soft. And geopolitical risks—particularly with the U.S. and Europe—still cast a long shadow over trade and investment flows. But the momentum is real, and the policy direction is no longer ambiguous.

And for the first time in years, there are signs that China’s leadership is recalibrating its relationship with business. Regulators are easing off platform crackdowns. Local governments are actively encouraging capital market listings. SOEs are under pressure to improve returns. And large private companies—from tech to logistics—are being allowed to refocus on growth and profitability. It’s not just pro-growth policy—it’s becoming pro-company. And in some cases (specifically Alibaba, JD & Tencent), even pro-shareholder.

Beijing isn’t hoping the private sector figures it out—it’s actively laying down the scaffolding. This isn’t the old playbook of flooding the market with credit. It’s more careful, more targeted, and arguably more sustainable. Support for household demand is being delivered through precise programs. Support for the future is being routed through strategic capital allocation into AI and infrastructure.

It’s not a sugar high. It’s a strategy.

If 2022 was the year of lockdowns, and 2023 the year of policy ambiguity, then 2025 may be the year China embraced its long-planned consumption pivot—backed by coordinated government support, real household demand, and a national tech buildout that may quietly reshape the country’s economic base.

For now, the Chinese consumer is coming back. And this time, they’re not coming back alone—they’re joined by the country’s most important companies, technologies, and capital allocators.

Not with fireworks. But with focus.

Comprehensive outlook of the current situation!

Any broker recommandation to buy Chinese and more broadly Asia ? I use interactive broker but it seems that they apply a min of 100 shares to buy over many stocks in local currency (not ADR)