China’s Rally Has Real Legs

Household savings, policy support, and a shareholder-friendly turn are pushing China’s market higher.

I’m a value guy. I like durable businesses at fair prices, then letting time do the heavy lifting. But every once in a while the market gives you a second gift: the thing you own for fundamentals also starts to trend.

When that happens, the right move isn’t to fight the market, it’s to let the wind at your back do some work.

That’s the setup in China right now. Call it phase one: the value case finally has a momentum tailwind. The real question is whether that tailwind is just a sugar high or the beginning of a proper cycle. One where flows, policy, and company behavior reinforce the move instead of choking it off.

The tape is speaking (and yes, price matters)

We’ve had a clean run across the China complex. The China internet basket has been firm, broad China has tracked higher, and several bellwethers reclaimed long-term moving averages and started printing higher highs. And price, inconvenient as it can be, is a loud signal in this business.

I’m not abandoning fundamentals. I am admitting the obvious: when price and fundamentals rhyme (even a little) you don’t have to be a quant to benefit.

I own Alibaba, Baidu, and KWEB. I didn’t buy them to make a point on Twitter; I bought them because the setup was very lopsided: strong assets, improving mix, and valuations that assumed permanent decline.

Now the market is finally cooperating. If that sticks, systematized capital tends to show up.

You can already see the flywheel begin to form.

Global managers have been heavily underweight China for years. Underweight plus rising price equals career risk. Benchmarks amplify it, factor models pile on, and discretionary money plugs the gap. That’s how rallies become regimes.

But momentum itself obviously isn’t the thesis. It just tells you the tide may be turning. The real question is whether there’s fuel behind it—and this time, there is.

Household savings, policy shifts, and a newfound culture of shareholder returns are all things China hasn’t had in prior cycles. That’s why this doesn’t have to be just another head fake.

Where the fuel comes from

If this rally turns into a real cycle, it won’t be because a chart looked pretty. It’ll be because an enormous wall of savings finally decides to leave the bank and policy makers stop choking the equity market every time it starts breathing.

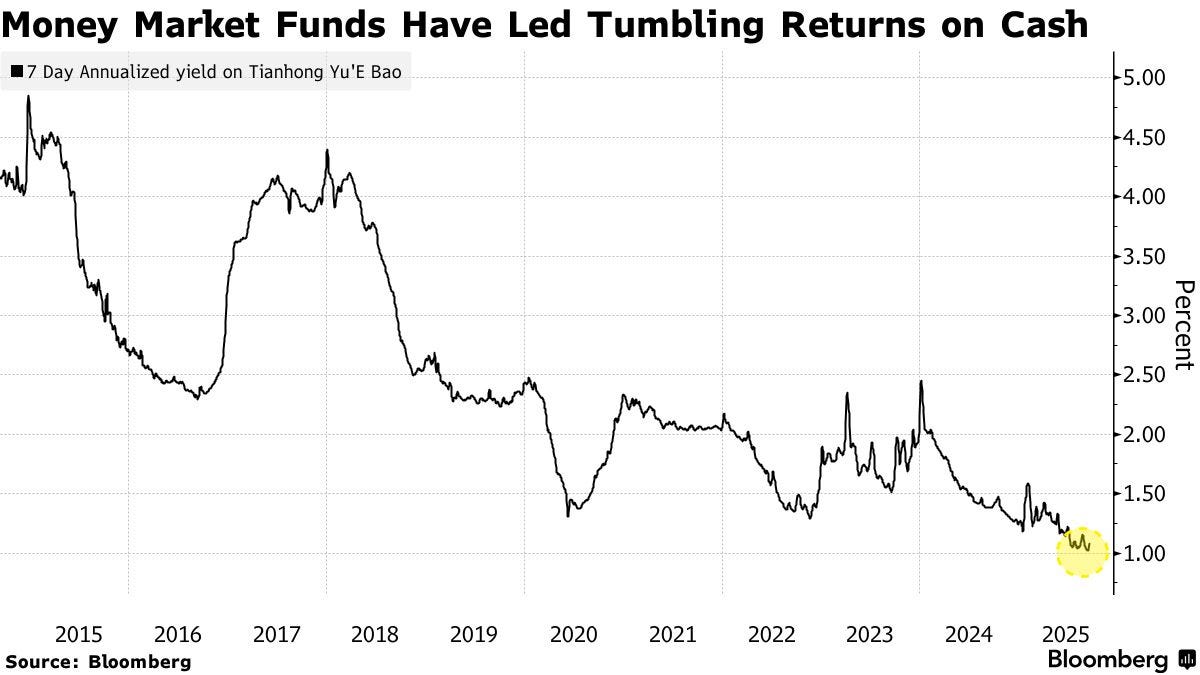

Chinese households are sitting on roughly $23 trillion in cash. That’s about the size of the country’s entire economy, parked in deposits that now yield close to nothing.

Property, the traditional store of wealth, is still healing. Sooner or later that changes behavior. People don’t stop seeking returns when the old playbook stops working. They simply look for a new one.

Even if just one percent of that pile rotates into equities, that’s over $200 billion of fresh buying power. Two percent is closer to half a trillion. You don’t need a flood to move the market. You just need a trickle from the biggest cash hoard on the planet.

The first destination for that money is broad and simple: dividend funds, big index sleeves, and Hong Kong shares of companies households already know from the A-share side. This isn’t a matter of preference, it’s inevitability. $23 trillion can’t just sit idle in accounts paying 1%. With property still shaky and bank deposits offering nothing, that capital has no real choice but to find a new home in financial assets.

And once the first wave goes in and markets start moving higher, confidence feeds on itself. People trust what’s working. A rising market attracts more local money, and that’s how you get something China hasn’t had in a long time—a rally that can actually turn into a sustained bull market.

Policy is helping this time too. Regulators are leaning into stability: slowing the IPO pipeline so supply doesn’t swamp demand, tightening insider sales so investors don’t feel like the exit is always jammed, and encouraging “market value management”—plain English for more buybacks, dividends, and cleaner disclosure.

It isn’t perfect, but it’s a far cry from the whiplash of past cycles. That alone lowers the left-tail risk that kept allocators hiding in cash.

The fundamentals don’t need to be spectacular. They just need to be believable. And across the bigger platforms, they are. Cloud and AI are showing up in the numbers. International commerce is becoming a real growth engine. Logistics networks are still humming. Costs are healthier because management is finally prioritizing what actually earns returns. Less “growth at any cost,” more focus and discipline. That’s exactly what you want while flows build: fundamentals that don’t undercut the tape.

Put it together and you get the tailwind of all tailwinds. A domestic savings glut that needs yield. A policy backdrop that wants a functioning equity market. And businesses that no longer contradict their own narratives. That’s real fuel. And unlike the hopium waves of the past, this one doesn’t need a miracle. It just needs time and fewer unforced errors.

If you’d like to support my work and get access to portfolio updates (what I’m buying and selling), deeper research, and more, I’d be grateful if you considered becoming a paid subscriber.

The structural change everyone missed: act like owners (and why this bull can have legs)

This is the tell that separates this bull run from previous (typically short lived) China bull markets. China’s biggest companies used to hoard cash and chase every adjacency in sight. Today, they’re acting like owners. Buybacks aren’t a stunt; they’re a standing order. Authorizations are big and actually used when shares are cheap. Dividends, once a “maybe,” are becoming policy.

Why does that change the game? Because capital return sets a floor and it enforces discipline. It also answers the question that kept so many investors on the sidelines: is the cash real? You don’t need a speech to prove it if you’re retiring shares every week and wiring dividends every quarter. Proof beats narrative.

Valuation still tilts the odds in your favor. Even after the bounce, you’re not paying pricey multiples for most of this. You’re paying mid-teens earnings for companies that are now returning cash, cleaning up their mix and continuing to grow.

You’re not buying perfection; you’re buying patience. And you’re getting paid to wait.

That’s why this can have real legs. There’s dry powder at home. There’s policy alignment. There’s a new habit of returning cash back to shareholders rather than lighting it on fire. The fundamentals are better than the Western headlines admit. The buyer base is sturdier and the underweights are obvious. If the dollar softens and rate cuts keep inching along, emerging markets get a tailwind.

But even without that, the domestic engine is enough to keep oxygen in the room.

Could it break? Of course. Policy could over-tighten. Geopolitics can always punch you in the mouth. Consumer confidence could take a detour. None of that is new.

The difference is the cushion. Buybacks and dividends compress downside in a way we simply didn’t have during the 2015 or 2020 runs. Back then, you owned hopes and charts. Today you own cash flows and fewer experiments. That HUGE.

How I’m handling it

I’m not trying to be a quant or pretend I’ve suddenly turned into a momentum trader. That’s not me. What I see in China right now doesn’t feel like another head fake. It feels like the beginning of a real cycle—one that starts with price strength but gets carried further by cash, policy support, and companies finally treating shareholders like owners.

I went long Alibaba and Baidu at the start of the year, and those calls have paid off. I’ve trimmed into strength, taken some profits, and shifted a good chunk into KWEB. If this rally turns into a true bull market, I’d rather have exposure to the whole tide than just a couple of boats.

That doesn’t mean I’ve changed how I invest. I still care about the same things: valuation, cash generation, and businesses that can compound over time. The difference now is that the tape isn’t working against me. Fundamentals and momentum are finally moving in the same direction, and when that happens the smart thing to do is let both do the heavy lifting.

The shareholder return shift is the key differentiator here. Previous China rallies collapsed because companies kept diluting shareholders with endless adjacencies and cash burns. If buybacks and dividends are now systematic rather than opportunistic, that changes the risk/reward calculus significantly. The $23T household savings rotation thesis is compelling - even 1-2% movement creates massive flows. Still, I'd want to see more evidence that the policy stability actually holds when markets get volatile.

Quite some number of Chinese American refuse to invest in US ADR Chinese stocks.

No reasons are given.

I don't know why.