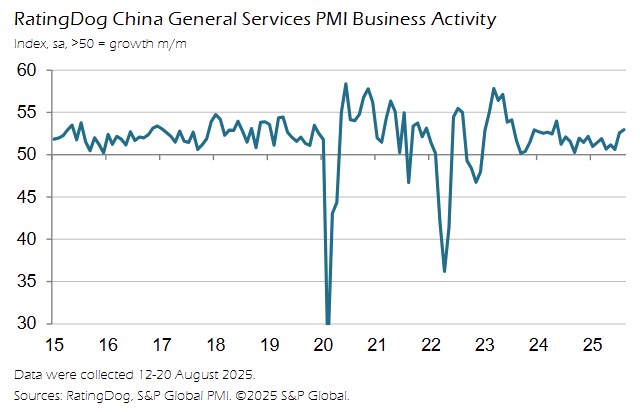

China Services PMI Hits 15-Month High

China’s services PMI for August came in at ~53.0, the strongest reading in more than a year.

Services now make up over half of the economy, so when they’re moving higher, it’s worth paying attention.

But I think it’s important to be mindful about what might be pushing it higher… A big part of the strength is almost certainly tied to the instant delivery war.

Alibaba, Meituan, and JD are basically tripping over each other to get anything you might want—food, groceries, medicine, electronics, you name it—to your door faster and cheaper than the rest. That arms race is pushing up activity levels, which PMI surveys capture, but it’s also eating into profits.

Subsidies are heavy, costs are rising, and margins get thinner the longer the fight drags on.

At the same time, there’s more happening here than just a subsidy-fueled delivery boom. Travel, restaurants and entertainment are all seeing real demand again. New orders are rising both at home and abroad.

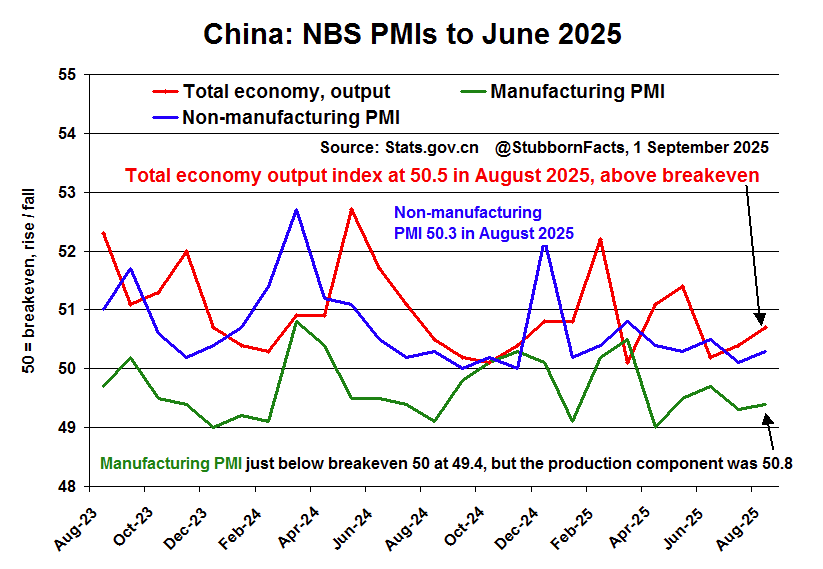

The problem is that manufacturing is still lagging. Factories have been in contraction for five straight months, so the recovery is leaning heavily on services while the industrial side stays weak. That doesn’t break the economy, but it does make the rebound feel uneven.

So where does that leave us? The latest PMI is encouraging because it proves demand is there, and it challenges the idea that China’s consumer story is finished. But it also comes with caveats.

The growth is real, the profits less so.

Worst case, this is just a sugar rush from instant delivery subsidies that fades once the competition cools. Best case, it’s the first real sign of a sustained rebound in services that helps offset weakness in manufacturing. Either way, the doom loop narrative doesn’t square with the data we’re seeing.

And stepping back, this is exactly why I remain bullish on China’s economy over the medium and long term.

Every recovery cycle has uneven patches, in this case, services pulling ahead while industry drags. But the bigger picture is that demand is alive, household spending is climbing back, and policymakers have shown they’re willing to keep leaning in with support. Trade-in subsidies, consumer vouchers, targeted stimulus—we’ve already seen the playbook, and I’d expect more of it as Beijing tries to lock in stability.

That combination of cheap valuations, an improving demand backdrop, and ongoing policy support is why I continue to think the China recovery story has much further to run.