China Stocks Are the Most Compelling Opportunity in Global Markets

It hasn’t been fashionable to be bullish on China. I get that…

The headlines have been loud, the sentiment swings have been violent, and there were stretches where it felt like the whole world had decided China was “un-investable”.

Even so, I stayed positive because the underlying story kept improving while the narrative stayed stuck in the past.

Back in September I wrote a post explaining why I thought China’s rally had real legs.

The takeaway wasn’t complicated. Even after a modest re-rating, the market was still trading at depressed multiples while the fundamentals, the policy tone, and corporate behavior were all quietly turning in a better direction.

Three months later, nothing about that view has weakened. If anything, the conviction is stronger.

This isn’t meant to retell the September piece. It stands on its own. But it’s worth building on it now because the story has continued to evolve the way I hoped it would.

China has kept outperforming. Sentiment has shifted from “don’t touch it” toward “maybe I shouldn’t ignore this.” Policy has leaned more supportive. And the large public companies are returning more capital through buybacks and dividends than at any point in recent memory.

Meanwhile, the United States has pushed into a place where index-level valuations assume a smooth AI super-cycle and a very gentle macro backdrop. The U.S. still has plenty to offer. It’s just that the part of the market lifting the index isn’t where the value is. It’s elsewhere.

I think the next few years will belong to China in a way that will surprise a lot of people.

And if I had to narrow the whole bet down to one stock, it would be Alibaba… but more on that in a bit.

Koyfin is the tool I use every day to compare financials, track valuation work, and pull most of the charts you see in this post. If you spend time digging into businesses, it’s a great platform to work from.

Coughlin Capital has a partnership with Koyfin, so readers get 20% OFF any plan using this link.

The Macro Picture

If you follow China through Western headlines, you have seen the same rhythm for months: soft PMIs, sluggish retail sales, ugly property data, etc.

Every release gets framed as proof that China is stuck in some permanent downward spiral.

I read those numbers differently.

Weak data in China does not play the same role that weak data does in the U.S. In the U.S., soft numbers can spook the Fed, tighten financial conditions, and hurt risk assets. In China, weak numbers are usually the trigger for more support. They are the justification policymakers point to when they ease.

There has been a lot of debate in the last two years about whether Beijing really wants to stimulate. You can see why that debate started. The focus from 2021 onward was on cleaning up excesses in property and internet platforms, not on juicing growth. That clean-up phase is mostly behind us now. The priorities are shifting.

I think over the next twelve months we are going to see more stimulus, not less. Not a 2009-style “flood the system” package, but a steady series of measures across credit, local government funding, and targeted consumption support. Some of this is already happening. Deposit rates keep drifting lower. Local governments are being given room to refinance. You see small but constant programs aimed at nudging spending in specific areas: green appliances, EVs, AI, rural upgrades, elder care, services.

This is where “Don’t fight the PBoC” comes in.

For years, the version of that phrase everyone used was “Don’t fight the Fed.” The idea was that if the U.S. central bank wanted financial conditions to loosen or tighten, it would usually get its way. In China today, the PBoC and the broader national team are playing a similar role for domestic assets.

When equity markets wobble too hard, you see state-related funds buying ETFs. When volatility spikes, you see signals from regulators and the central bank that they are watching and willing to lean against disorderly moves. There is a soft floor under parts of the market.

You can literally see it on a longer-term chart of the Shanghai Composite… it does not spend much time meaningfully below certain levels before support appears.

You do not need to believe in a hard put with a fixed strike price. It is enough to accept that policymakers now see stable equity prices as a useful tool. That changes the risk profile for investors.

In that context, weak macro numbers are not just bad news. They are the fuel for more easing. Bad data is what gives the PBoC and the national team cover to keep leaning into support.

That is exactly the environment where you want to be long equities, not short them.

The Consumer: Cautious, Not Broken

On the ground, the demand picture is mixed, but it is not the disaster story people like to tell.

Retail sales are growing at low to mid single digits. That is not a boom, but it is not a collapse either. The mix is changing in ways that make sense for a more mature economy. Households are spending more on services, travel, entertainment, health, and small luxuries. They are spending less on things directly tied to the housing boom.

You can see this in places like Hong Kong, which is heavily exposed to mainland tourism and discretionary spending. Retail sales have been growing again. Luxury categories are no longer being crushed. Visitors are coming back. This is not a picture of a consumer in hiding.

Confidence is not perfect. People are still cautious. Property has clearly broken the old wealth model. But the equity market does not need a euphoric consumer. It needs a reasonably stable consumer and companies that can take that stability and turn it into cash flow.

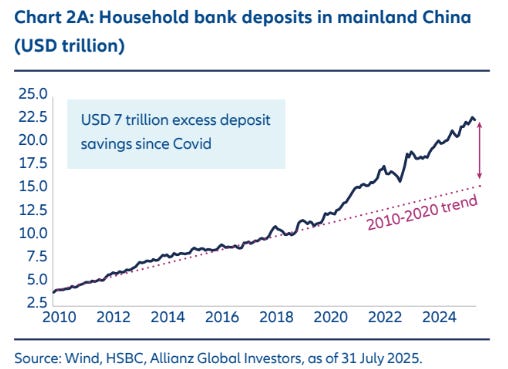

The other big piece is household savings. Chinese households still sit on an enormous pile of deposits built up over years and reinforced during Covid. Those deposits earn very little in real terms.

At the same time, listed companies are offering higher dividend yields and more consistent buybacks than at any other point in recent memory.

The gap between money in the bank and money in good Chinese equities is wide.