Cheap ≠ Interesting

Where I think the real opportunity is in payments

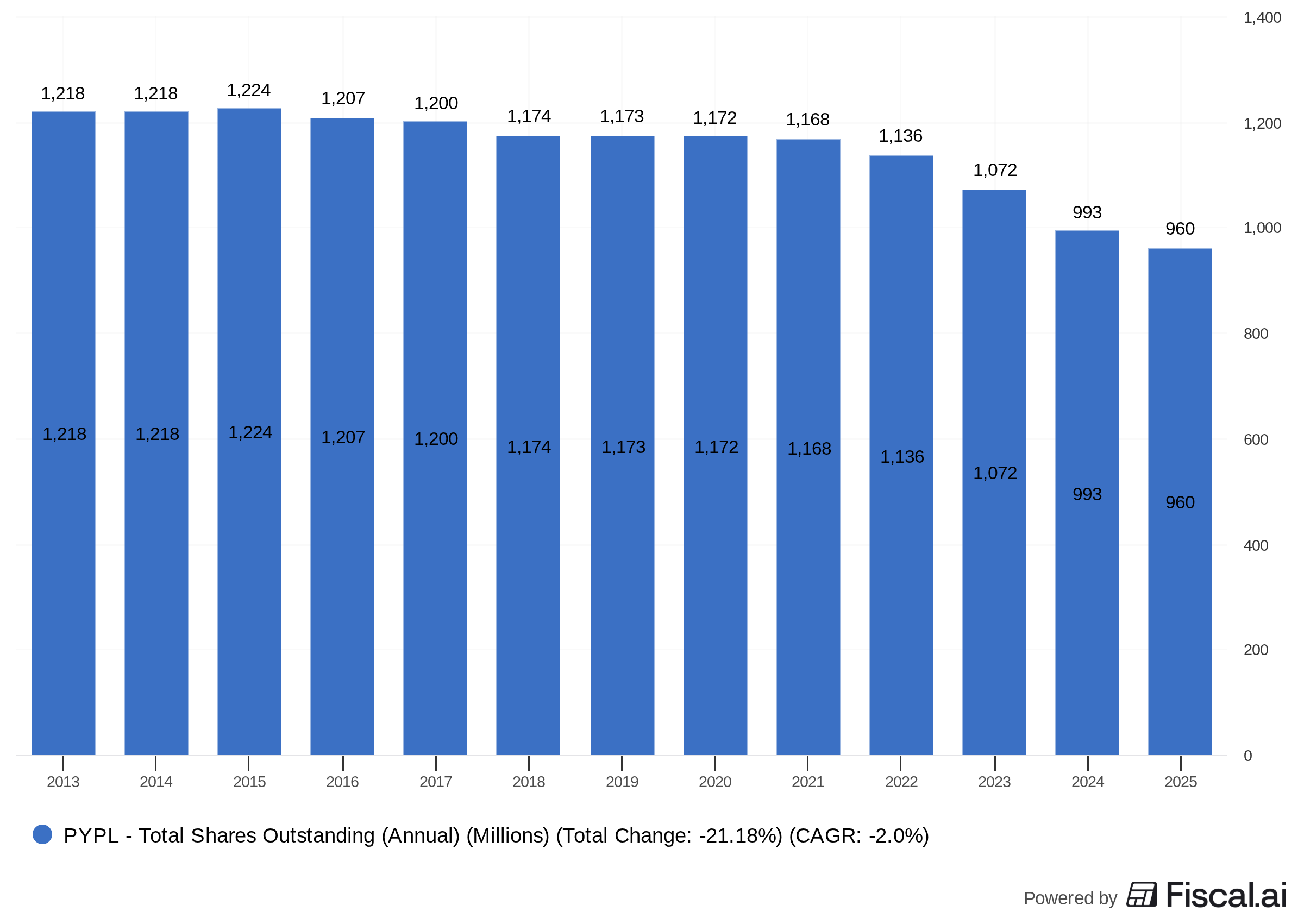

Lately I can’t scroll Twitter or Substack without running into another PayPal “deep value” pitch. The argument is always the same: it’s cheap, it mints cash, and management is retiring shares by the bucketload. And that’s all true. Forward P/E in the low teens, billions in buybacks, decent free cash flow. It checks all the boxes of a value screen.

But cheap is not the same as interesting. Cheap doesn’t automatically mean it’s the best place to park capital when the entire payments and fintech complex has come down to earth. If the whole sector has re-rated lower, then PayPal’s multiple isn’t the differentiator, it’s the business model. And the business model, to me, looks more like a treadmill than a compounder.

I get why people cling to it. The nostalgia factor is strong. PayPal was the original digital wallet. It had real brand power, Venmo became a verb, and for a while it felt like the de facto checkout button of the internet. But look around now. Apple Pay and Google Pay live in your pocket by default. Venmo has yet to turn into the monetization machine that bulls promised. And transaction growth has slowed to the point where management’s only lever is buybacks…

That’s not a disaster, it’s just not exciting.

When I think about where I want exposure in this space, I want businesses where growth is still obvious, not something I need to rationalize by talking about “financial engineering.” That’s where Adyen and Shift4 come in.

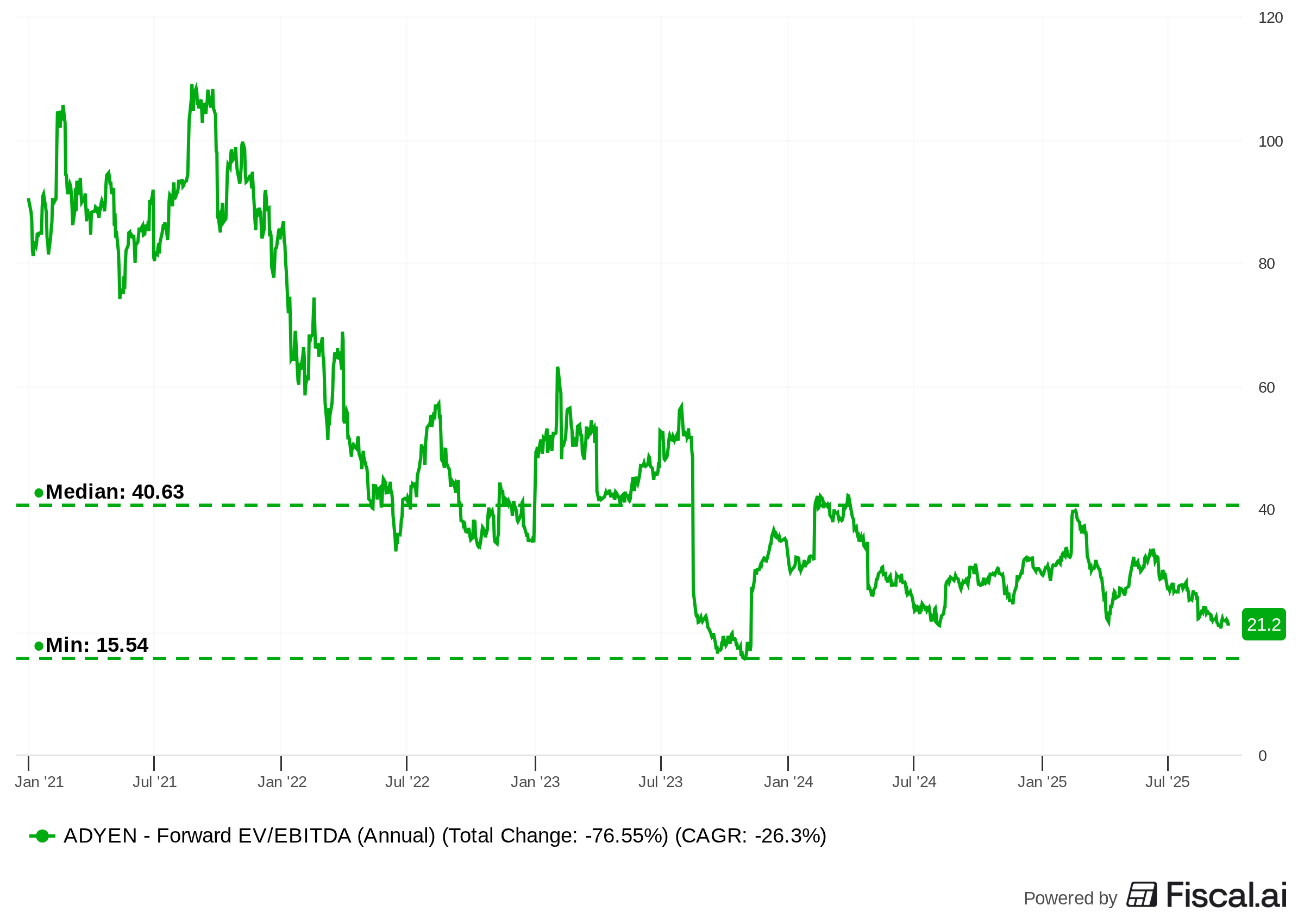

Adyen in particular is fascinating right now. For years, it was the name everyone admired from a distance. Best-in-class infrastructure, pristine balance sheet, enterprise customers locked in by global scale and a single codebase. The only problem? You couldn’t buy it without holding your nose at the multiple. That premium was deserved, but it kept me on the sidelines.

Fast forward to today, and Adyen is basically the cheapest it’s ever been as a public company. Not “cheap” like PayPal, but cheap relative to what it’s been historically—low 20s forward EV/EBITDA versus the nosebleeds it once commanded.

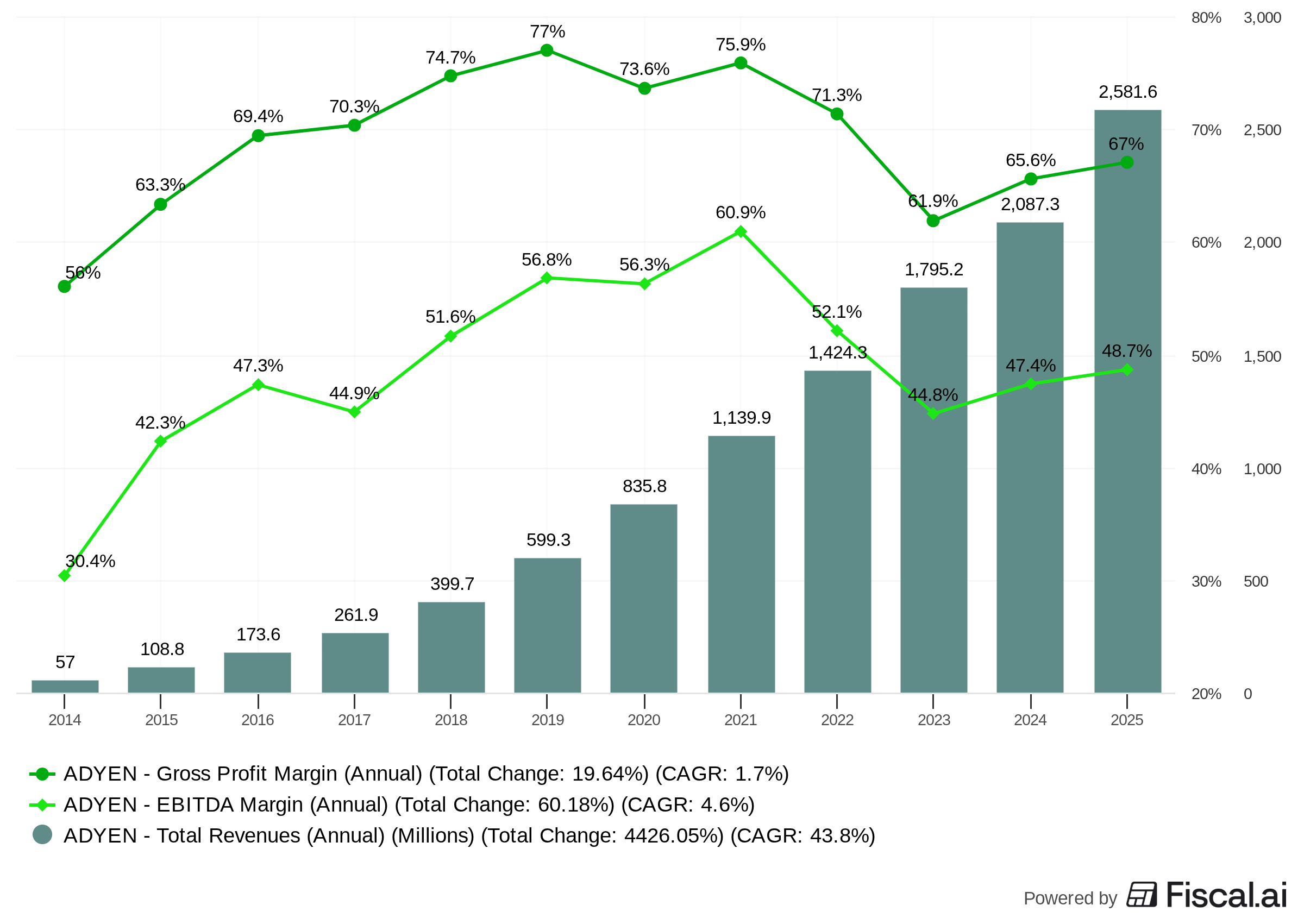

And the business itself hasn’t broken. If anything, margins have rebounded, free cash flow is humming, and the customer base is as entrenched as ever. It’s rare to see a quality compounder come down to “normal” valuation territory. When it does, I take notice.

Then there’s Shift4. I won’t rehash the full thesis here since I just posted a write-up a few days ago, but I'll link the full post below for those who are interested.

![[New Position] Shift4 Payments (FOUR)](https://substackcdn.com/image/fetch/$s_!PiaE!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F6bfbe39a-ee06-4b63-bb2f-30884fa4e88b_2048x1452.jpeg)

The quick thesis is fairly simple: dirt cheap for the growth it’s putting up. Founder-led, software-first, and deeply embedded in industries where switching costs are real. Restaurants, hotels, stadiums, entertainment venues. Not just another payments company, but a platform that keeps pulling more of the stack in-house. That’s why I opened a position. The market can keep labeling it however it wants, I’ll keep building while the multiple looks this low.

So when I see people pile into PayPal because “it’s cheap,” I can’t help but think they’re missing the point. Everything in payments looks cheaper than it did two years ago. The question isn’t “what’s cheapest?” It’s “what deserves my capital?”

PayPal has a future. It will keep buying back stock, posting solid quarters, and nudging guidance. It’ll work as a cash-return vehicle. But if Adyen is trading near the cheapest multiple in its history, and Shift4 offers a longer growth runway at an even lower multiple than PayPal, why would I settle for a company whose real growth years are already in the rearview?

That’s how I see it. PayPal is fine. But, the real opportunities in this space are elsewhere.

Adyen is choosing not to be super profitable right now but could do so if they wanted - i.e. get back to a low-60% margin in a hurry. It's a very attractive combination of growth plus margin expansion in reserve. Definitely looks more interesting at these levels.

Blue chip premium and moat. US vs Europe for Adyen and lower TAM and more cyclically for FOUR