Cash is King?

There’s a version of the future where this market is actually fairly priced.

In that version, AI changes the world faster than anyone thought possible. Productivity soars, margins expand, and the whole universe of AI-driven and software-heavy businesses actually grow into the valuations the market is giving them today.

The economy avoids recession, inflation fades away, and rates come down gently without breaking anything. Earnings explode and today’s prices don’t look expensive in hindsight—they look like a gift.

That version exists.

But betting on it feels like betting on a perfect game. Everything has to go right. And right now, the market is priced like it already has.

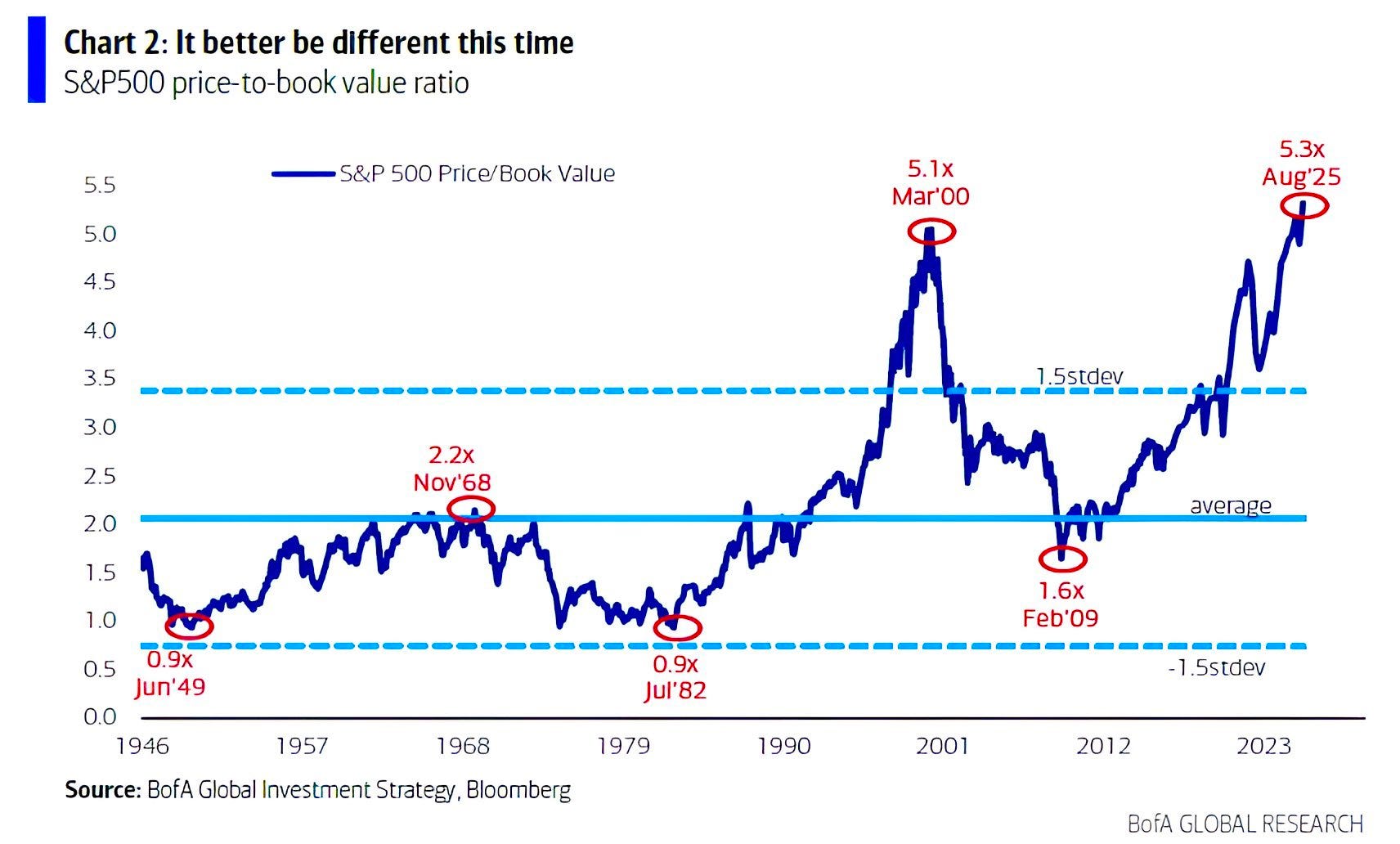

The S&P 500 is trading at 5.3x book value, the highest level in history. Higher than 2000, higher than any other cycle we’ve ever seen.

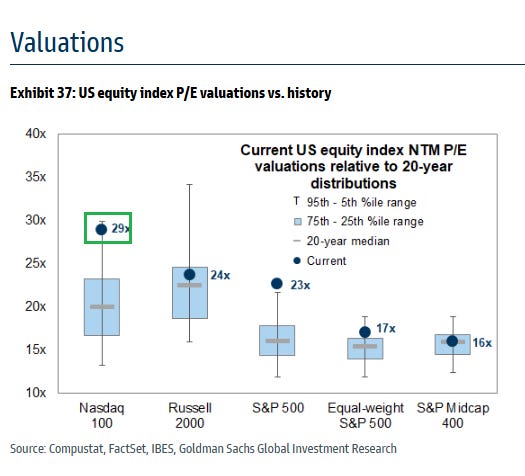

On earnings, the picture isn’t any better. The index sits around 23x forward earnings, and the Nasdaq 100 is closer to 29x. That’s not just above average—it’s pressing the very top end of the past twenty years of history.

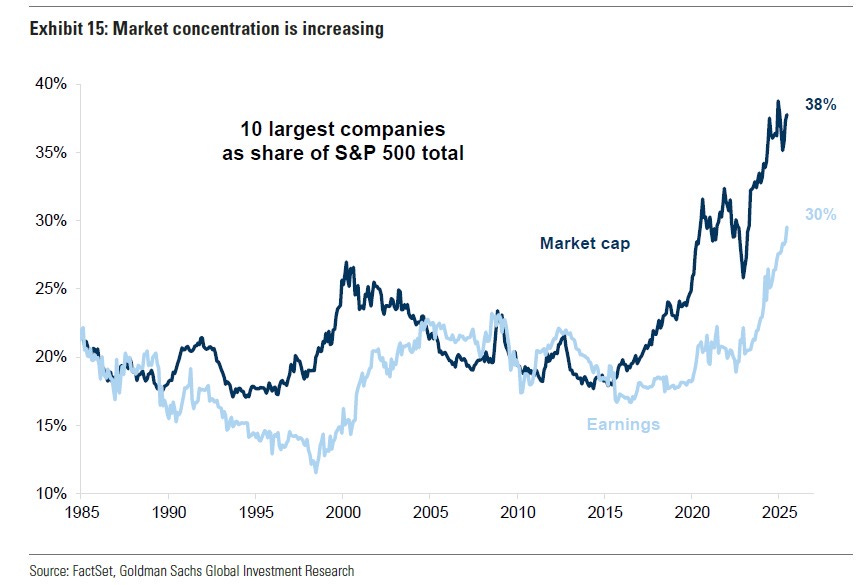

The bigger issue is that leadership is so concentrated. The top ten names now make up over a third of the index and trade at 30–40x earnings.

These are the biggest companies on earth, already valued at trillions. To justify those multiples, they’ll need massive, sustained growth from here. Maybe they get it. But if they don’t, the downside is significant.

AI is the story holding it all together. The idea is that chip demand never slows, monetization shows up quickly, and returns on all this capex justify the trillions already spent.

That could happen. But there are plenty of more ordinary outcomes too… over-ordering that leaves the industry with too much capacity, depreciation weighing on earnings, or adoption curves that take longer than hoped.

If even one of those plays out, these stocks don’t just miss by a little, they get repriced lower.

Meanwhile, everyone is already on one side of the boat. Hedge funds are long, retail money is back, passive flows keep piling into the same names, and volatility is near the floor.

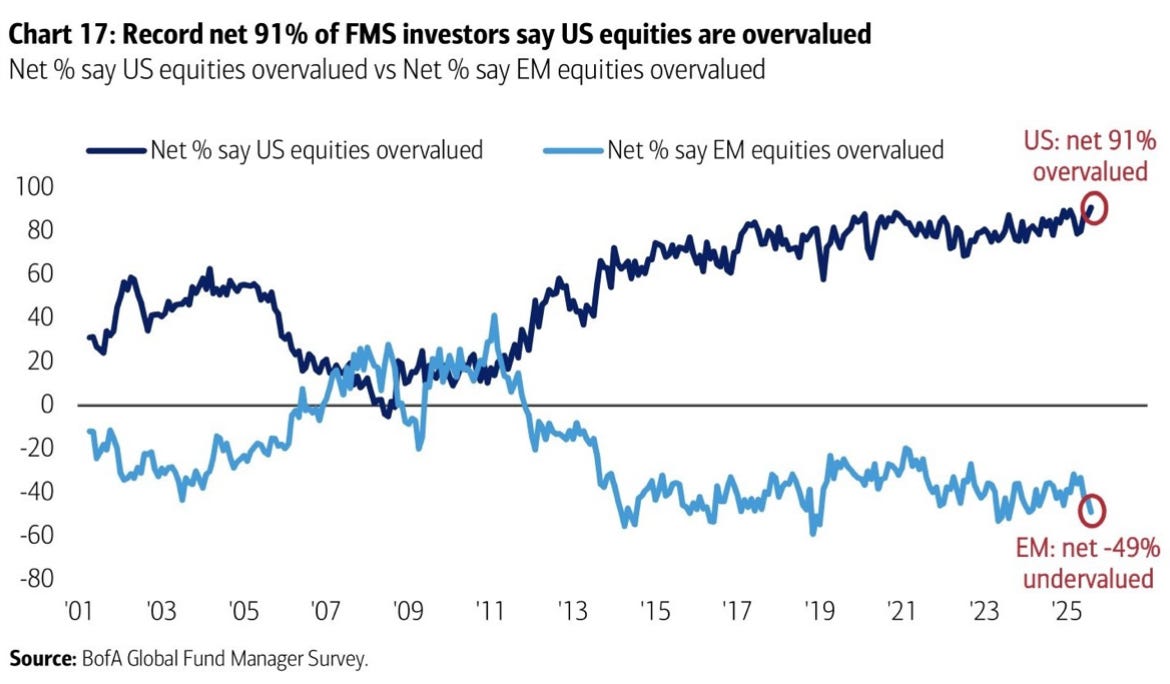

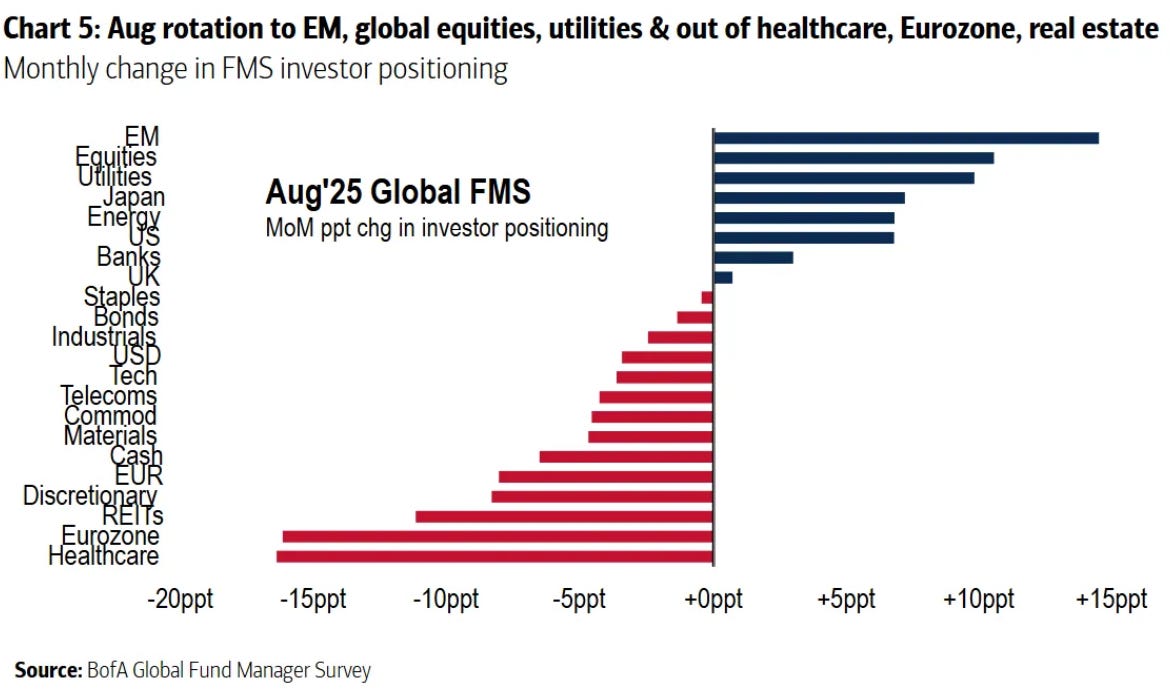

According to Bank of America’s survey, 91% of fund managers say U.S. equities are overvalued, the highest reading on record. At the same time, nearly half say emerging markets are undervalued.

That doesn’t mean the U.S. market has to crash tomorrow, but it does mean the crowd is leaning heavily one way. When sentiment is this one-sided, it doesn’t take much to shake confidence.

That’s why I keep at least a little bit of cash. Not because I think timing the market is possible, but because optionality has value. Dry powder matters when perfection is already in the price.

And this is where looking beyond the U.S. really matters. Because while U.S. equities are priced like everything has to go right, plenty of other markets are priced like they’re permanently broken. Emerging markets still trade around 14x earnings. China is closer to 12x.

Even sentiment is starting to shift. The latest survey shows fund managers finally rotating toward EM and Japan while trimming U.S. exposure. It’s a small move, but it’s there.

And when I look at the companies themselves, the gap between perception and reality in China feels as wide as I’ve ever seen it.

Alibaba is buying back stock aggressively, leading the country in AI and cloud, and trades at just 8x EBITDA. Baidu is closer to 5x with a fortress balance sheet. JD runs a profitable logistics network, yet the market values it like it’s on its last legs at 6x.

None of this requires a miracle. It just requires that the world doesn’t end. That’s a much easier setup than paying top dollar for the U.S. and hoping AI saves the day on schedule.

So yes, I think cash is king right now—but only as a tool. I want the flexibility to take advantage of mispricings. The rest of my capital is in places where expectations are already on the floor.

I don’t need a perfect game. I just need the world not to end. And that’s a setup I’ll take every time.