Burford and YPF — Judgment In, Upside Ahead

Unpacking the legal, political and financial implications of the YPF decision for Burford Capital.

Burford Capital has long been one of those stocks that divides investors. There are those who understand the model and trust management—and those who find it too opaque, too volatile, or simply too niche to bother with. Fair enough. It’s a business built around complex legal claims, often in foreign jurisdictions, where outcomes are unpredictable and value realization tends to be lumpy. It’s not the kind of company you can model quarter-to-quarter.

But every now and then, something happens that forces the broader market to take notice. That’s exactly what we just saw.

On June 30, U.S. District Judge Loretta Preska ordered Argentina to turn over its 51% stake in YPF to partially satisfy a $16.1 billion judgment—a case that Burford Capital helped finance nearly a decade ago. The market responded with a 20% rally in BUR shares. But even after that move, the stock simply returned to where it was a month earlier. That says a lot about both investor skepticism and the opportunity still on the table.

And to be fair, that skepticism hasn’t been entirely misplaced.

The YPF case has loomed over Burford for years—a high-profile, binary legal outcome that the market consistently treated as a long-shot. Even those of us who’ve followed it closely (and hold shares) saw it as a call option—known, but heavily discounted. Now, with a firm ruling in hand and a major legal hurdle cleared, it’s worth revisiting Burford as both a business and an investment.

Now feels like an inflection point for the business—and not just because of the court win. In the span of a few weeks, Burford cleared two of its biggest overhangs: one legal, and one political.

A Legislative Risk Removed—At Least for Now

Let’s rewind a bit.

In June, Burford sold off not because of any case development, but because of language buried in a Congressional reconciliation bill. Specifically, the Senate Finance Committee had included a 31.8% withholding tax on “qualified litigation proceeds.” The logic—if you can call it that—was to treat litigation finance the way the U.S. tax code treats contingency fees earned by lawyers. Burford’s management warned this would be devastating to the business and the broader industry.

Investors took the threat seriously. BUR fell from ~$13.50 to under $11 in a matter of days.

Then came the reversal. The Senate Parliamentarian ruled that the provision violated the Byrd Rule (a reconciliation constraint), and it was stripped from the final bill. When President Trump signed the “One Big Beautiful Bill” on July 4, the litigation-finance tax was gone.

But the market didn’t move much on that alone. The stock only started to rally days later, once the YPF judgment and turnover order hit the tape—a clear, high-stakes catalyst that re-priced the odds of recovery.

The market reacted quickly—but again, all that rally did was unwind the earlier selloff. There’s still no multiple expansion here, just a reversion to “fair” value.

The YPF Order: A Legal Turning Point

Burford first disclosed its backing of the Petersen and Eton Park claims against Argentina years ago. The argument: when Argentina nationalized 51% of YPF from Repsol in 2012, it failed to make a proper tender offer to minority shareholders, as required under YPF’s bylaws. Petersen and Eton sued. Burford financed the litigation in exchange for a portion of any future recovery.

Fast-forward to 2023: the court awarded the plaintiffs $16.1 billion, one of the largest judgments ever issued against a sovereign in U.S. courts.

Then, on June 30, 2025, the court ordered Argentina to transfer its Class D shares of YPF (representing approximately 51% of YPF's outstanding shares) to a global custody account at Bank of New York Mellon ("BNYM") within 14 days and to instruct BNYM to transfer those shares to Petersen and Eton Park within one business day.

The logic: the court had already found Argentina liable, and the shares in question were “used for a commercial purpose” under the Foreign Sovereign Immunities Act—meaning Argentina couldn’t shield them from enforcement.

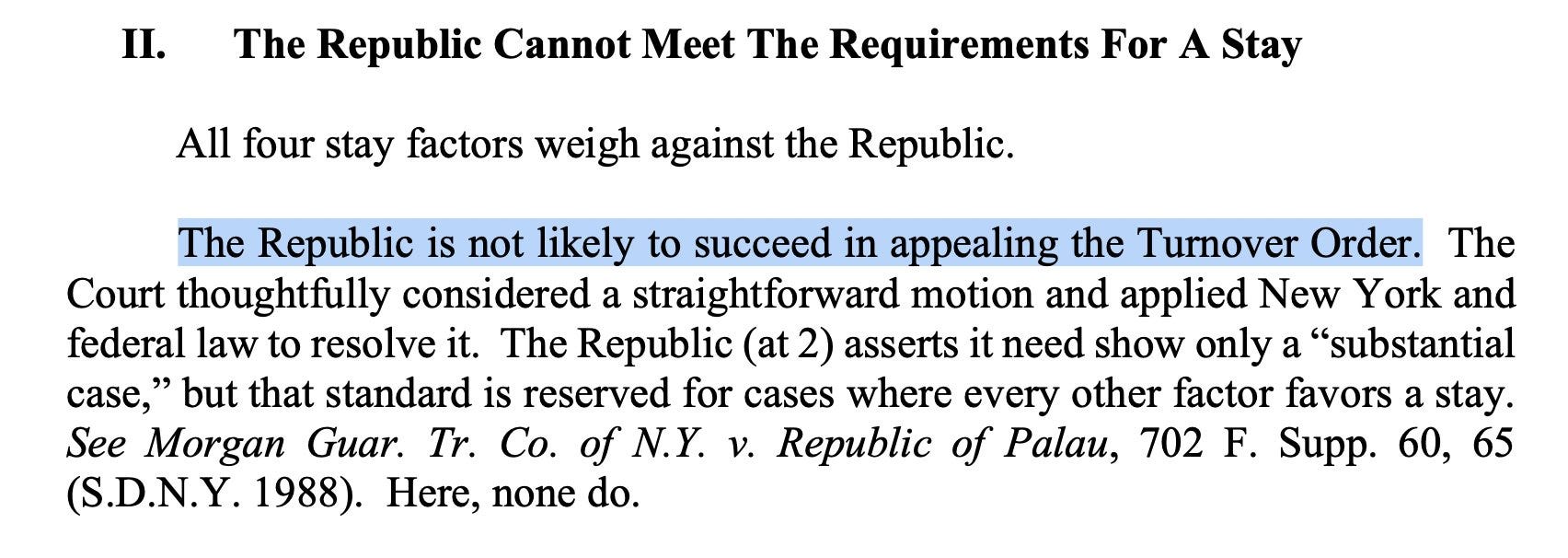

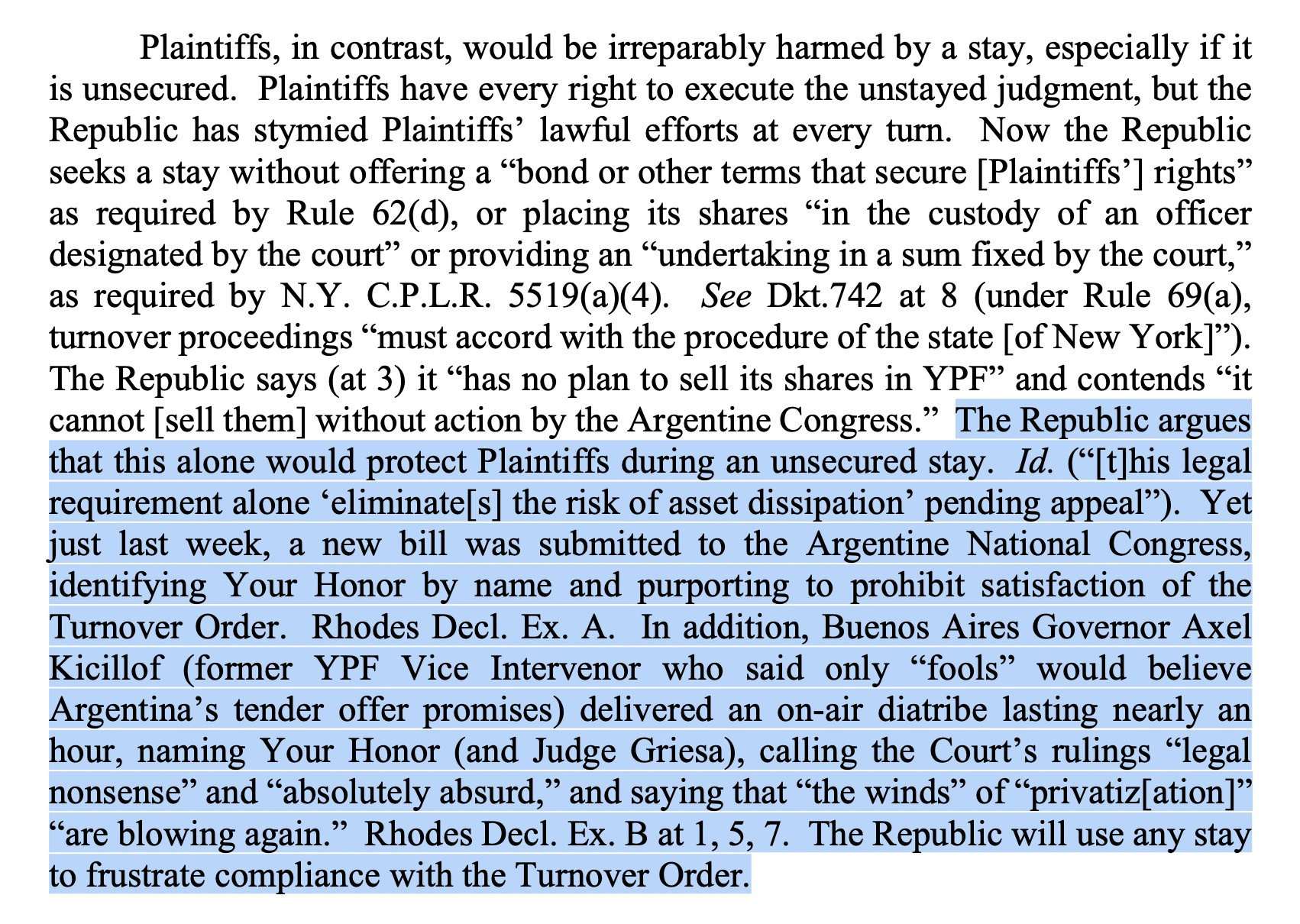

Argentina immediately appealed. But Preska’s follow-up opinion was unequivocal:

“The Republic is not likely to succeed in appealing the Turnover Order.”

The court also cited Argentina’s actions as justification for denying any stay. Just one week prior, Argentina’s Congress introduced a bill aimed at blocking compliance with the U.S. order. Buenos Aires Governor Axel Kicillof—who was deeply involved in the original YPF takeover—delivered a live on-air rant calling the court’s decision “legal nonsense” and warning that “the winds of privatization are blowing again.” The court wrote:

“The Republic will use any stay to frustrate compliance with the Turnover Order.”

For a market that has treated the YPF claim as theoretical—at best—this was a clear signal that enforceability is no longer just a hope.

Turning Judgment Into Value

Burford has disclosed that it holds a non-controlling contractual interest in the Petersen and Eton Park claims. The company expects to receive somewhere between 35% and 73% of net proceeds, depending on a range of factors—including enforcement costs, third-party entitlements, and how the recovery is ultimately structured.

Assuming a midpoint estimate (~55%), Burford could stand to collect $8–9 billion from this case—against a current market cap of roughly $3.5 billion. Of course, that’s not revenue the company can recognize today. Timing will depend on whether Argentina negotiates a settlement or pushes the appeal further. Enforcement may still take time—but the probability of real recovery has now materially improved.

And that’s the key shift: for years, this case was treated by the market as either permanently delayed or unlikely to ever pay out. That’s no longer the base case. Investors now have to seriously consider the possibility that Burford sees a multi-billion-dollar windfall in the coming quarters.

The Bigger Picture: A Win for Litigation Finance

While YPF is a milestone for Burford, it also marks a moment of broader validation for the litigation-finance model.

A U.S. federal court has just enforced a multibillion-dollar claim against a sovereign state. That alone will send a message to plaintiffs, counterparties, and governments alike. It shows that litigation funding—when done right—can level the playing field in cases that would otherwise be too large or politically sensitive for a traditional legal process to resolve cleanly.

Still, the model isn’t without friction. The political risk hasn’t disappeared. The tax scare in June was narrowly avoided, but it could return in future budget cycles. Representative Darrell Issa’s proposal to mandate disclosure of all litigation-finance agreements is still on the table—an idea that could make deal terms more public and potentially weaken Burford’s negotiating leverage in future cases.

Burford operates in a space that blends legal nuance, financial structuring, and geopolitical exposure. That’s part of what makes it interesting—but also inherently difficult to value. The cash flows are real, but lumpy. The outcomes are asymmetric, but binary. You don’t need to model it precisely to understand the appeal—you just need to understand how the incentives align.

Why I’m Still Holding

I’m still holding my position in Burford. I’m roughly break-even at current prices, but I think the setup looks better now than it has in a long time. The YPF ruling isn’t the end of the story, but it’s the clearest sign yet that this case is moving toward resolution—and that Burford’s approach works in even the most complex, politically charged environments.

The stock still trades cheap relative to the optionality embedded in its case portfolio. Litigation finance is maturing, and Burford remains one of the few public vehicles with scale, judgment, and a real track record. So long as they continue securing enforceable judgments and allocating capital wisely, I think there’s still significant upside ahead.

It’s a complicated business, no doubt. But complexity is often where the best opportunities live—and Burford continues to prove it can navigate that terrain better than most.

any chance for a detailed public update? have only seen one other since summer 2025.

milei fanboyz have fled despite trump's megaloan to argentina. however, not a great time in america to appeal for theft of foreign oil assets.