Big Tech Is Becoming Big Utility

Big tech as big utility. I’m not sure the market is ready for what that looks like.

There’s obviously a lot of debate right now around AI and capex and I’m sure most of you already have an opinion one way or the other. But it’s something I’ve been thinking a lot about, so now it’s my turn to share my thoughts.

For years, the bull case for these companies was as simple as it gets. High margins. Capital light. Incredible cash flow generation. You paid a premium multiple because these companies printed money without needing to spend much to do it.

Thanks to AI and the never-ending need for compute, that story is changing.

These businesses are fundamentally different than they were even two years ago. When you look at them today, they look a lot more like utilities. And because of that increased capital intensity, I don’t think we should be valuing Big Tech the way we used to.

It just doesn’t make sense anymore.

The Ever Increasing Spend

First, let me just lay out what happened in the last few weeks of earnings. Because the numbers are kind of staggering.

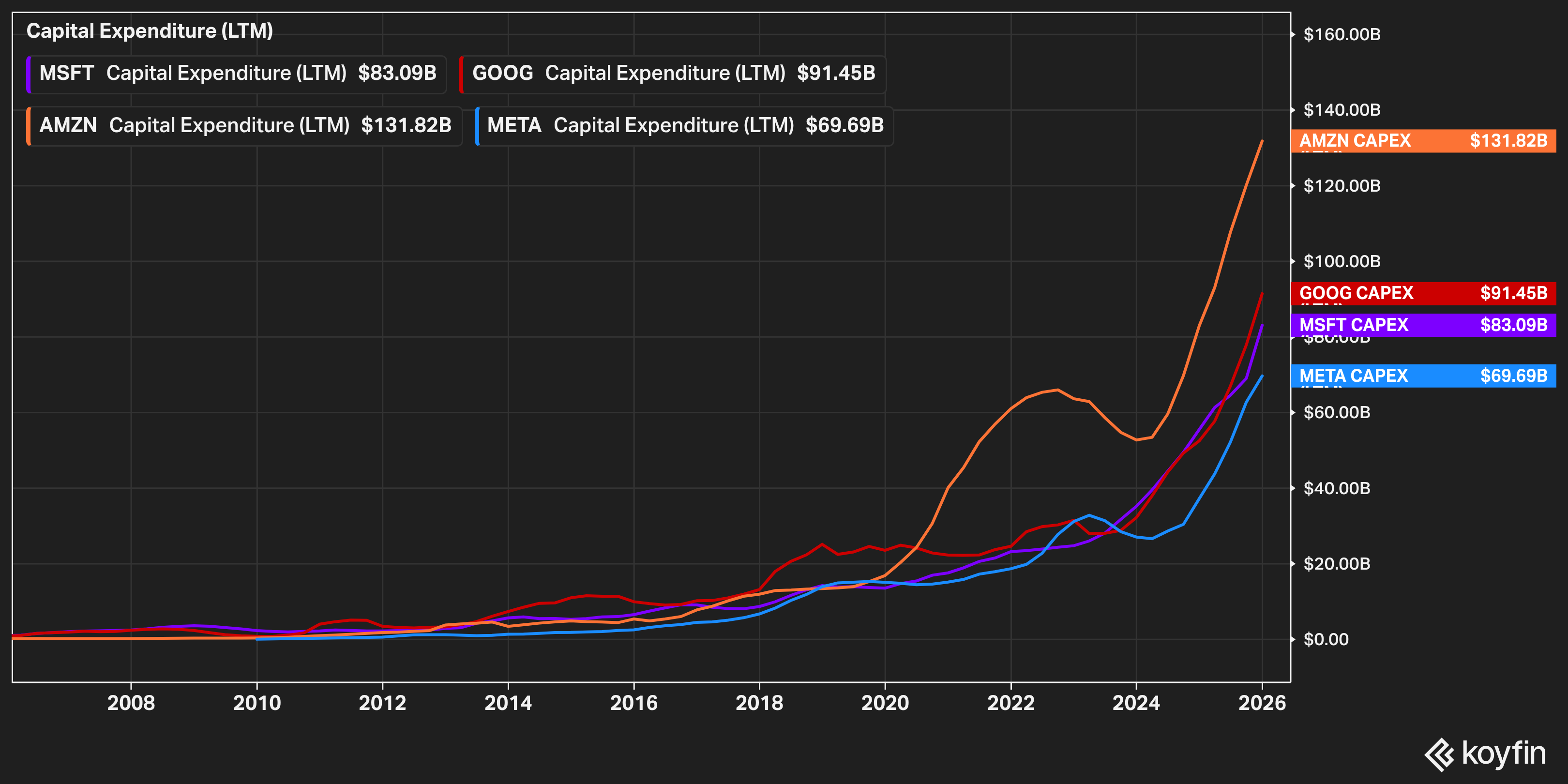

Amazon guided 2026 capex to roughly $200 billion. The Street was expecting about $146 billion. Amazon’s trailing twelve month free cash flow had already fallen to $11.2 billion, driven almost entirely by a $50.7 billion year-over-year increase in property and equipment purchases. Morgan Stanley now projects Amazon’s free cash flow goes negative this year. Negative.

Alphabet guided $175 to $185 billion. The Street was at $119 billion. That’s roughly double what they spent in 2025 ($91 billion) and more than triple 2024 ($52.5 billion). Analysts project Google’s free cash flow could fall almost 90% this year, from $73 billion to about $8 billion.

Meta guided $115 to $135 billion, up from $72 billion in 2025. A 74% increase. In 2021, Meta spent $19 billion on capex. Now the midpoint of their 2026 guidance threatens to consume nearly all the free cash flow their ad business generates.

Microsoft spent $37.5 billion in a single quarter. Two thirds of that on short-lived assets like GPUs and CPUs. Free cash flow for the quarter was $5.9 billion, down sequentially. Analysts are penciling in north of $105 billion for the full fiscal year.

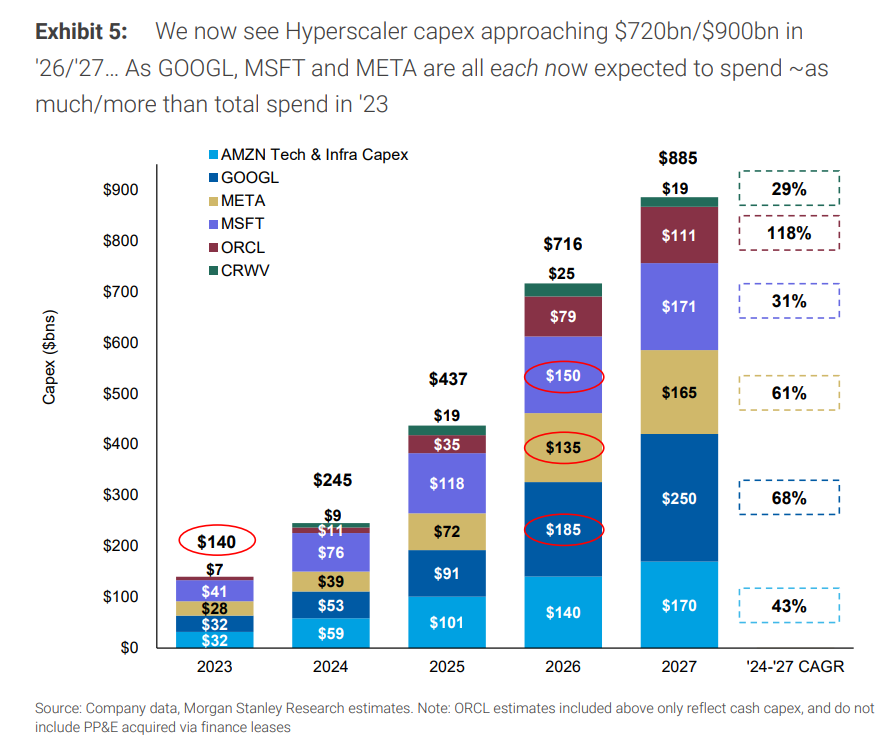

Add it all up and the four hyperscalers are expected to spend roughly $650 billion combined in 2026. In 2023, that number was roughly $140 billion.

$140 billion to $650 billion in three years…

The market kind of had a mixed reaction to these reports…

Meta’s stock popped 10% after earnings despite the capex guidance being above expectations. Alphabet initially dropped 7% after hours when the capex number hit, but then recovered almost entirely during the earnings call and closed basically flat the next day. The stock is still sitting near all-time highs, up about 70% over the past year.

Amazon and Microsoft? They got hit and stayed hit.

I think the market reacted the way it did because Meta actually paired the spending with a massive revenue beat and 30% forward guidance. Alphabet posted 18% revenue growth, Cloud accelerated to 48% growth, and net income was up 30%. Both companies showed up with the receipts. Amazon and Microsoft handed you a promise and asked you to wait.

The market is telling you something right now. If you’re going to spend like crazy, you better show me the growth right now. Not next year. Not “over the long term.” Right now. And the stocks that could do that got a pass. The ones that couldn’t got sold.

I think that reaction is more instructive than any analyst note you’ll read this week.

The Quality of the Earnings Is Changing

So why does this matter for how you value these stocks?

The reason big tech traded at 30x, 35x, 40x earnings for years was because of what the earnings were. They were clean. Capital light. A huge percentage of every dollar in revenue converted to free cash flow. That’s what justified the premium. Not growth alone. The quality of the earnings.

That quality is deteriorating.

A company that converts 30% of revenue to free cash flow and a company that converts 2% of revenue to free cash flow are not the same type of investment. They shouldn’t trade at the same multiple. Period.

And I want to be clear: this applies to Meta and Alphabet too, even though the market is treating them like the winners right now.

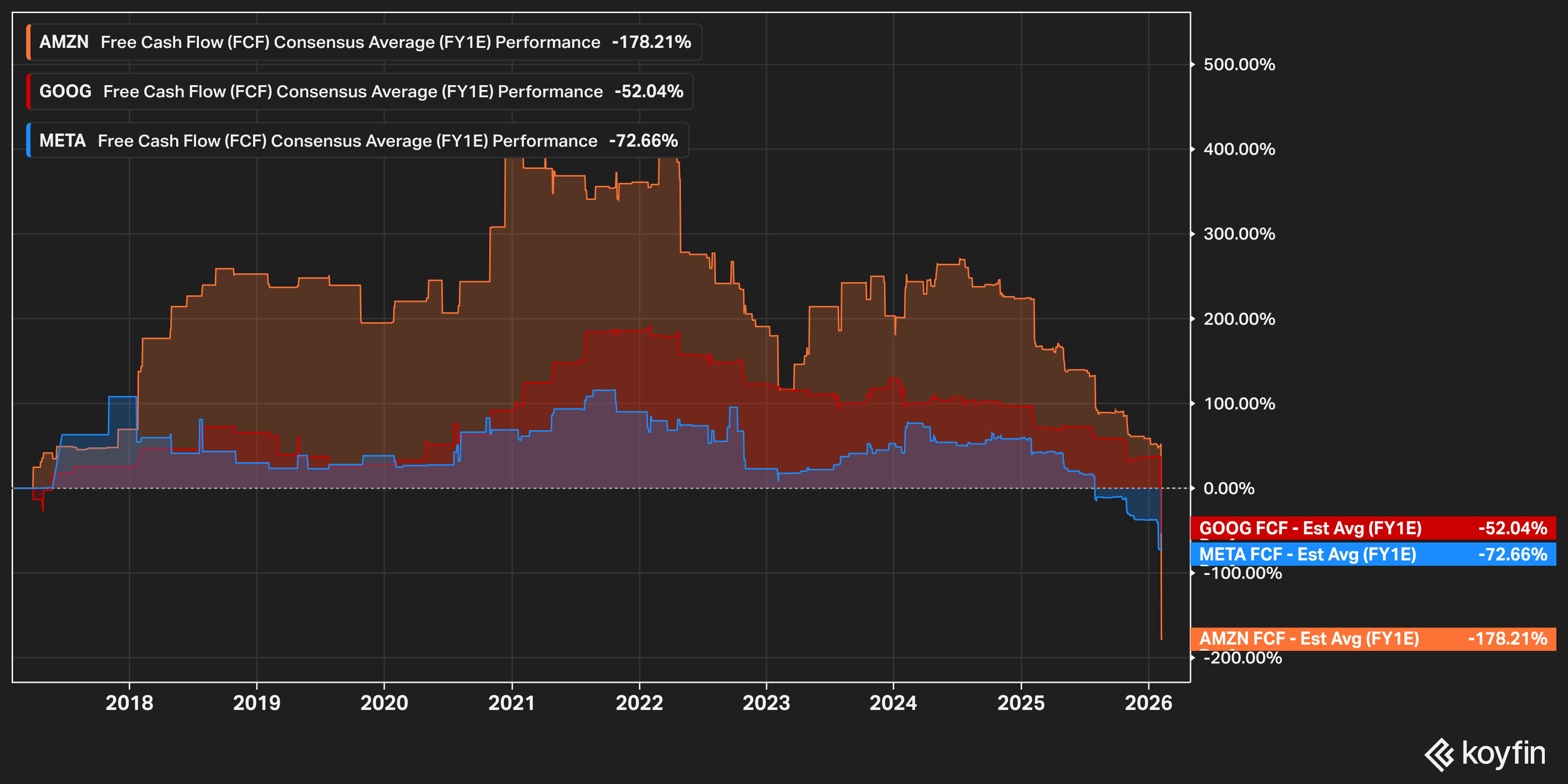

They’re getting a pass because they showed the revenue growth to go with the spend. That’s fair in the short term. But their free cash flow profiles are still deteriorating. Meta’s capex guidance threatens to eat nearly all the cash their ad machine generates. Even Alphabet, for all its Cloud momentum, saw free cash flow basically go flat year-over-year despite operating cash flow growing 34%. The capex is swallowing the gains.

The market can reward the growth today, but the math hasn’t changed. These companies are converting less and less of their revenue into cash that actually belongs to shareholders. A lower FCF conversion rate means a lower multiple. Eventually that catches up.

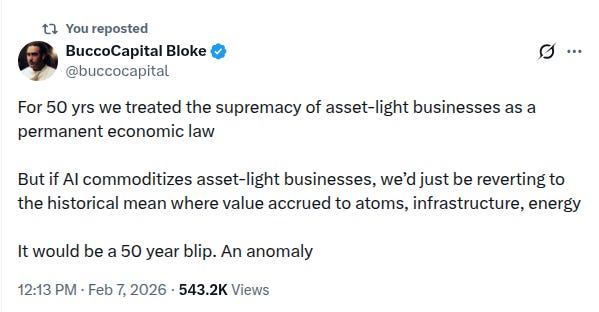

And this might be bigger than just a valuation question. Bucco Capital tweeted something the other day that really stuck with me:

Read that again. Because if he’s right, then the premium multiples the market assigned to big tech weren’t a reflection of some permanent truth about these businesses. They were a reflection of a specific era. An era where software scaled infinitely, marginal costs were near zero, and every dollar of revenue practically fell straight to the bottom line. That era might be ending.

What are these companies actually doing right now? Spending every penny they can find on chips and data centers…

Alphabet’s CFO specifically flagged that depreciation growth is going to accelerate meaningfully. That’s not how a software company talks. That’s how a utility talks. And utilities trade at low-to-mid teens multiples for a reason. They’re good businesses. Steady cash flows, essential services, long runways. But they require constant reinvestment just to maintain their infrastructure. The market doesn’t give you a 35x multiple for that.

And unlike software, where you build it once and it scales forever, AI infrastructure has a treadmill problem. GPUs depreciate at roughly 20% per year. You’re not building an asset that lasts decades. You’re building something that needs to be replaced in a few years. The capex doesn’t stop. One estimate I saw suggested the hyperscalers face an annual depreciation expense of $400 billion by the time they add $2 trillion in AI assets to their balance sheets by 2030.

That would be more than their combined profits in 2025.

Now look, these companies have over $420 billion in cash and equivalents combined. Cloud backlogs are enormous. Alphabet’s backlog doubled year-over-year to $240 billion. AWS revenue is reaccelerating. Microsoft’s commercial remaining performance obligation is at $625 billion.

Demand is obviously real. Nobody is arguing that people don’t want AI compute. The question I’m raising is whether the economics work at this scale when four companies are all racing to build the same thing at the same time. Competition compresses returns. We’ve seen that before.

And there’s a debt angle that I think people are sleeping on. Historically these companies funded everything internally. That’s changing rapidly…

Google quadrupled its long-term debt in 2025 to $46.5 billion. Amazon’s SEC filing explicitly mentioned it may seek to raise equity and debt. Meta has been burning through their cash pile and total debt has ballooned to nearly $100 billion. When companies that never needed outside capital start tapping the debt markets, pay attention.

Where This Leaves Us

I’m not short these names. I’m not telling anyone to sell. These are still incredible businesses with massive advantages. But I think the era of paying 30x, 35x, 40x earnings for Big Tech is probably over.

For the past decade you could buy these stocks and not think twice. These were businesses that converted 30 cents of every dollar into free cash flow. You didn’t need to overthink it. And honestly even if you never bought a single share of Microsoft or Meta, you still benefited.

The S&P 500 is nearly 40% these names. The top 10 stocks, almost all of them Big Tech, make up more of the index than the bottom 400 combined. Your 401k compounded the way it did in large part because these companies printed cash without needing to spend much to do it.

And I guess my concern is that the new version of this trade just doesn’t look as good. You’re buying these stocks and hoping $700 billion in annual spending eventually generates returns, waiting a few years to find out, and accepting that a big chunk of the cash these businesses used to generate is getting plowed back into depreciating infrastructure.

That’s not just a problem for people who own these stocks individually. When 40% of the index is changing what it is, that’s everybody’s problem.

I think the market is starting to figure this out, even if it hasn’t fully priced it in yet. Microsoft is down nearly 20% from its highs. Amazon has dropped from over $250 to $200. Meta and Alphabet are the relative winners despite planning to spend a combined $300 billion on capex this year, and I think that tells you everything about what the market cares about going forward.

It’s not about who spends the most. It’s about who can show you the revenue to justify it.

But even the winners have CEOs on every call saying some version of “we see enormous demand” and “we anticipate strong returns on invested capital over the long term.” Long-term is doing a lot of heavy lifting in that sentence. If the payback period is 5 to 10 years and the assets depreciate in 3 to 5, the math gets uncomfortable.

Ultimately, the point I’m trying to make is I think Big Tech multiples need to come down to reflect what these businesses actually are now, not what they used to be. Maybe not to utility levels, but the direction is clear. And if you’re still valuing these companies like they’re capital-light software businesses, I think you’re using an old map.

Big tech as big utility. I’m not sure the market is ready for what that looks like.

Disclaimer: I’m just one investor thinking out loud. This isn’t financial advice. I may or may not own positions in the names mentioned. Do your own work before buying or selling anything.

Hey Brian, really interesting article!

One thing came to mind while reading it. Right now, we’re basically in the middle of a situation where no one really knows how it will play out. There are several leading AI companies competing in a race and even experts don't know who will actually win. At the same time, there are quite a few businesses whose models could be disrupted or at least see pressure. And again no one really knows how this will evolve.

So the investors are picking one side and betting on one of possible outcomes.

But what if we would just say that we don’t know how this will end and choose not to invest in this space at all. I mean, there are so many great companies outside of AI and SaaS.

Don’t get me wrong, I think there are great opportunities in the AI space and chances for huge returns. But if the outcome is that uncertain imho it starts to feel a bit like gambling.

I think it all depends on what the return on the spend is.

If it's at or below cost of capital, then it is certainly a terrible investment and the shares deserve to be priced as such.

However if the Capex spend is generating multiples above the cost of capital, then it's value creative for shareholders. Speaking specifically about META, from 2020 - 2025 it's ROIIC for the entire period was 24.4%, and that's considering the invested capital base increased $228 billion over the entire timeframe.

Regardless, as a META investor, if they can generate ~24% returns on capital then I want them to make those investments all day every day.

Will ROIIC compress? Maybe, although if the hardware spend continues to fuel software growth and creates competitive advantages, then spend baby spend, so long as the return is above the cost of capital.

The other thing the investor needs to consider too is - is this growth capex versus maintenance capex? If it's growth capex then FCF should rebound and FCF margins should recover once the capital spend ceases.

If it's maintenance capex then that's a bad thing and the investor should not expect FCF margins to recover.

The infrastructure build out and model development is heavy upfront, but then once built, the data centres require power and that's about it to run. Although the useful life of chips is depreciated over ~4-6 years, it's not uncommon for many of the GPU clusters to have a useful life of 7+ years.