Baidu (BIDU): A Return to Growth?

Maybe boring search isn’t so boring anymore

I’ve been thinking about Baidu a lot lately. Not for the usual headlines about AI breakthroughs or their robotaxi ambitions, but for something far less glamorous—and, in my view, potentially more impactful to next week’s earnings—the state of their core business.

Baidu’s bread and butter is still search and performance marketing, and the Baidu App (which bundles search, news, and other content) is the primary front door. It doesn’t get the same attention it used to. It’s not flashy, and it certainly doesn’t enjoy the hype cycle that large language models or robotaxi’s do. But it’s still the engine that pays the bills.

And in the last few months, the environment for that business has started to look a lot healthier.

For more on why I like Baidu longer-term, here’s a post I wrote a while back:

China’s digital ad market has quietly been picking up steam. QuestMobile’s Q2 data shows internet ad spend hit roughly RMB 200 billion, up 6.8% year-on-year.

Budgets are getting bigger too, with more than a third of “hard” ad buyers (search, display, video pre-roll) spending over RMB 10 million in the first half. And June alone, thanks to the 618 shopping festival, accounted for nearly 18% of all H1 ad spend from traditional advertisers. That’s a lot of money chasing attention.

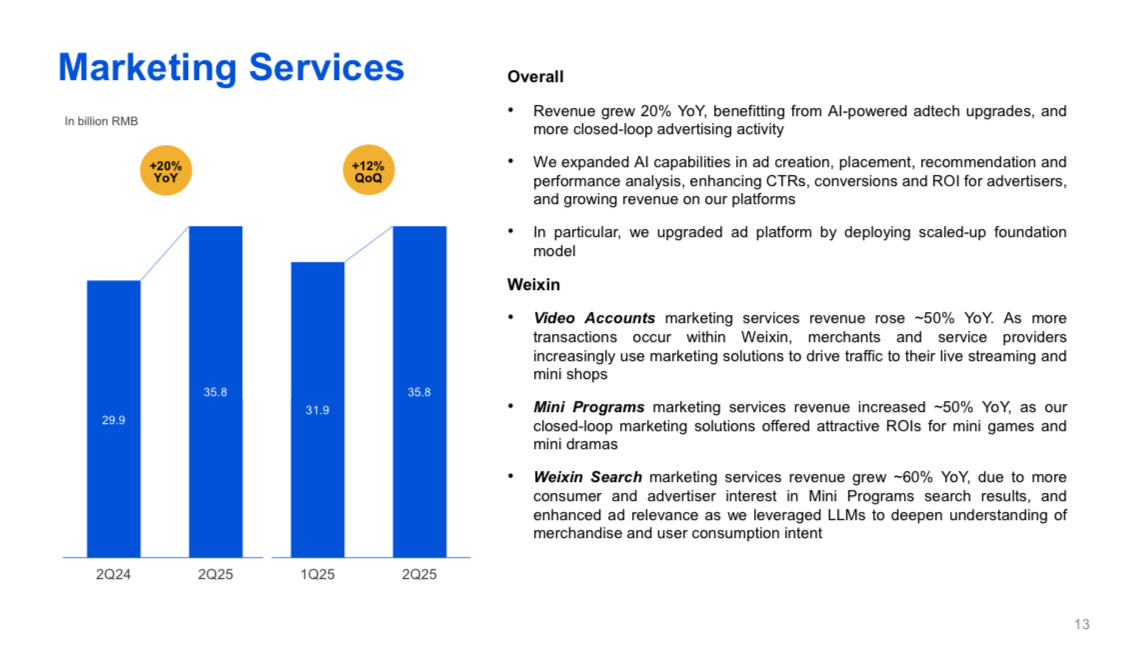

We got an early read on where some of that spend landed when Tencent reported. Marketing services revenue was up 20% from a year ago to RMB 35.8 billion. Video Accounts and Mini Programs, which are prime ad real estate for e-commerce promotions, saw revenue jump about 50%.

That’s insane growth for a company of Tencent’s size.

You don’t get that kind of growth at that scale unless two things are true: advertisers are spending aggressively, and the broader economy isn’t as dead as everyone thinks.