Baidu (BIDU): Still Too Cheap?

A lot going on here and the market doesn’t seem to care.

Baidu first caught my eye in late 2024 because the stock was stupid cheap and nobody cared.

At the time, Baidu had something like $30 billion in market cap with $27 billion in net cash and equity stakes sitting on the balance sheet. You were basically getting paid to take the operating business for free.

I wrote it up, laid out a sum-of-the-parts, and the conclusion was very, very simple: even if you were deeply skeptical about AI, robotaxis, and everything else management was pitching on conference calls, the math didn’t require any of it to work…

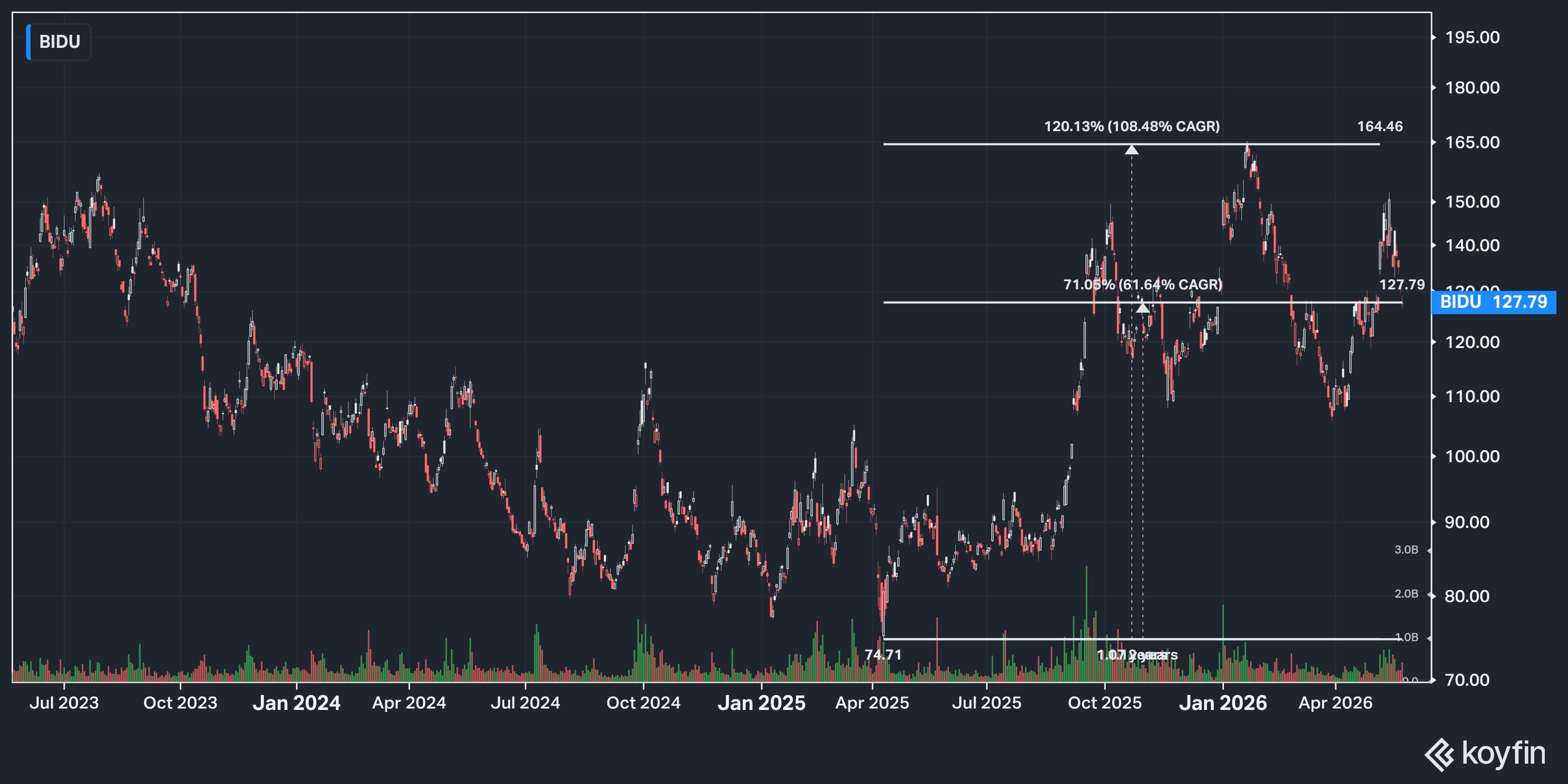

The stock has roughly doubled since then. The original cheap-stock pitch has mostly played out and the “easy” money has been made.

But the business has also gotten more interesting, which is why I’m writing about it again. And most of that comes down to Kunlunxin.

Kunlunxin is Baidu’s chip subsidiary. I mentioned it last year but honestly I didn’t spend much time on it. It was making AI chips for Baidu’s own data centers, which was fine, but it wasn’t a real business yet.

It didn't stay that way for very long. Kunlunxin is now pursuing a dual-track IPO in Hong Kong and on Shanghai’s STAR Market with a reported target valuation of at least $14.7 billion. Jefferies has the range at $16-23 billion.

I completely missed this, and I think it’s a good example of why buying stocks trading around net cash (even in China) tends to work out. You were sitting on free call options all over the business. Kunlunxin was one I didn’t even know I had.

So I want to spend most of this post trying to actually think through what the chip business could be worth and what that means for Baidu’s valuation today.

They just reported Q1 earnings though so I guess we should start there.

Q1 2026 Results

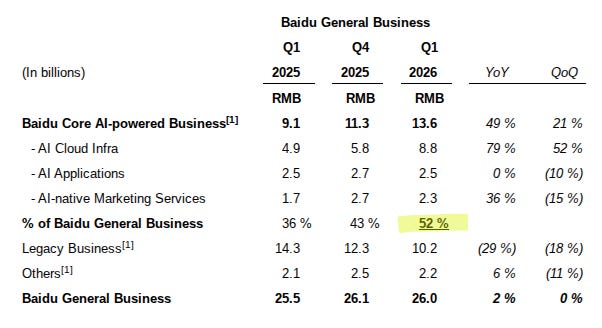

Baidu reported on May 18th. Revenue was RMB 32.1 billion, and Baidu General Business (which strips out iQiyi) came in at RMB 26 billion, up 2% year-over-year. First quarter of positive growth in a while.

The AI-powered business crossed ~50% of General Business revenue for the first time. RMB 13.6 billion, up 49%. AI Cloud Infra did RMB 8.8 billion, up 79%. GPU cloud revenue grew 184%. Impressive huh?

Online marketing revenue was RMB 12.6 billion, down 22%. Search ads are shrinking, and honestly faster than I expected. Although part of me wonders if AI is just growing so fast that it’s making everything else look worse by comparison. A year ago search was 63% of General Business revenue. Now it’s 48%. Either way the business is moving.

Non-GAAP net income was RMB 4.3 billion at a 14% margin, adjusted EBITDA was RMB 6 billion at 19%, and they beat EPS estimates by a few percent.

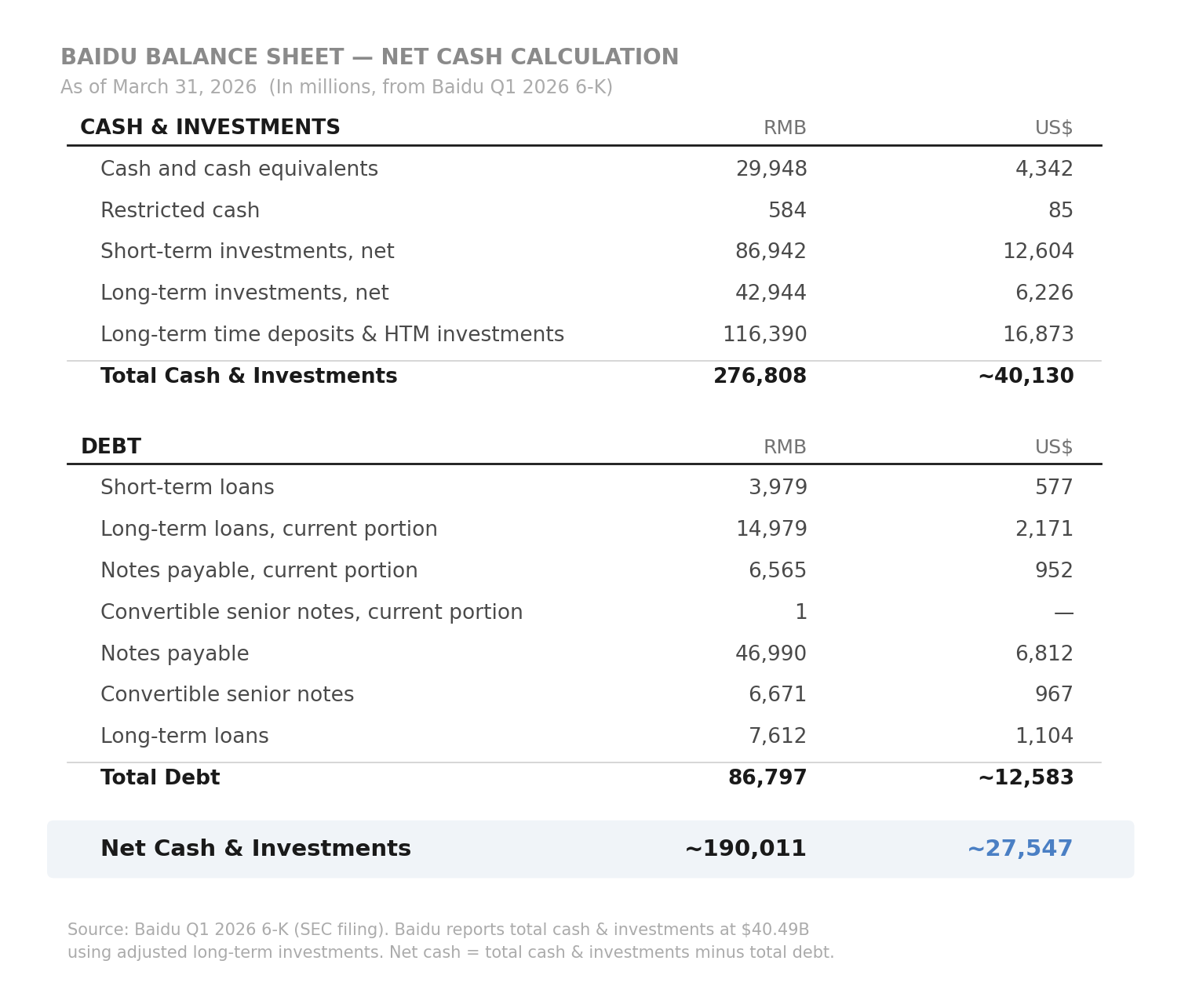

The balance sheet has roughly $40.5 billion in total cash and investments against about $12.6 billion in debt and debt-like financing, so call it roughly $28 billion of net cash and investments.

That number is still in the same ballpark as when I first wrote about Baidu in 2025, helped by slightly lower debt.

The quarter confirmed what we already knew, which is that AI is becoming the business while search slowly fades into the background.

The Chips

So, back to Kunlunxin.

The quarter is mostly context. Baidu has been moving this way for a while now. AI is becoming a bigger piece of the business, and each quarter has made that a little harder to ignore.

But Kunlunxin is the part I think still needs more attention.

The company went from roughly RMB 2 billion in revenue in 2024 to an estimated RMB 3.5 billion in 2025, and it reportedly hit breakeven, with external customers (meaning not Baidu) crossing 50% of revenue for the first time.

The customer list is pretty hard to argue with: Tencent, Vivo, China Mobile (which gave them a contract worth over RMB 1 billion), with JD, Meituan, ByteDance, State Grid, and China Merchants Bank all in various stages of testing or deployment. By unit volume, Kunlunxin is the #2 domestic AI chip shipper in China behind Huawei’s Ascend.

Two years ago this was an internal cost center. Now it has a legitimate third-party customer base and it’s filing for a dual-track IPO.

The reason all of this happened is pretty obvious, at least in hindsight. Nvidia can’t sell advanced chips into China anymore, and no major Chinese company is going to build its AI future assuming that changes. Whether the restrictions ease or tighten, the pull toward domestic compute was always going to accelerate once it started. Kunlunxin happened to be in the right place with working silicon when the demand showed up.