Inside the AI Capex Boom

A deep dive into the capex plans of Microsoft, Amazon, Google, Meta, and Alibaba.

Every earnings season has a theme. In 2022, executives were still talking about supply chain bottlenecks and chip shortages. By 2023, the focus had shifted to inflation, rising interest rates, and cost control.

More recently, the focus has turned to AI infrastructure.

Quarter after quarter, Big Tech has been reporting stronger and stronger results, with AI driving much of the momentum. These models need vast computing power, and the easiest place to get it is the cloud. Selling that compute—along with storage and high-end chips—has become a meaningful growth engine, lifting both revenue and margins.

Microsoft’s Azure, Google Cloud, and Amazon’s AWS are all seeing tangible top-line growth and profitability gains tied to AI demand. Even Meta, which doesn’t sell cloud capacity, is pouring billions into AI because it’s improving ad performance and boosting profits.

At this point, the connection between AI adoption and earnings is too consistent to dismiss. The payoff is showing up now, not in some distant future—which is why the largest U.S. tech companies are committing to some of the most aggressive capital spending plans in years.

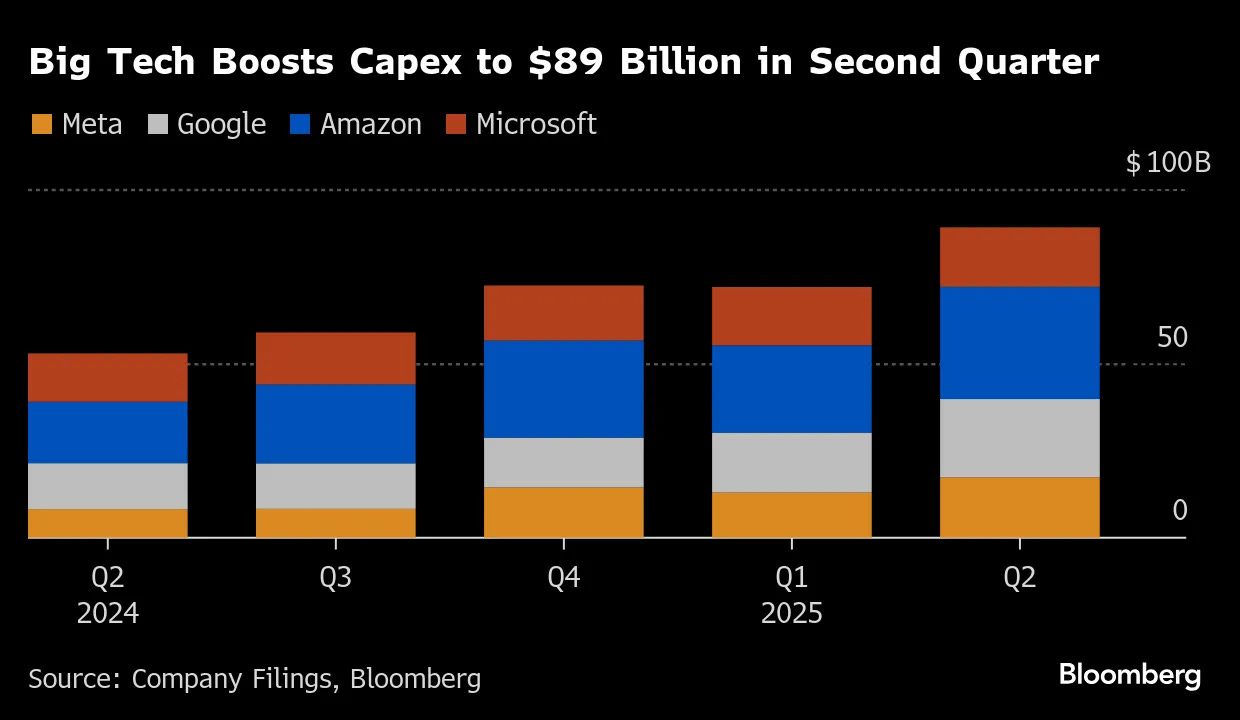

Leading the pack is Microsoft, where Azure’s revenue jumped 39% year over year last quarter. Management followed with guidance for roughly $30 billion in capital spending this quarter, aimed at projects with contracted customers already lined up.

Alphabet told a similar story. After a strong Q2, it raised its full-year capex plan from around $75 billion to $85 billion. Google Cloud grew revenue 32% and nearly doubled its operating margin to 20.7%. The cloud backlog now sits at about $106 billion—demand that’s already sold and just needs to be switched on.

AWS, the original giant in this space, is still in expansion mode. Second-quarter revenue reached $30.9 billion, up 17.5% from a year earlier, with $10.2 billion in operating income—a 33% margin. Amazon spent about $31 billion on capex in the quarter, most of it on AWS, and said this level of spending will continue through the year.

Even Meta, which doesn’t rent out cloud capacity, raised its 2025 capex guide to $66–72 billion, saying AI is improving ad efficiency enough to pay for itself.

Add it all up, and you’re looking at nearly $100 billion in spending from the big four U.S. tech names in a single quarter.

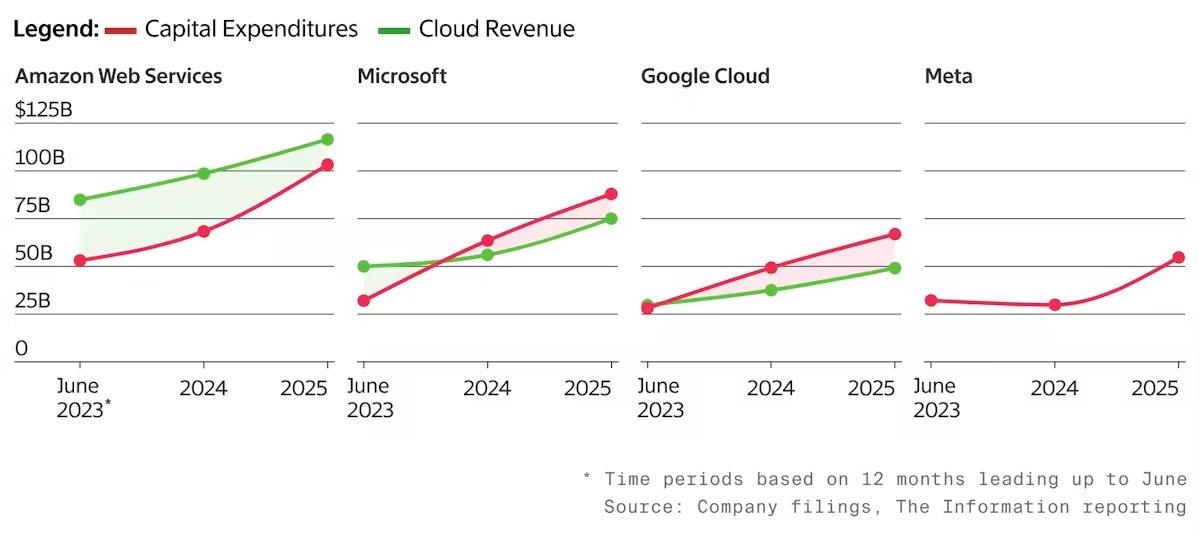

And as the chart below shows, in several cases the capex curve is now climbing faster than revenue itself—a sign of just how aggressive this race has become.

These are enormous numbers, and that’s where my skepticism starts to creep in.

In the short term, the spending makes sense—demand is strong and margins are expanding. But AI infrastructure is expensive to build and even more expensive to run. Power, cooling, and ongoing maintenance all pile up on the expense side. Depreciation schedules on this kind of hardware might be three to five years, but the pace of chip innovation means some of it could be outdated even sooner.

The underlying assumption is that these data centers will quickly fill with high-margin workloads. I’m not convinced that will always be the case, especially as competition forces prices lower.

We’ve seen a version of this before. In the late 90s, telecom companies spent billions laying fiber, confident the internet would eventually fill the pipes. It did, but many of the companies that laid the fiber never lived to see the payoff. The winners became essential infrastructure, but the road there was littered with failures. The lesson is simple: the infrastructure can be necessary and valuable in the long run, but the ROI doesn’t arrive evenly for everyone.

Which brings me to Alibaba.

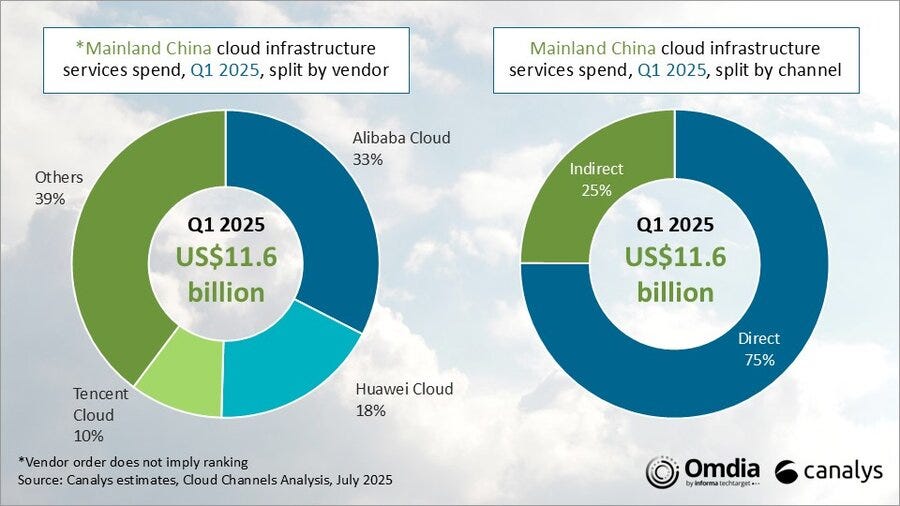

When I look at the numbers, Alibaba’s cloud business is in a strong position and quietly picking up speed. In China—the second-largest cloud market in the world—it’s been the clear leader for years, holding roughly a third of the market. Chinese companies spent about $11.6 billion on cloud infrastructure in the first quarter alone, according to Canalys, up 16% from last year.

Within that, AI-related workloads on Alibaba’s cloud have been growing at triple-digit rates for seven consecutive quarters.

Globally, it’s the fourth-largest provider with around 4% market share. That’s nowhere near AWS or Azure in scale, but it’s big enough to matter, especially when most of its growth comes from markets where it already has deep relationships and a local advantage.

After a slow couple of years, growth has returned. In the March quarter, Alibaba’s Cloud Intelligence revenue rose 18% and segment adjusted EBITA jumped 69%. That suggests the infrastructure they’ve built is finally being used more efficiently, and customers are spending on higher-value services. Management has pointed to faster growth in public cloud and strong AI adoption—exactly the kind of pattern we’ve seen drive results for the U.S. hyperscalers.

That’s the key connection. The same forces that have boosted AWS, Azure, and Google Cloud—sticky AI workloads, higher margins, and deeper customer lock-in—are taking shape for Alibaba. The difference is that Alibaba has been more selective with its buildout.

In February, it announced plans to invest more than $50 billion over the coming years in cloud and data center expansion. But it has a track record of scaling in step with actual demand. That spend will likely focus on areas where demand is visible—AI inference, data services, and industries already tied into its wider business.

That wider business is its biggest advantage. If your sales run on Taobao, your logistics on Cainiao, your payments on Alipay, and your internal communications on DingTalk, adding an AI service from Alibaba Cloud isn’t a major project—it’s a quick integration. Once those tools are trained on your data, moving to another cloud means months of retraining and reconfiguring. Most companies won’t bother.

This is why I’m bullish. I expect Alibaba Cloud to grow more than 20% when it reports in August, and I think that pace could accelerate into the 20–30% range for the next few years. AI is moving from pilots to production, Chinese companies are shifting more workloads to the public cloud, and Alibaba is in a prime position to win that business.

There are risks—policy changes, export controls—but these are well known and, in my view, already priced in. At today’s valuation, the market isn’t giving much credit for any of this. With a leading share in China, a fast-growing AI workload base, a $50 billion expansion plan backed by plenty of cash, and a profitable core business, the upside looks better than the sentiment suggests.

Back in the 90s, a lot of telecom companies spent big laying fiber. The internet eventually filled those pipes, but not everyone who built them made it. AI infrastructure will probably follow a similar path—huge long-term payoff, but a bumpy road getting there. The U.S. hyperscalers are going all-in, spending faster than revenue’s growing. Some will hit the jackpot, others might find themselves with expensive data centers that aren’t earning their keep.

Alibaba’s playing it differently. They’re adding capacity where they already know the demand exists—inside an ecosystem where customers are deeply tied in. If your sales, payments, logistics, and communications all run through Alibaba’s platforms, moving your AI workloads there isn’t a leap—it’s just turning it on. And once you’ve done that, switching is more trouble than it’s worth.

The growth’s already showing up. AI workloads on Alibaba Cloud have been compounding triple digits for almost two years. Public cloud adoption in China still has years of runway, and Alibaba’s sitting on about a third of that market with profitability to match. They’ve got a $50+ billion buildout planned, but it’s targeted—more “expanding into demand” than “build it and hope.”

At today’s valuation, none of this is priced in. Most investors still file Alibaba under “China e-commerce” and move on. That’s fine. I’m happy to own a profitable market leader that’s quietly turning itself into one of the most important AI infrastructure companies in Asia—before the market catches on.

Really interesting, thank you for the write up!