Alibaba Cloud: What’s It Actually Worth?

I’ve beaten the Alibaba drum plenty by now. Cloud has been a big part of why, and it’s done a lot of the heavy lifting in the re-rating over the past year. But I still don’t think the market fully gets it.

This post is narrower than my usual Alibaba writeups. I want to think through one question: how big could Alibaba Cloud realistically become over the next three to five years, and what does that mean for the stock?

To answer that, I need to start with the market itself.

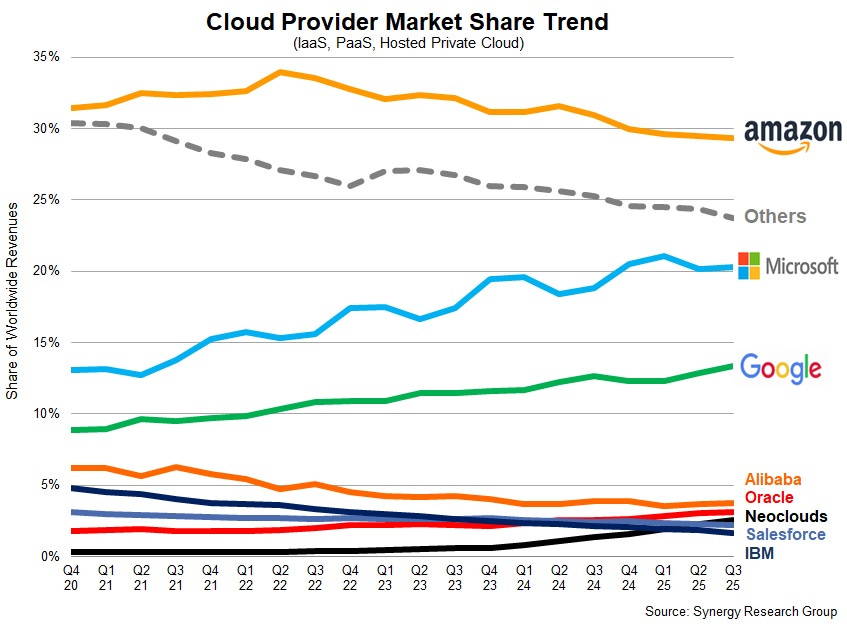

The global cloud infrastructure market is dominated by three players. AWS holds roughly 30% share, Microsoft Azure around 20%, and Google Cloud about 13%.

Together they control something like 63% of the worldwide market. That concentration has been remarkably stable. These are entrenched businesses with deep customer relationships, massive capex programs, and the kind of switching costs that make churn almost nonexistent at the enterprise level.

Alibaba sits at about 4% of global cloud infrastructure. On a worldwide basis, it’s a rounding error compared to the big three.

But global share is the wrong frame for thinking about this business. China is a separate and much younger market. It operates under different rules, different procurement relationships, different regulatory structures.

And in China, the picture looks completely different.

China Cloud Market

Market size depends heavily on what you’re measuring, and definitions vary a lot between sources. Let me walk through the main lenses.

CAICT, the China Academy of Information and Communications Technology, provides the broadest view. Their numbers show China’s total cloud market at RMB 616.5 billion in 2023, up 35.5% year over year. They forecast this exceeding RMB 2.1 trillion by 2027. That’s roughly a tripling in four years. Public cloud specifically was about 74% of 2023 spend, around RMB 456 billion, growing 40% year over year.

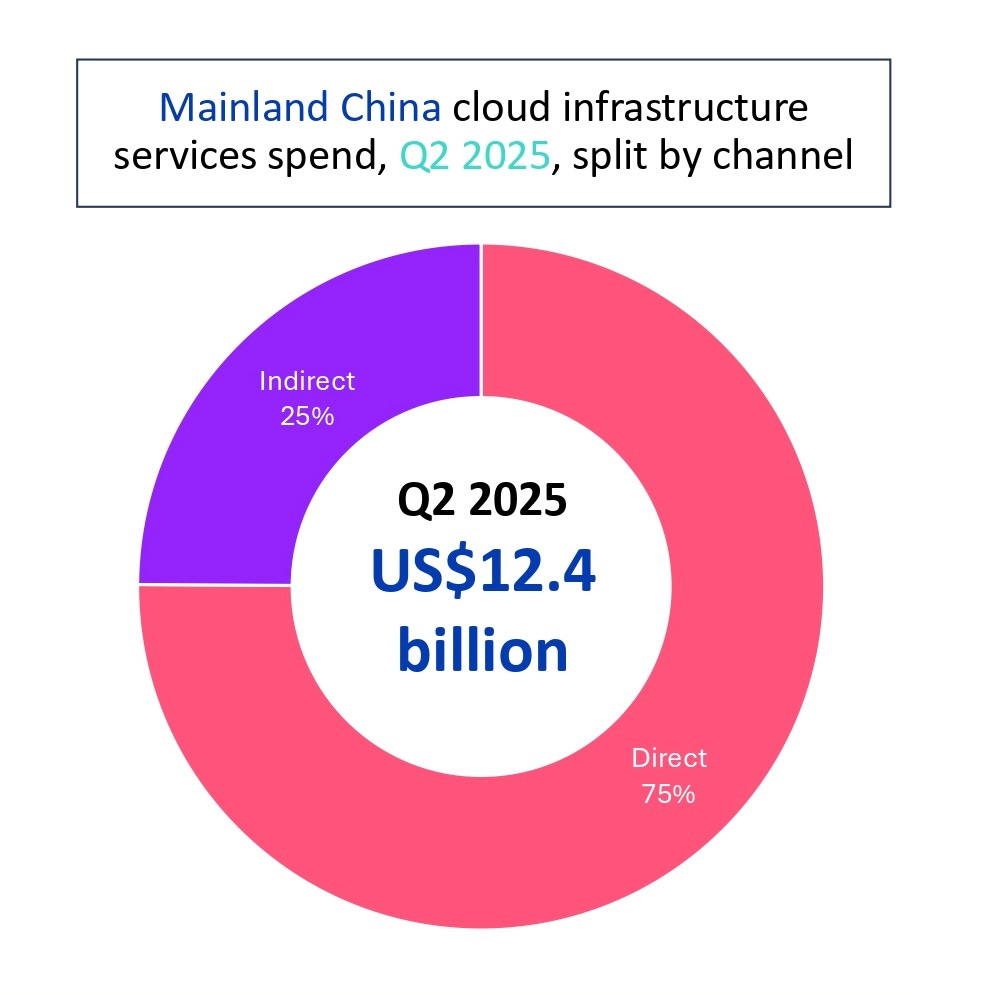

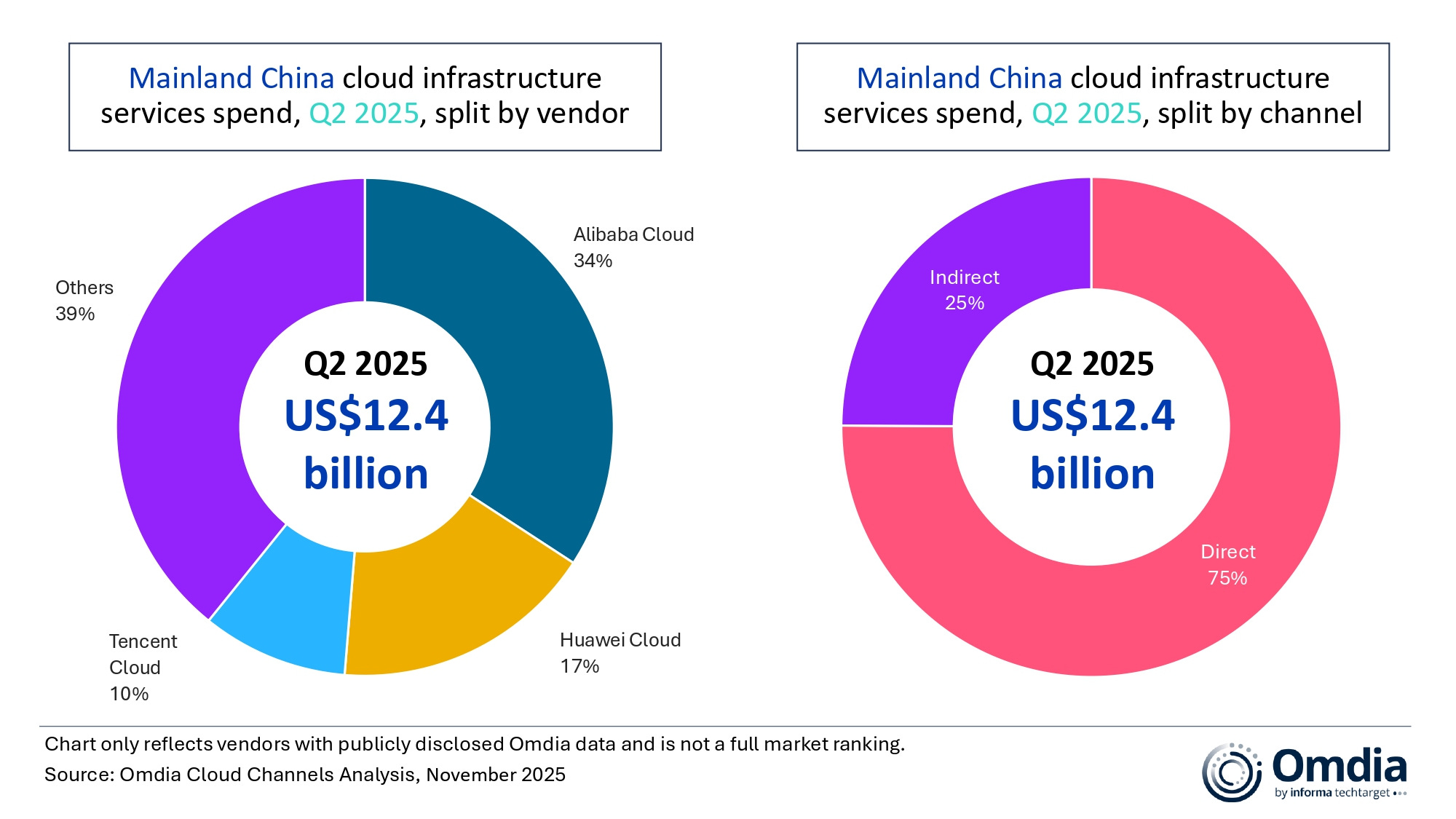

Omdia tracks a narrower slice they call “cloud infrastructure services,” which is closer to what most investors think of when they talk about AWS or Azure.

Their quarterly data shows Mainland China spend of $11.6 billion in Q1 2025, up 16% year over year, accelerating to $12.4 billion in Q2 2025, up 21% year over year.

All sources point to an acceleration in growth…

Various research houses estimate the China cloud computing market will reach somewhere between $100-140 billion by 2030, growing at 18-23% CAGRs depending on the methodology.

Mordor Intelligence pegs the 2025 market at around $50 billion, expecting it to reach $136 billion by 2030.

The practical takeaway is that however you slice it, China’s cloud market is large, growing faster than the global average, and still underbuilt relative to the US. The structural buildout has room to run.

Alibaba Dominates In China

Omdia’s share data for cloud infrastructure services shows Alibaba Cloud leading with roughly 34% share in the first half of 2025. Huawei is second at 17-18%. Tencent sits at about 10%. The rest is fragmented among state telecoms and smaller players.

This isn’t a close race. Alibaba has roughly double the share of its nearest competitor.

The reasons for domestic dominance are boring but important. Data sovereignty matters. Government procurement relationships matter. Regulatory familiarity matters. US hyperscalers can’t just walk into China and win enterprise contracts the way they can in Europe or Southeast Asia. The barriers are structural.

There’s also a segmentation dynamic worth noting. Alibaba and Tencent have historically been stronger with private-sector developers and internet-native workloads. Huawei and the state telecoms have structural advantages in government and SOE-heavy accounts.

These lines are blurring as AI pushes everyone toward full-stack offerings, but the segmentation still matters for understanding competitive dynamics.