Alibaba (BABA): Q1 2026 Earnings Review

After being written off quarter after quarter, it finally feels like sentiment is starting to turn.

Alibaba reported results this morning, and for the first time in a long while, the stock actually reacted the way it should.

Shares jumped more than 12%—the biggest post-earnings move we’ve seen in years. After being written off quarter after quarter, it finally feels like sentiment is starting to turn.

On the surface, the numbers weren’t great. Revenue for the June quarter was RMB 247.7 billion (~$34.6 billion), up just 2% year-over-year and a bit below expectations. Adjusted profit also missed, weighed down by continued investment in quick commerce. But if you back out businesses they’ve sold, revenue growth was closer to 10%. And GAAP net income still came in strong—up 76% to RMB 42.4 billion (~$6 billion)—helped by some investment gains.

The point, though, is that this quarter wasn’t about beating or missing a line item. What mattered was where the growth came from, and how management talked about the business.

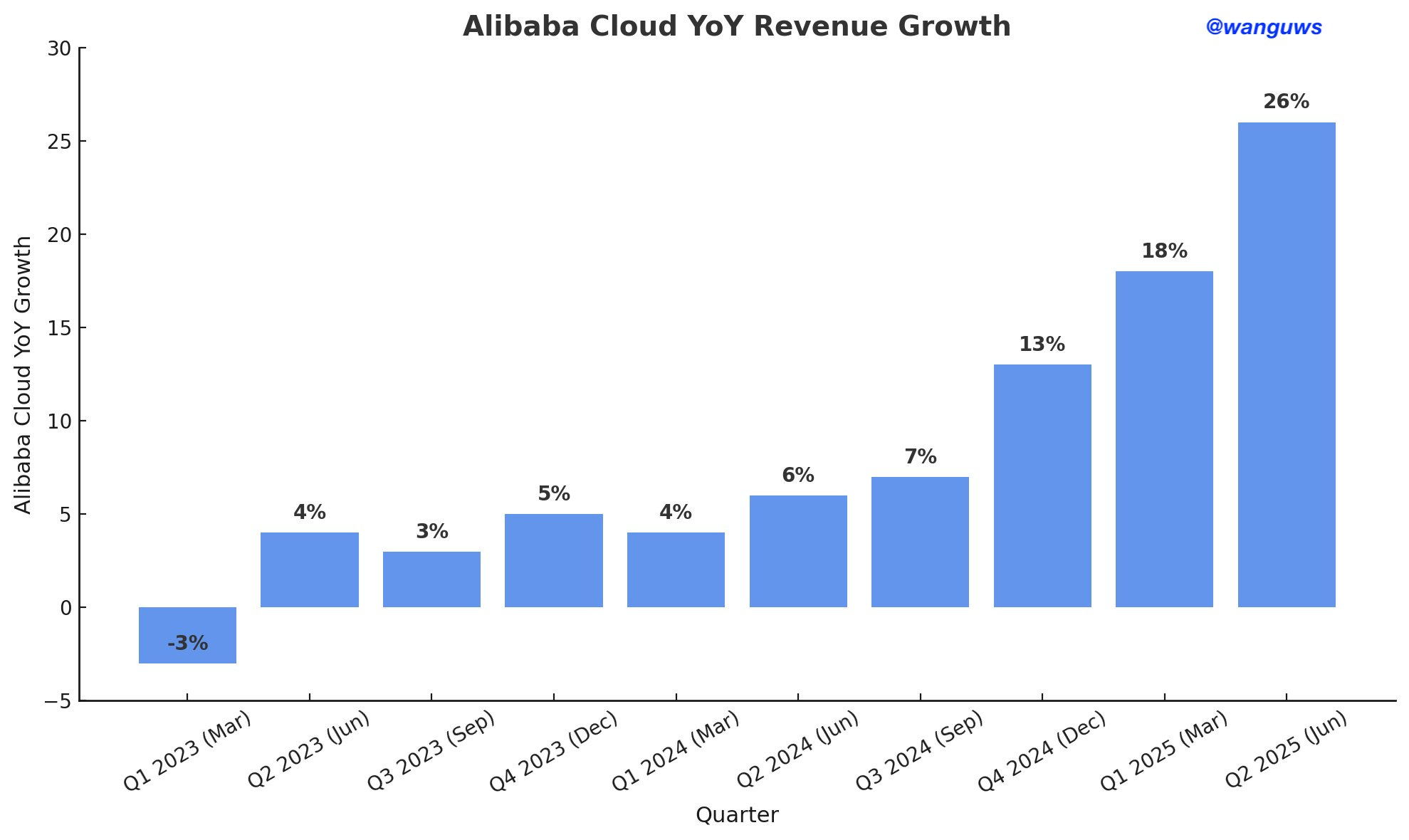

Cloud was up ~26%. International commerce grew ~19%. And the word that came up over and over—76 times on the call—was AI.

This isn’t just about Cloud anymore. AI is starting to show up across the whole ecosystem: logistics, advertising, customer engagement, even product rollouts. It’s becoming the common thread that runs through Alibaba’s businesses, and you can finally start to see it in the results.

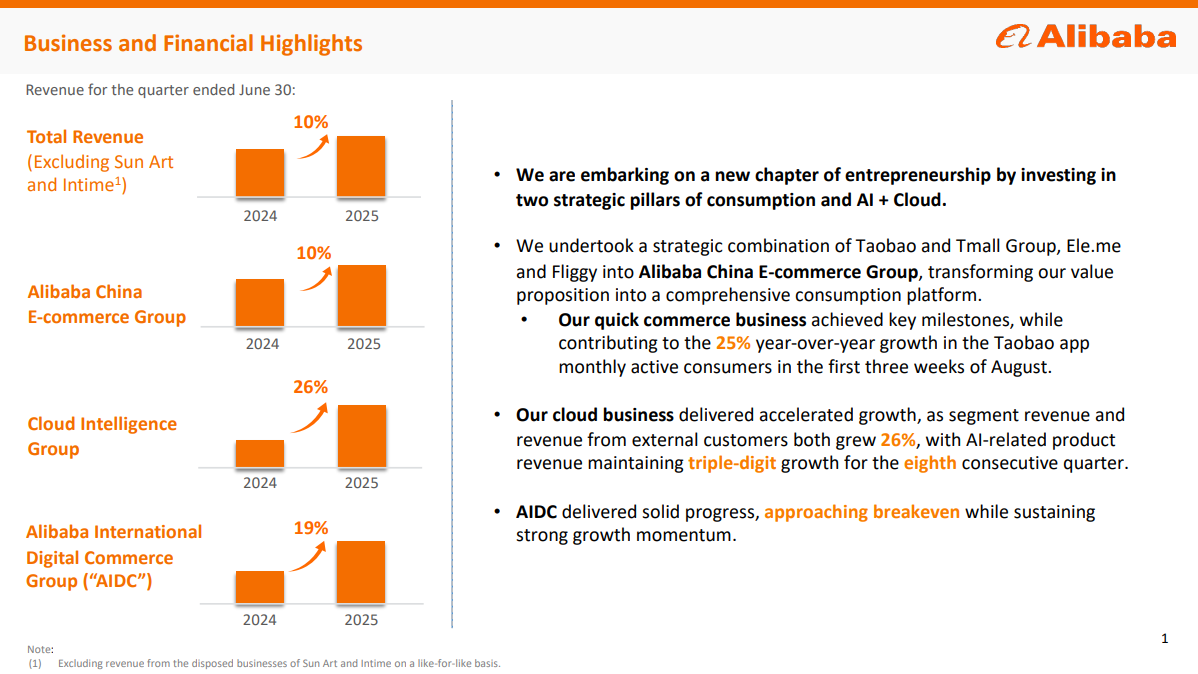

Business and Financial Highlights

China e-commerce: RMB 140.1B, +10% YoY

International commerce: RMB 34.7B, +19% YoY

Cloud: RMB 33.4B, +26% YoY

Quick commerce: RMB 14.8B, +12% YoY

Net income: RMB 42.4B, +76% YoY

Buybacks: $815M (7M ADS), $19.3B left on authorization

While the overall revenue figure looked modest, the core businesses are showing double-digit growth, Cloud is re-accelerating, and profits nearly doubled. That’s not the picture of a company in decline.

Cloud and AI

The star of the quarter was Cloud. Revenue grew 26% year-over-year to RMB 33.4 billion, its fastest growth in years. For most of 2023, Cloud was stuck in the low single digits, even shrinking in early quarters. But the turnaround over the past 18 months has been sharp—growth went from negative in Q1 2023 to +26% this quarter.

AI is the main driver. Management noted that AI-related products have now grown at triple-digit rates for eight straight quarters and make up more than 20% of external Cloud revenue.

“Our cloud business delivered accelerated growth, with AI-related product revenue maintaining triple-digit growth. We will continue to invest in anticipation of customer growth and technology innovation to maintain our market leadership.”

Margins are improving too, with adjusted EBITA up 26%. That tells you this isn’t just a top-line growth story—efficiency is moving in the right direction. And Alibaba is investing with intent: this quarter it rolled out its own AI chip, part of a longer-term plan to reduce reliance on Nvidia and strengthen domestic supply.

For years, the knock on Alibaba was that Cloud wasn’t living up to its potential.

Now, with back-to-back quarters of accelerating growth and AI becoming a meaningful contributor, it’s clear the business is entering a new phase. If this trajectory continues, Cloud won’t just be an earnings driver—it’s the piece that will force the market to finally stop treating Alibaba as “just another e-commerce company.”