Alibaba (BABA): Fundamentals > Headlines

I want to start with the obvious.

There’s a declassified memo floating around DC claiming Alibaba has been helping the Chinese military with tech that could be used against the US. Payments, data, IP-theft tools, the usual laundry list.

Alibaba didn’t waste time responding. They called the claims “completely false,” questioned the motivation behind the leak, and pointed out the FT couldn’t verify any of it.

“We question the motivation behind the anonymous leak, which the FT admits that they cannot verify. This malicious PR operation clearly came from a rogue voice looking to undermine President Trump’s recent trade deal with China.”

The headline is all we’ve got so far… there’s been nothing else since. No White House follow-up. No press briefing. No details. Just a one-off headline dropped into the news cycle and then radio silence.

To me, it feels like skepticism-by-design. Alibaba Cloud is re-accelerating. AI demand is exploding. They’re one of the only true full-stack AI players in the world outside the US hyperscalers. That kind of momentum puts a target on your back.

The timing doesn’t feel random either. Jensen Huang just said China could win the AI race. He had to walk it back almost immediately, but the point landed. China’s tech ecosystem, especially Alibaba Cloud, is moving faster than Western headlines admit. So when an unverifiable memo suddenly appears casting Alibaba as some kind of covert military contractor, I assume it’s meant to cool enthusiasm.

It’s also a bit funny if you step back. The US government uses Palantir and half a dozen defense-adjacent tech firms to build targeting, surveillance, and intelligence systems. That’s not a secret. Yet everyone is supposed to be shocked that China might expect similar cooperation from its own national champions? Come on. Same playbook, different team colors.

Anyway, the bigger point is none of this touches the actual Alibaba thesis. What it does show is that the stock is still heavily influenced by headlines. And when prices move more on noise than numbers, there’s usually opportunity for anyone willing to sit through the nonsense.

I’ve owned Alibaba through every ugly headline you can name. The crackdowns. The delisting fears. The “China is uninvestable” era. The Jack Ma drama. Through all of that, the business didn’t fall apart. If anything, it got healthier. They cut the fat, trimmed the empire-building, got serious about costs, and doubled down on what actually matters: cloud and AI.

And that’s really where Alibaba sits today, right at the intersection of two forces I don’t think the market has fully priced in.

A multi-year China equity bull market built on policy support and a gigantic savings pool that has to leave bank deposits at some point

Alibaba’s position as China’s leading full-stack AI and cloud platform, with most of the restructuring behind it

This post is my attempt to lay out a clean, valuation-anchored bull case. I will lean bullish, but I am not ignoring the obvious risks.

The China Setup

I’ll keep the macro picture short because I’ve talked about it plenty already. The point is pretty simple: the backdrop in China looks a lot better today than it has at any point in the last couple of years.

Policy has shifted in a real way. Rates have been cut, reserve requirements have come down, and liquidity is finally flowing. Regulators are actively trying to support the market instead of letting it bleed out.

On top of that, households are still sitting on a massive pile of savings. Well over 100 trillion yuan in personal deposits, more than 300 trillion in the system overall. And banks keep nudging deposit rates lower. At some point people start looking around and thinking, “I need a better return than this.” That doesn’t mean the whole country piles into stocks at once, but even a small rotation can move prices.

Yet the market still values China like something is fundamentally broken. It trades at a clear discount to developed markets and even to broader EM. You get the usual EM discount, plus an extra layer of China fear, even though earnings across the big sectors have been fine.

I rely on Koyfin as a core part of my investment research. It’s a powerful platform for tracking markets, analyzing fundamentals, and building custom charts—all in one place.

Try Koyfin NOW and get 20% off any paid plan.

The question isn’t “does China go back to 10 percent GDP growth?” It’s simpler: can I buy structurally advantaged businesses at reasonable multiples while policy is easing and that savings pile gradually moves into risk assets?

If yes, then you want exposure to the structural engines: AI, digital infrastructure, and consumption.

Alibaba sits at that intersection.

The catch? The stock is no longer priced like a broken asset. It’s priced like a solid, slightly controversial compounder. You’re not getting paid for disaster anymore. You’re getting paid for uncertainty around how big the cloud and AI opportunity really is.

Cloud and AI

A year ago Alibaba Cloud was treated like a problem child. Growth had slowed, there were questions around strategy, and the market wanted proof that AI could turn into real money.

We have that proof now.

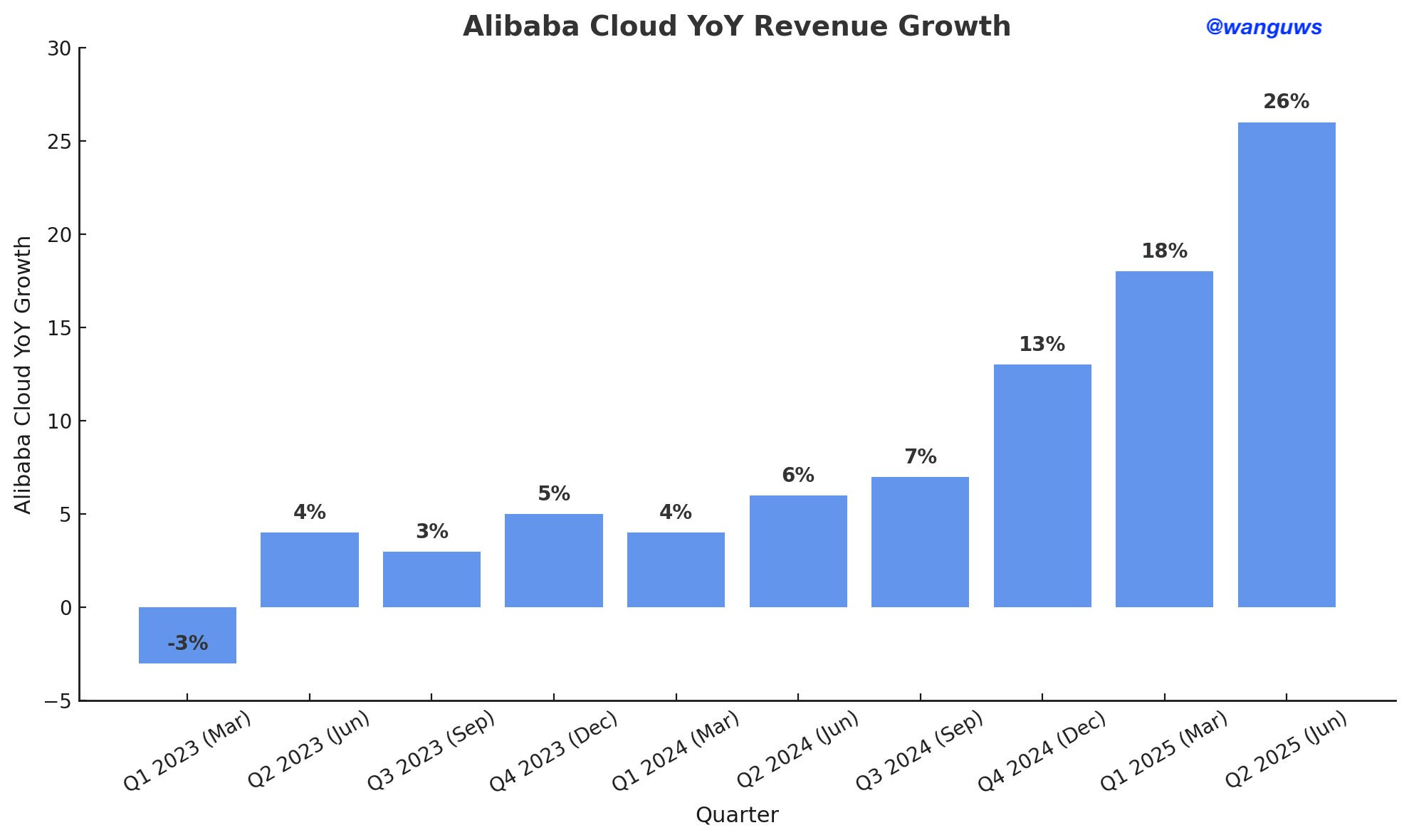

Cloud revenue has re-accelerated for 5 straight quarters. The latest quarter came in around 26% year-on-year to roughly 33.4 billion RMB, and AI-related products already account for more than 20% of external cloud revenue. Those AI products have been growing triple digits for multiple quarters.

That’s a real trend. It’s also a big reason why the stock has already doubled this year.

China’s approach to AI is different from the US “one killer consumer app” mindset. Beijing sees AI as industrial infrastructure—something embedded into logistics, manufacturing, financial services, public systems, healthcare. Everything behind the scenes.

That matters because it creates steady, long-duration demand. Government agencies and big enterprises don’t churn. They pick a partner, integrate deeply, and stick with them. And in China, Alibaba is king.

They are one of the only full-stack providers in the world. Infrastructure, Qwen models, enterprise tools, consumer applications. The feedback loop is tight. What gets built for Taobao or Amap or DingTalk often becomes something enterprises can use the next quarter.

And now they are starting to show some consumer-facing ambition too. The recent revamp of Qwen into a more “ChatGPT-like” assistant hints at that. It is not a pivot away from enterprise or infrastructure. It is more of a signal that Alibaba wants Qwen to be a real brand layered on top of the same models and training clusters that power the back-end business. Early days, but the direction makes sense. In China’s system, owning both the pipes and the touchpoints has real strategic value.

Consensus is still sitting around 28 to 30% for next quarter’s cloud growth. I think that is too low. I think Alibaba Cloud prints 33 to 35% year on year this quarter.

If they hit that range, or even just match estimates, it confirms three things: