Alibaba (BABA): Cloud Keeps Accelerating

38% cloud growth, margin expansion guided, quick commerce profitability pulled forward

Alibaba reported Q4 2026 earnings yesterday morning and the market finally got the kind of cloud commentary it has been waiting for.

The reported numbers were definitely a bit confusing/mixed. Revenue was fine, profitability was pressured, and quick commerce is still weighing on margins. None of that is new though. That has been the setup for the last few quarters.

What was different this quarter, or at least much clearer, was the shape of the business itself. The restructuring is mostly behind them, the divestitures are fading out, and you’re really starting to see Alibaba as just two businesses at this point: E-commerce and Cloud/AI.

And on the cloud side specifically, this was the quarter where management got a lot more direct about the AI revenue trajectory and where margins are heading.

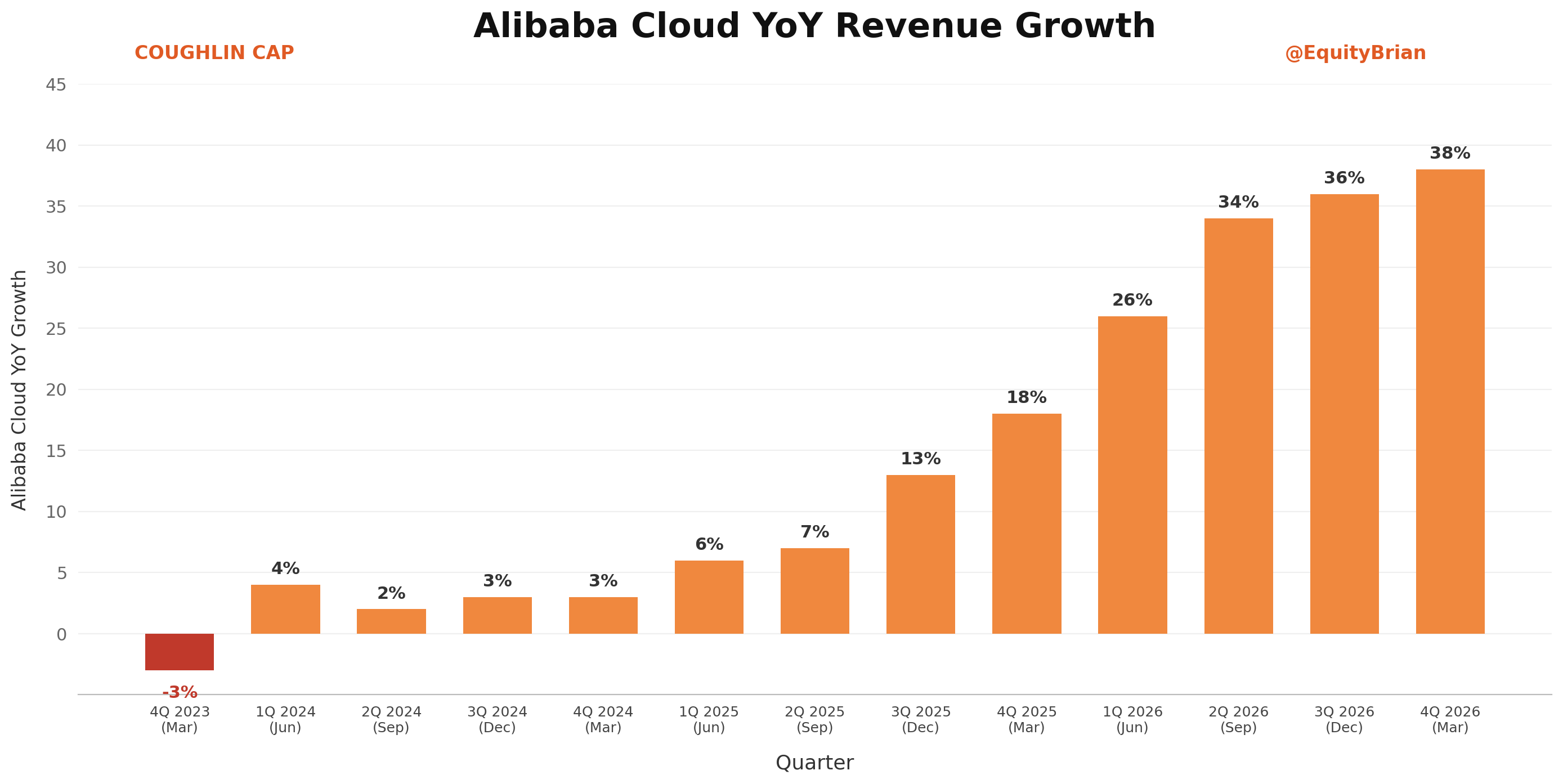

Cloud

Cloud revenue grew ~38% year-over-year, with external revenue up roughly ~40%. Cloud EBITA was up ~57% on a roughly ~9% margin. Management once again guided to further acceleration from here.

AI-related products hit RMB 9 billion in the quarter, triple-digit growth for the eleventh straight quarter, now representing about ~30% of external cloud revenue.