A New Era for Chinese Equities

The evolution of value in the broader Chinese market

I rely on Koyfin as a core part of my investment research. It’s a powerful platform for tracking markets, analyzing fundamentals, and building custom charts—all in one place.

Try Koyfin now and get 20% off any paid plan.

I've spent a lot of time reflecting on China lately. Not just following the news or tracking market moves, but genuinely thinking about the long-term story.

It's easy to feel discouraged when headlines highlight regulatory crackdowns, economic slowdowns, or geopolitical tensions. Yet, beneath the volatility and constant noise, I keep coming back to something deeper—a fundamental shift that's quietly but steadily unfolding in the broader Chinese market and its leading companies.

For years, China’s tech giants prioritized one thing above all else: growth. Profits took a back seat as expansion was king. From the 2010s well into the early 2020s, capital allocation revolved around building sprawling digital empires—new ventures, bold acquisitions, and aggressive market subsidies designed to capture market share at almost any cost. Returning capital to shareholders through dividends and buybacks was simply not part of the strategy.

That era has decisively come to an end.

Over the past couple of years, we've witnessed a significant evolution—not just in how these companies deploy their cash, but more importantly, in how they fundamentally view shareholder ownership. Initially, this shift was a response to slowing growth rates and heightened regulatory oversight. Now, however, it appears to be a permanent change in mindset. Chinese tech companies are genuinely embracing the concept of shareholder returns, marking a critical and positive turning point for investors.

This new approach began, as many transformative movements in China do, with policy. Following the stringent regulatory crackdown that began in 2020, the government made it abundantly clear that unchecked growth would no longer be tolerated. Instead, Beijing demanded greater financial discipline and accountability. One unmistakable message emerged: companies must start treating shareholders as true stakeholders rather than passive bystanders.

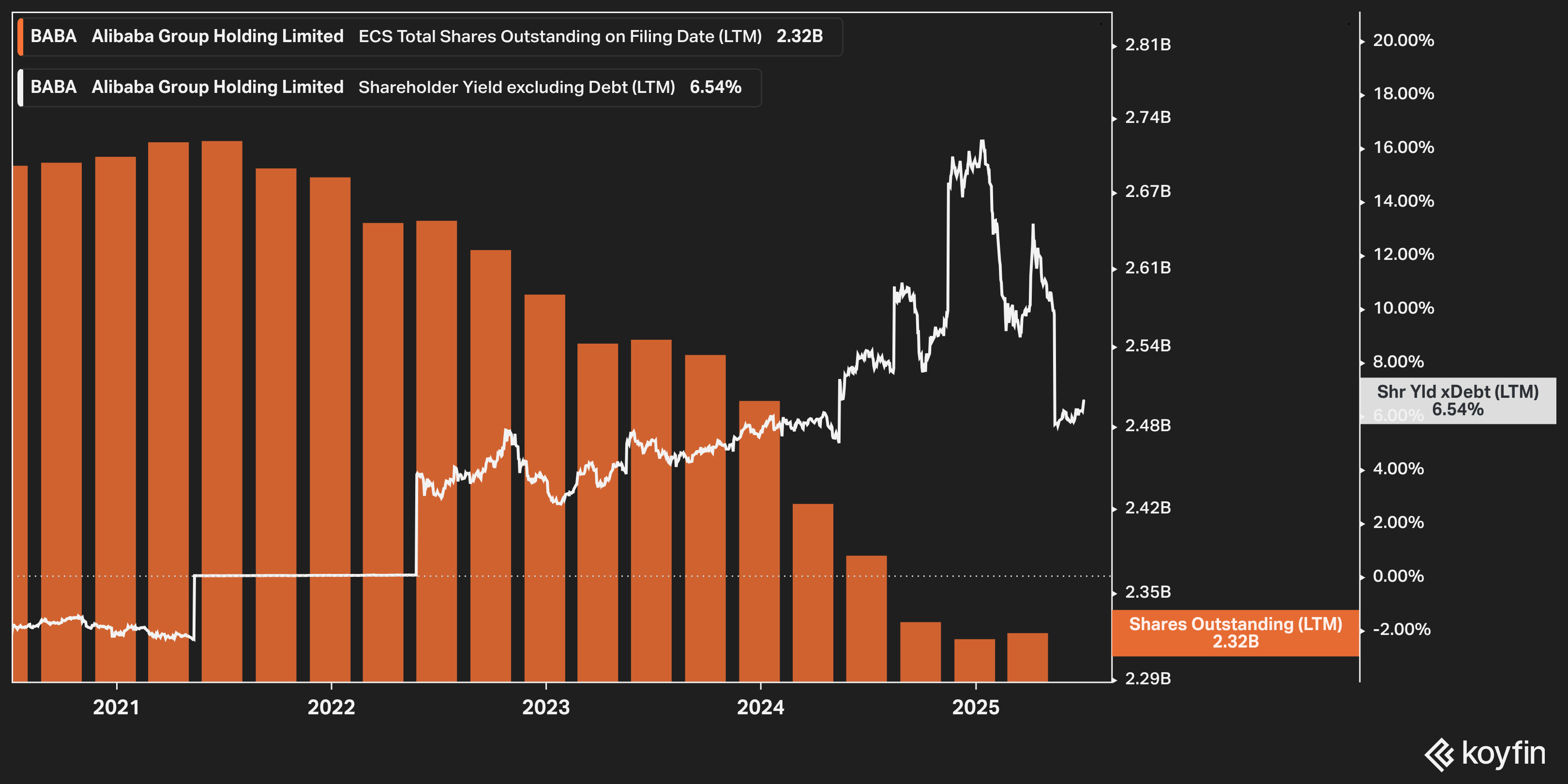

Corporate responses followed quickly. In 2023, Alibaba paid its first regular dividend and expanded its buyback program to $25 billion, targeting a 3% annual reduction in share count. It marked a turning point in how the company balances growth with shareholder returns.

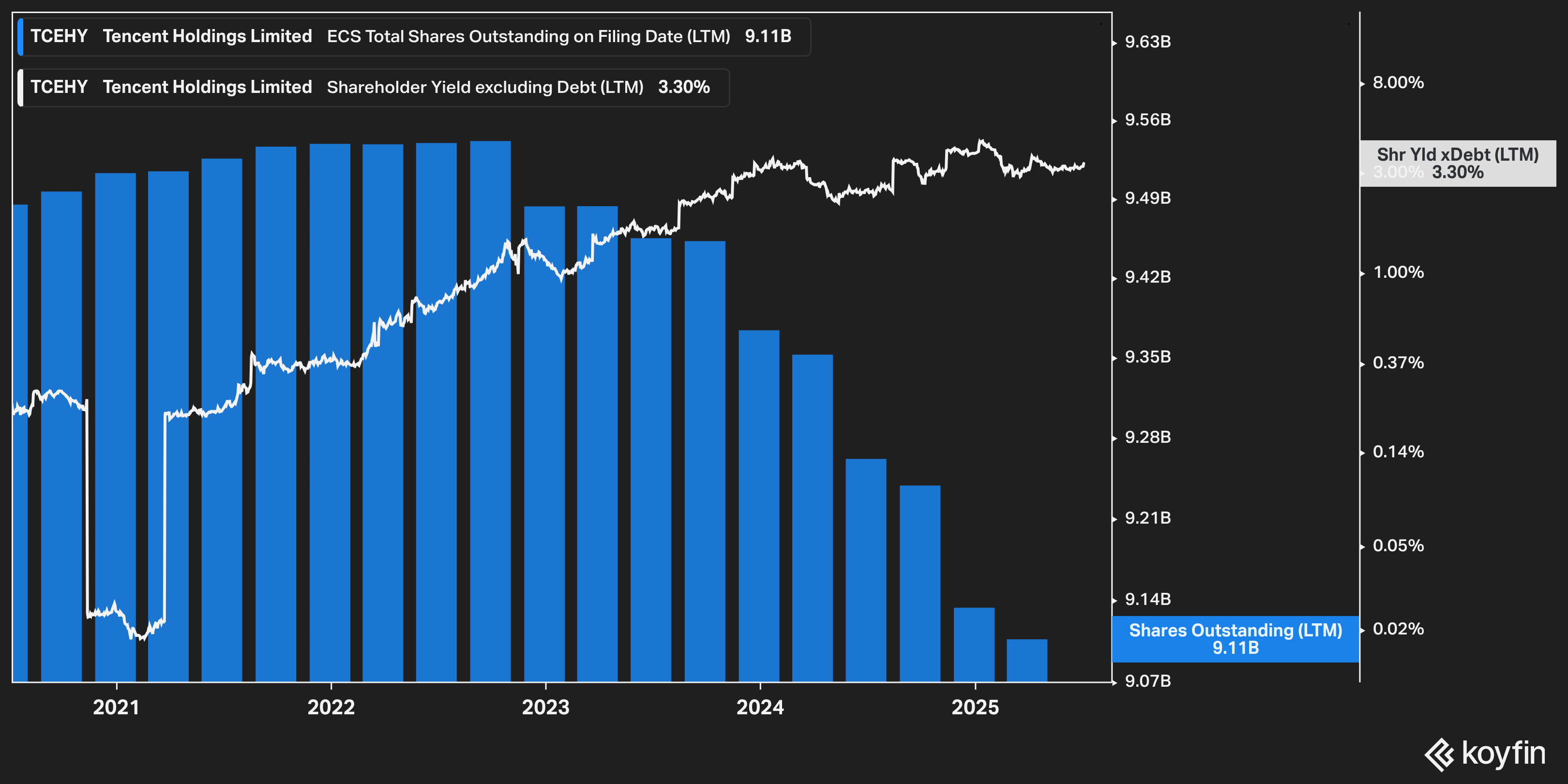

By 2024, Tencent had dramatically accelerated its buyback activity, spending an estimated HK$1 billion per day—the fastest pace in its history. This aggressive action demonstrated that shareholder returns had moved from a secondary consideration to a central pillar of its capital allocation strategy.

JD.com quickly joined the movement, authorizing a new $5 billion buyback plan. Similarly, companies like NetEase, Baidu, and Kuaishou signaled their alignment with this strategic pivot, underscoring that capital returns were no longer isolated instances but industry-wide standards.

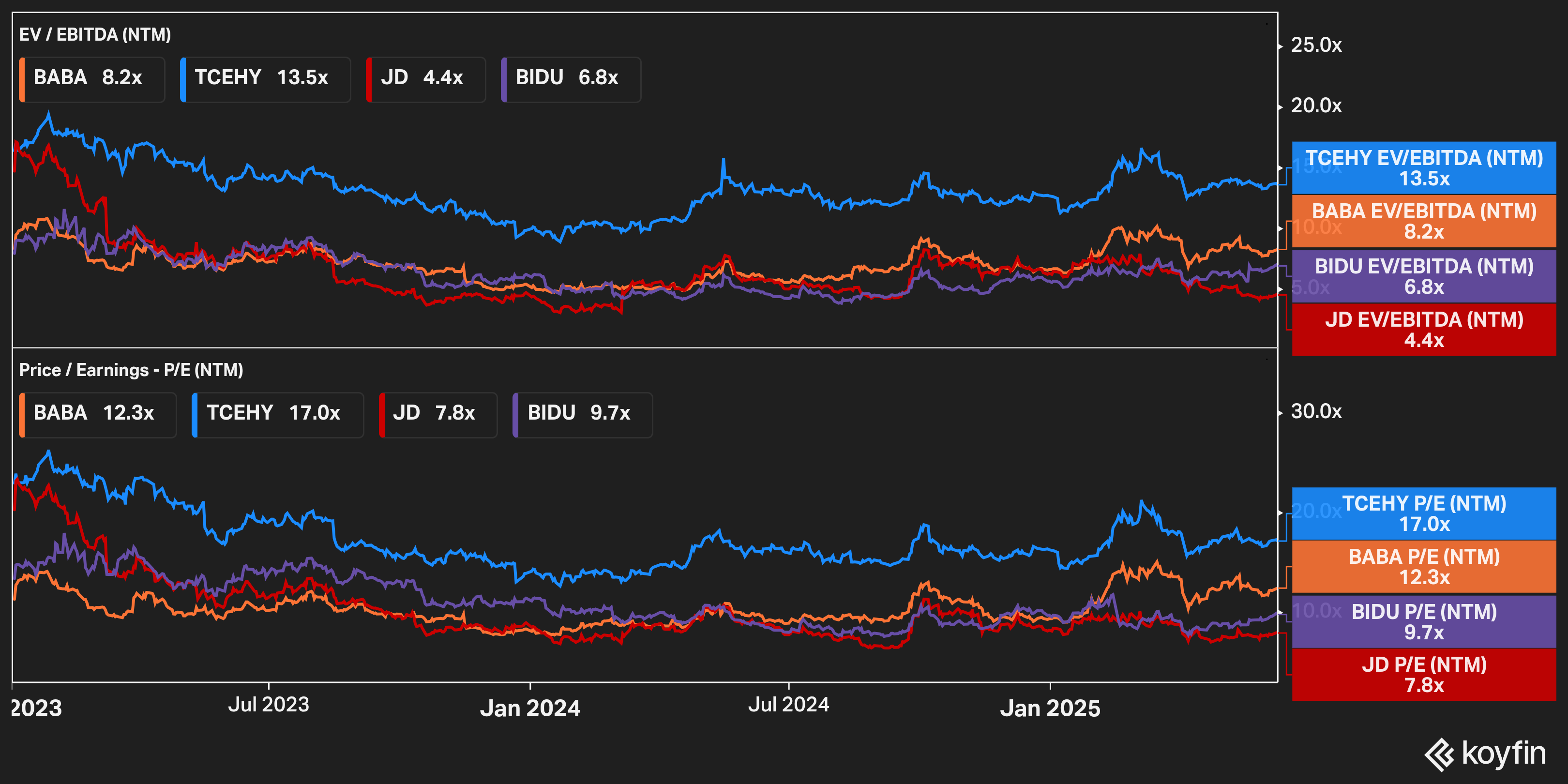

I think it’s important to recognize this change is not just a reaction to depressed stock prices. Rather, it reflects a fundamental rethinking of capital allocation amid more moderate domestic growth and compressed valuation multiples. With JD.com trading at less than 5x EBITDA, Alibaba and Baidu between 6–8x, and Tencent under 15x, buybacks have emerged as arguably the most attractive use of surplus capital.

Regulators are actively reinforcing this pivot. The State-Owned Assets Supervision and Administration Commission (SASAC) has openly encouraged SOEs to bolster investor confidence via dividends and buybacks. Simultaneously, the securities regulator is enabling companies to fund these programs more readily through bond issuances. This alignment of corporate and government interests suggests that nurturing an investor-friendly market environment has become a national priority.

In 2023, Chinese companies distributed a record RMB 3.4 trillion in dividends, with yields approaching 3%—the highest seen in nearly a decade. Moreover, nearly 1,900 A-share companies repurchased over RMB 130 billion worth of shares in just the first eight months of 2024, setting yet another milestone. Goldman Sachs forecasts shareholder returns could rise further to RMB 3.5 trillion in 2025, potentially establishing a new peak.

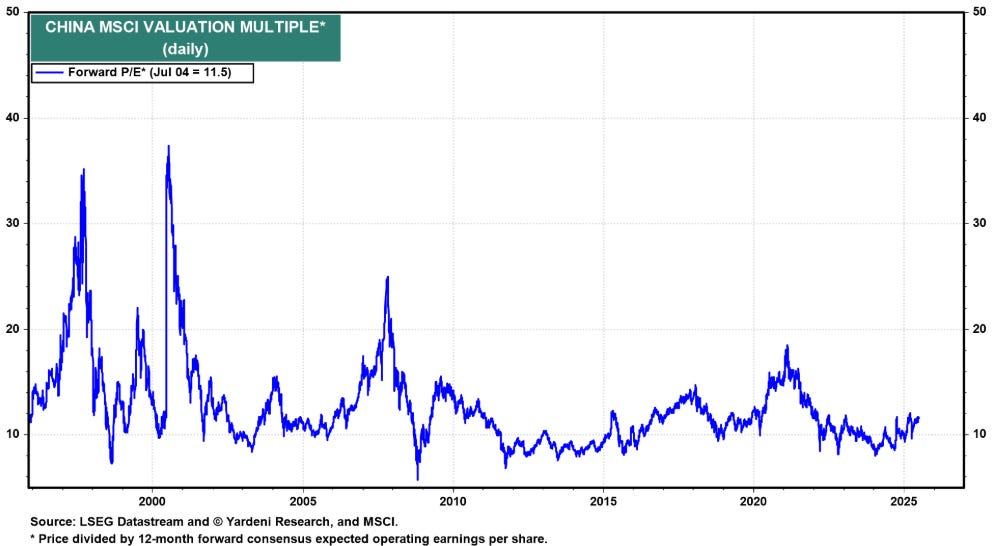

Investor response has been somewhat robust, reflected by surging southbound flows via Stock Connect—reaching approximately US$78 billion year-to-date and projected to surpass US$110 billion by year-end. This activity is spurred by compelling dividend yields and valuations, with MSCI China still trading around 11x forward earnings.

One persistent criticism of investing in Chinese tech historically was inadequate capital returns. Now, that critique is gradually losing validity.

Consistent returns of capital by fundamentally robust companies rebuild investor trust, attract long-term capital seeking stability and yield, and act as buffers in turbulent market conditions. Dividends and buybacks become stabilizing forces, reducing volatility and supporting longer-term ownership.

Importantly, this doesn’t imply a retreat from growth investments.

Tencent continues aggressive funding into AI and gaming innovations. Alibaba remains committed to cloud infrastructure expansion and advanced AI training capabilities. JD.com and Meituan maintain significant investments in logistics and local services despite fierce competition. The distinction is the measured and disciplined approach companies now adopt: growth at any cost has been replaced by the pragmatic question—what is truly the best use of our capital?

Further emphasizing the permanence of this shift is the growing role played by investor activism within the Chinese market. Shareholders have become more vocal in advocating for improved governance, transparency, and capital returns. Chinese management teams have started to engage more openly with investors, adopting international best practices such as regular communication, clearer financial reporting, and enhanced disclosure of strategic priorities.

Ultimately, this is not only a more rational approach to business; it's significantly better for shareholders.

If the 2010s represented unbounded growth and the early 2020s focused on navigating uncertainty, the mid-2020s promise a phase of real value realization. Chinese tech doesn't need radical transformation to succeed—it simply needs to keep its newfound financial discipline and shareholder focus.

This subtle yet powerful shift may very well be one of the defining narratives for emerging markets investors today. It offers a compelling narrative of a sector moving from adolescence to maturity, providing investors with an attractive blend of sustainable growth, financial prudence, and consistent returns.

So all-in Asia ? The fact that Trump and US urgently discussed trades with Chinese about rare earth shows the shift of power. While US shoot out load, bombing, making noise in media. Quiet China owns critical resources for the next era (IA, robotics) and clearly state that they don't Russian to stop war to retain US's attention from them. US= scream of the dying king, China = rise of Phoenix ?

Very good article, analysing different phases for Chinese equities. Remind me of Japan changing phase.