5 Stocks to Buy Now

A handful of names the AI mania is ignoring

Feels like AI and the bottlenecks around it are sucking the air out of every other conversation right now. Power, GPUs, CPUs, fabs, data centers, model labs, anything in that supply chain. That’s where the attention is. That’s where the money is. That’s where people are getting rich, and I get it. FOMO is a very powerful force…

But that kind of euphoria always creates ignored corners somewhere else. While everybody is piling into the same handful of trades, real businesses with real cash flow keep grinding away at multi-year lows because they don’t fit the theme of the moment.

So I want to do the unfashionable thing and write up five names I think are too cheap right now. Some of these I've written about before. Some haven't gotten as much airtime lately. What they all have in common is the stock has been getting worse while the actual business has been doing fine. Or in a couple of cases, very very well.

None of them are AI plays, at least not the kind people are chasing right now. That's not an accident.

That does not mean these are easy. Cheap stocks are usually cheap for a reason. Sometimes the reason is stupid. Sometimes it is very real. The job is figuring out which one you’re dealing with.

In no particular order…

Markel (MKL)

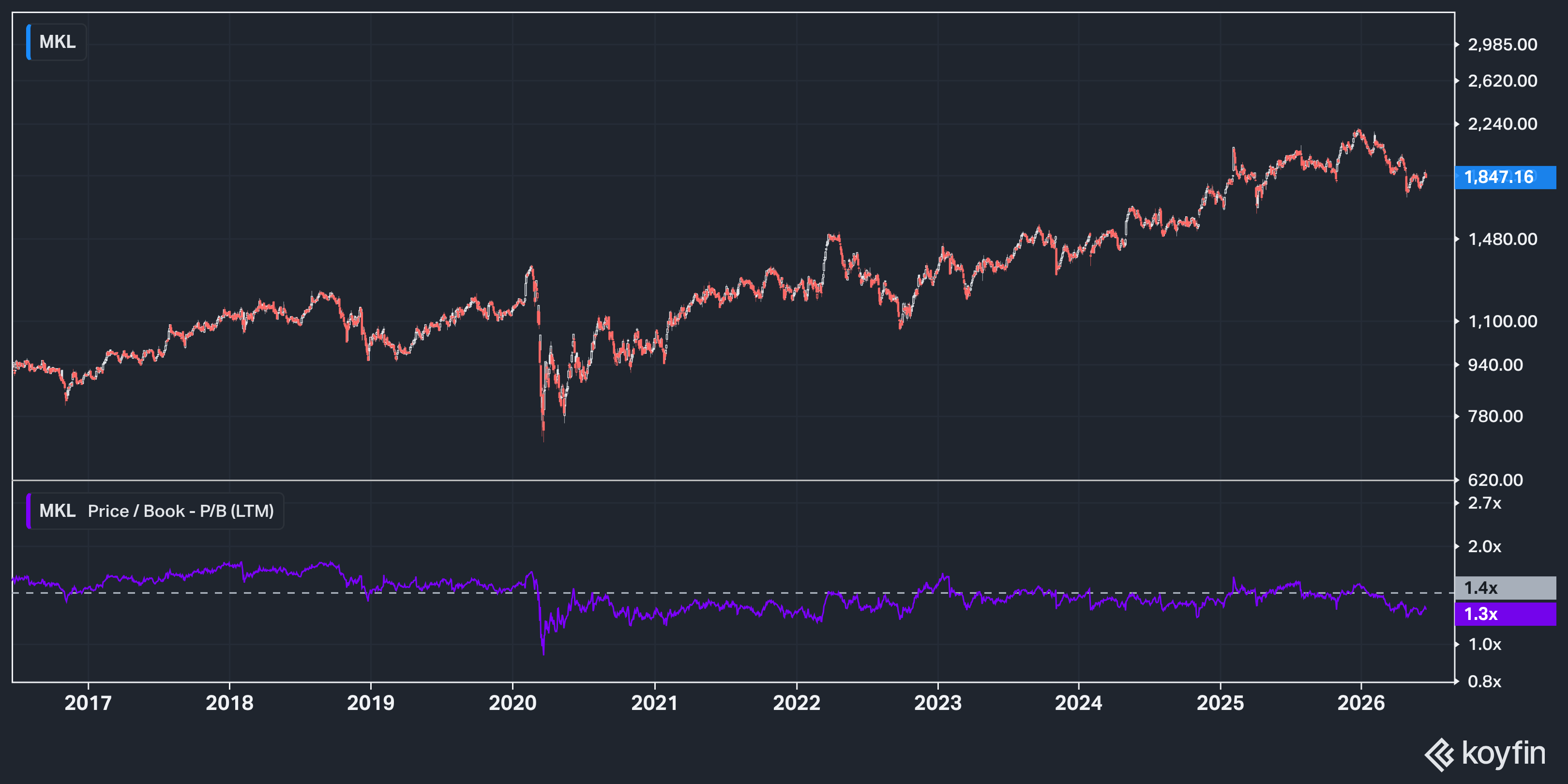

Markel is the lowest blood pressure name on this list.

No one is going to confuse this with a rocket ship. It’s specialty insurance, an investment portfolio, and a bunch of operating businesses inside Markel Ventures. That mix has always made the “mini-Berkshire” comparison easy, even if the comparison has been beaten to death at this point.

The stock has finally gotten interesting again. At around $1,850, you’re paying roughly ~1.3x book. That’s not a screaming 50-cent dollar. But for Markel, which has historically gotten more respect than this, it’s a reasonable starting point.

The insurance business also looks better than the headline numbers suggest. Q1 GAAP operating results were messy because of equity portfolio marks, but adjusted operating income was up 4%. The insurance combined ratio improved to 93%, and Markel Insurance adjusted operating income rose 31% to $369 million. That’s the stuff I care about.

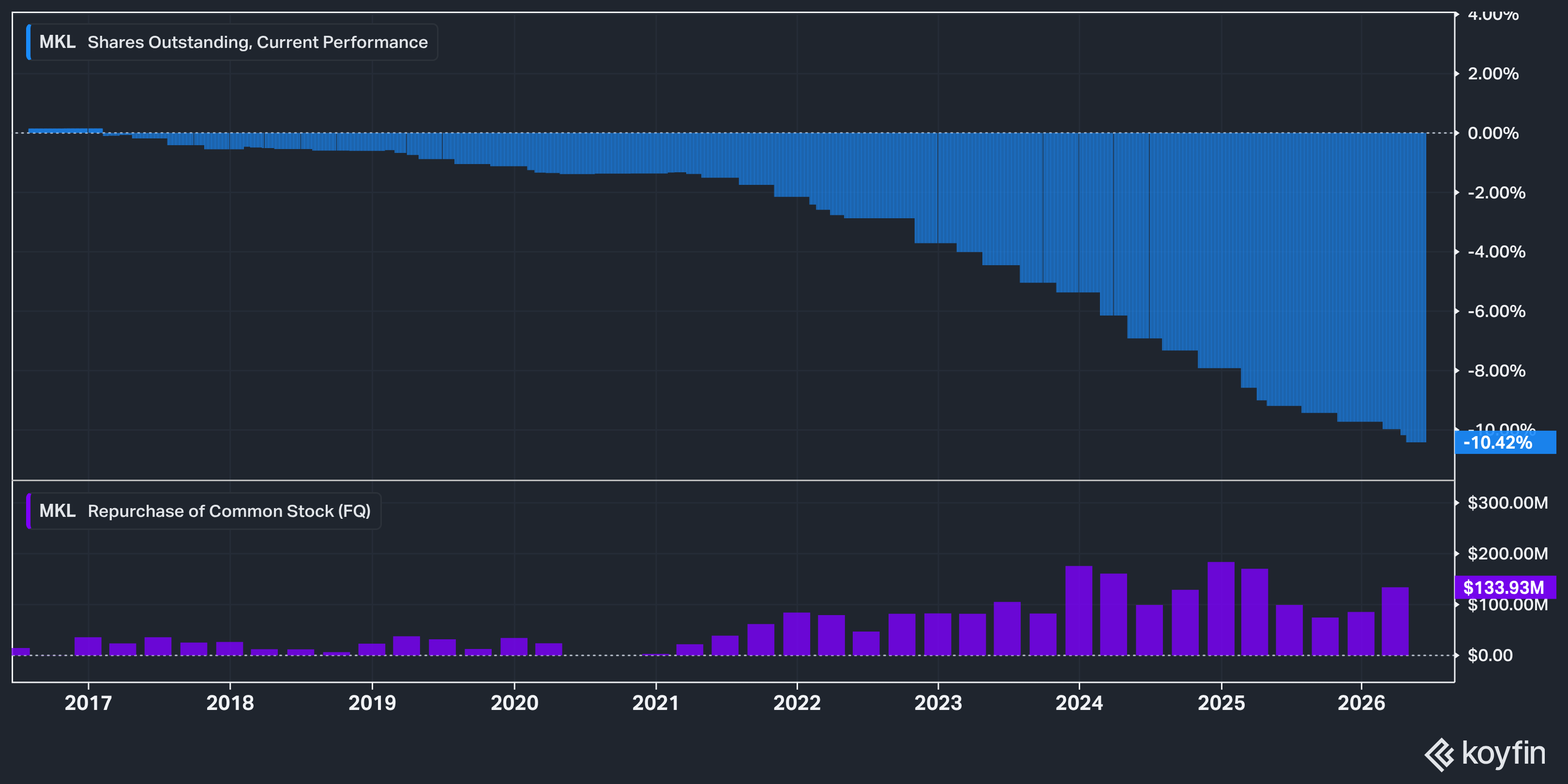

Markel also bought back $134 million of stock in Q1, while adjusted underwriting gross premium volume still grew 10% excluding the impact of Global Reinsurance and Hagerty-related changes. I’m not looking for fireworks here. I’m looking for quiet compounding and intelligent capital allocation, and that’s what they keep delivering.

You don't need perfection from Markel. You need underwriting to stay disciplined, Gayner to keep allocating capital decently, and the share count to shrink when the stock is cheap.

This is not the name I expect to double overnight.

It is the one I expect to wake up ten years from now and be glad I owned.

The other four names are for paid subscribers.

Paid gets you the full archive, nearly 200 posts, plus every new writeup from here. It’s $24/month or $220/year.

I also opened a lifetime option to the email list yesterday. It’s $600 one time, no renewals ever. The Stripe link is capped at 10 total spots, and 8 are left as of right now.